Personal Wealth Management / Market Analysis

Why Gold's Glitter Shouldn't Catch Your Eye

Six-year high or no, gold still isn’t a worthy long-term investment.

What is shiny and yellow and at a six-year high? Gold, of course! Headlines are having a field day with this, spouting all the reasons this most precious of metals could soar from here and even bust through 2011’s record high of $1,921 per troy ounce.[i]

Some of those reasons are purely technical, using jargon like base and support. Others cite the prospect of Fed rate cuts, central bank purchases and gold’s supposed lure as a hedge against negative long-term interest rates in most of Europe and Japan. We find all of this reasoning a bit suspect, just as we find all of gold’s supposed wonders a bit suspect. Gold, for all the hype, is just a commodity—not a super-asset imbued with special powers.

For fun and illustrative purposes, here is a comprehensive list of all the things that supposedly make gold a good long-term investment:

- Inflation hedge

- Deflation hedge

- Hedge against low or negative long-term interest rates

- Hedge against Fed rate cuts

- Hedge against a weak dollar

- Stability during crises

- Stability during war

- Central bank buying

- Indian holidays stoking demand

- It is shiny

Some of these overlap to a degree, but we separated them to make two points. One, to hear pundits tell it, gold is basically the CBD of the financial world: It will cure your nausea, numb your aches, help you sleep, make your hair shiny and make your complexion glow! (Just don’t ask anyone to, you know, prove it.) Two, a lot of these reasons to own gold contradict each other. In an inflationary environment, the Fed is likely to raise short-term interest rates—so if that is good for gold, then how are rate cuts also good? In a crisis, be it financial or geopolitical, the dollar usually strengthens—so how can both a strong and weak dollar be good for gold? You might as well just say interest rates and the dollar being in existence boost gold.

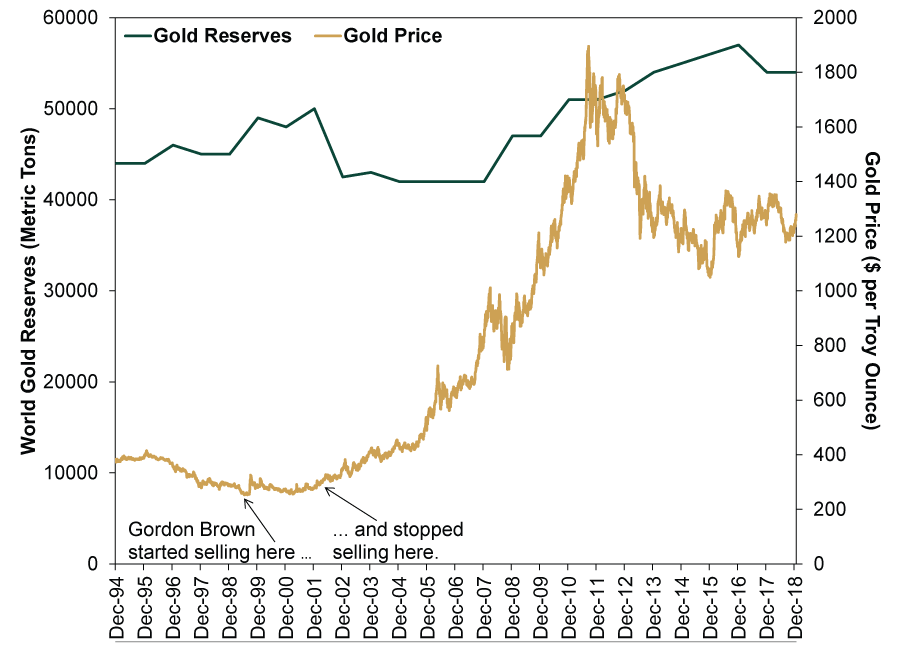

Even the reasons that don’t contradict each other don’t hold up well. If gold is so stable, then why has it had massive price swings in both directions since becoming freely traded in 1974? If central bank purchases are so good, then why did gold fall from September 2011 through the end of 2015 alongside central bank buying? Why did it soar after then-UK Chancellor of the Exchequer Gordon Brown’s infamous decision to sell off the Britain’s gold reserves in 1999 – 2002? There is a reason they call that “Brown’s Bottom,” folks. As Exhibit 1 shows, government buying simply isn’t driving the gold train.

Exhibit 1: Gold Doesn’t Much Care About Central Bankers’ Transactions

Source: FactSet, as of 6/25/2019. Annual gold reserves and daily gold price (London PM Fix), 12/31/1994 – 12/31/2018.

