Personal Wealth Management / Market Analysis

Why JOLTS Shouldn’t Jolt Your Economic Outlook

People are reading far too much into job openings.

Of all the economic indicators out there, the most entertainingly named has to be the JOLTS report—shorthand for the job openings and labor turnover survey. This supplemental employment release from the Labor Department has a trove of data missing in the monthly Employment Situation Report, including details on the number of job openings and how many people are resigning from their jobs versus getting pink slips. We always enjoy this report and think some of its nuggets are useful, but we are flummoxed by headlines’ reaction to the latest release, which showed job openings falling a bit but staying near record highs. One big crowd argues this is surefire evidence a recession isn’t here. The other cites the falling number of openings as a sign labor markets are cooling. We don’t think either interpretation carries much weight and urge you, dear readers, not to factor these data into your economic or market outlook.

The bullish school says the 11.3 million job openings in May—miles above the 7 million openings on the 2020 lockdowns’ eve—shows a red-hot labor market at odds with recession chatter.[i] The more pessimistic bunch points out that there were nearly 11.9 million openings in March, arguing the downtick shows businesses are cooling their jets in response to Fed rate hikes.[ii] In our view, both claims are at odds with how labor markets typically function as an economic indicator. For one, employment tends to follow economic growth, not lead it. Hiring is a big up-front investment, so businesses tend to delay it until they have reached the limit of what they can produce with current headcount—and tend to avoid layoffs until there is no other alternative, as that renders prior investment in employees a sunk cost. So you typically don’t see employment start to fall until after a recession has begun—and it usually won’t start recovering until after the ensuing economic bounce is underway. Two, the Fed started hiking in March, and most research estimates monetary policy changes take around 6 – 18 months to start bearing fruit in the real economy, making it unrealistic to think the Fed’s moves are already affecting hiring.

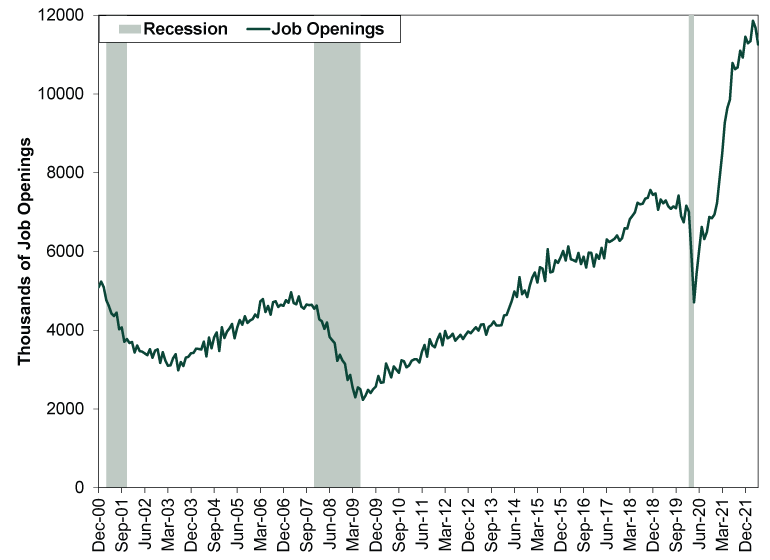

Most importantly, the JOLTS report’s very limited history doesn’t suggest job openings are predictive. Exhibit 1 shows the entire data set, which begins in December 2000, with recessions shaded. As you will see, it is normal for job openings to drift sideways or lower during a broader economic expansion. They also roll over so far in advance of a recession that they are utterly useless from a timing perspective.

Exhibit 1: Job Openings Aren’t Predictive

Source: St. Louis Federal Reserve, as of 7/7/2022. Recession dating from the National Bureau of Economic Research.

Even if you disagree with us and think employment is a leading indicator, we don’t think job openings would pass a basic logic test. Openings could fall because businesses filled positions—or because they removed job postings. Those removals could stem from cutting headcount plans because times are lean—or from an inability to find the workers they need, which leads them to invest in technology instead. Simply looking at the raw number of openings won’t tell you why those openings exist or, therefore, whether there are worrisome signs from an economic standpoint. We think that is ever true today, considering businesses’ well-documented difficulty filling positions. If job openings are down because people are returning to the workforce and helping the labor shortage ease, we imagine that is welcome news. If they are down because businesses canceled hiring plans, then we can understand why some might be pessimistic.

Then again, it shouldn’t be too hard to answer these questions by looking at May’s Employment Situation Report and ADP National Employment Report or the weekly jobless claims data from that period. Which brings us back to our initial point about all this stuff being late-lagging. All JOLTS does is put some additional color on jobs data that have been available for almost five weeks now—an eternity for stocks, which look forward. They have long since priced the economic trends that drove whatever headcount decisions employers made in May and are looking to what comes over the next 3 – 30 months. JOLTS doesn’t tell us what will happen over this stretch.

Not that we are anti-JOLTS. It has some useful tidbits. For instance, the quit rate is a handy gauge of sentiment and general business conditions. If people already have a job lined up or are confident they can get one, then the quit rate will tend to rise, making it an indicator of improving economic sentiment. That can help you get a better sense of expectations, lest you rely too much on consumer and investor surveys. Said surveys are all about how people feel in the moment. But the quit rate is about actions, which as the old maxim goes, speak louder than words. It is presently down a tick over the past few months, which seems consistent with the broader picture of escalating recession fears. That isn’t predictive, but we do think it helps put some more color on what stocks have been pricing in this year—and suggests those who say stocks are ignoring recession risk are quite wide of the mark.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Why the SOX “Bear Market” Isn’t Foreboding2026-07-21

-

Politics Blunting Burnham?2026-07-21

-

Expert Commentary 3 Things You Need to Know This Week | Q2 Earnings, ECB Meeting, Trump Accounts

2026-07-20

2026-07-20 -

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—July 13 - July 172026-07-20

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today