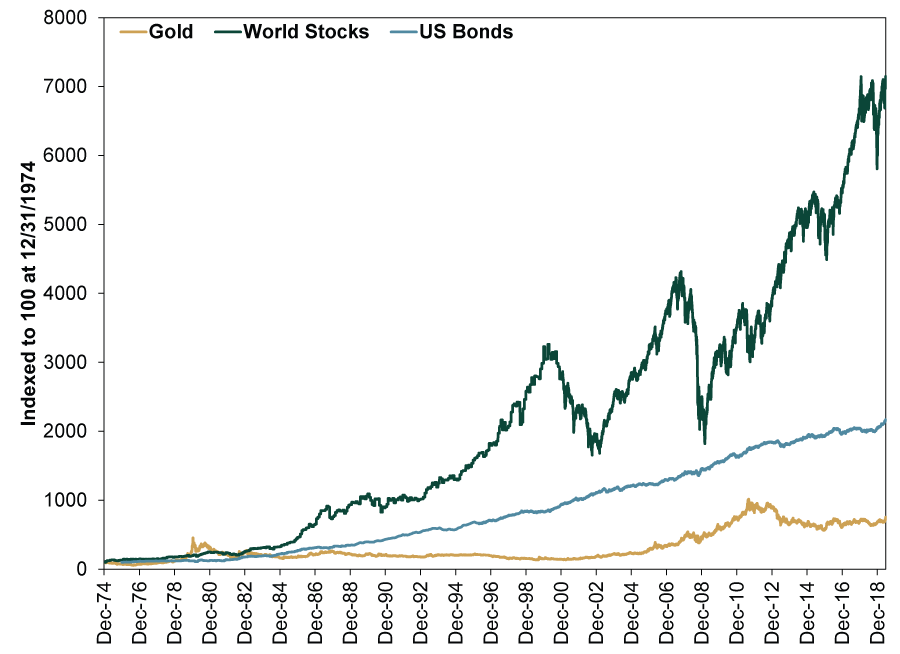

If gold were a viable long-term investment, one would reasonably expect it to have, well, done something over the long term. If not beat stocks, at least come close. You would think, especially given all the talk of gold and rates being connected, it would maybe beat bonds, too. Yet as Exhibit 2 shows, it hasn’t. Since gold began trading freely at the end of 1974, stocks have lapped it repeatedly. US bonds’ total return since the end of 1975, when our bond data begin, have more than doubled gold’s. Call us crazy, but we fail to see the point of owning gold as an investment.

Exhibit 2: Gold Isn’t That Shiny

Source: FactSet, as of 6/25/2019. Gold price (London PM Fix) and MSCI World Index with net dividends, 12/31/1974 – 6/24/2019 and US Aggregate Bond Total Return Index, 12/31/1975 – 6/24/2019.

Here, we would normally go on to explain that gold has no inherent ability to generate earnings and doesn’t pay interest or dividends—but there is a newfangled school of thought that argues this doesn’t matter, since most European and Japanese bonds don’t pay interest now, either. Yes, if one must pay the Japanese, German, French, Dutch, Danish, Swedish and Swiss governments for the privilege of lending them money for the next 10 years, a commodity with no dividends or interest might seem attractive by comparison. But that is a false choice, considering the many other fixed income options that do pay interest—like US Treasurys and UK Gilts, not to mention a vast world of investment-grade corporate debt. Plus, investors typically own bonds for their lower expected volatility. Why would a hard-swinging commodity with multiyear bear markets in its history be an effective swap? The very thought makes the whole “yield chasing” argument jump the shark.

Lest the quips and toughness in the above paragraphs suggest otherwise, we aren’t inherently anti-gold. It is pretty, and it has done well at times. However, we think it is too subject to sentiment-driven gyrations to be an effective long-term investment for folks seeking to grow their retirement assets and provide for them and their families for decades. Think about it. Would you rather invest your life savings in companies that generate profits and get new opportunities as technology advances? Or a yellow metal with limited industrial use and huge vulnerability to people’s emotional whims? Do you want something with a solid history of generating long-term returns for patient investors? Or a solid object only the greatest market timers of all time could repeatedly profit on, considering most of gold’s cumulative returns have come in short bursts?

We know which one we would pick. If you are investing for the long haul, let the commodity traders and technical analysts have their fun with gold. Central bankers, too! There are much better options for everyone else, in our view.

[i] Source: FactSet, as of 6/25/2019.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Economics Q2 US GDP’s Stealthy Strength2026-07-31

-

Expert Commentary This Week in Review | Fed Meeting, US GDP, Eurozone GDP

2026-07-31

2026-07-31 -

Market Analysis Don’t Fret the EU’s Low Summertime Gas Storage Levels2026-07-31

-

Economics On Fires and GDP2026-07-30

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today