Personal Wealth Management / Economics

Will a Possible Trump Steel Tariff Corrode Stocks?

Talk of tariffs stokes fear of a trade war and economic downturn but are these fears overblown?

If you follow financial media lately, you might be under the impression you ought to be steeling yourself for some new protectionist measures from the Trump administration. Any day now Commerce Secretary Wilbur Ross is expected to announce findings from an investigation-permitted under Section 232 of the Trade Expansion Act of 1962-that could argue for tariffs on steel, allegedly based on national security concerns. This all plays right into longstanding fears that Trump is a trade disaster waiting to happen, triggering headlines claiming "Trump's plan to slap tariffs on steel imports carries big economic and political risks" and warning they "could set off global trade wars." But despite the sensational rhetoric, steel tariffs are nothing new and, in our view, are unlikely to live up to pundits' fears.

President Trump's positions on trade have stoked these fears. On the campaign trail, Trump was a sharp critic of trade, in particular the North American Free Trade Agreement (NAFTA) and China. He frequently said on the stump he would use executive branch powers to "protect" American jobs and specifically that he believes steel imports are "killing our steelworkers and our steel companies." (Hence, why we say Commerce's investigation is allegedly based on national security concerns.) Trump's protectionist rhetoric is a major reason why Wall Street feared him winning, and why some economists and pundits argue his policies are bad for the economy.

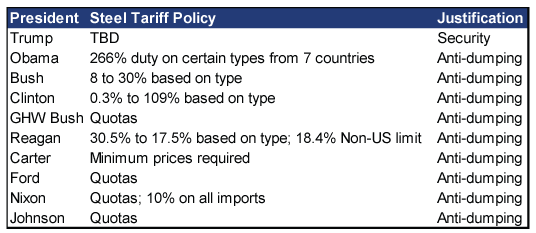

But regardless of those fears, what the Trump administration is proposing is nothing new. Basically every administration since President Lyndon Johnson has enacted some variety of steel tariff, even if the justification slightly differs now.

Exhibit 1: Presidents Like Protecting Steel

Source: National Bureau of Economic Research, as of 6/29/2017. For the record, Obama implemented steel tariffs twice (2014 and 2016). Our table cites the recent move.

So media, in hyping what Trump might do, is overlooking the fact virtually all recent presidents have done the same. Heck, we just saw this 16 months ago, when the Obama administration imposed similar tariffs on China, South Korea and five other nations.

While protectionist measures are a risk for markets, industry-specific (and usually small in scope) policies like this generally lack the scale to be bearish for broader markets. The Commerce Department reported the value of all US steel imports amounted to only 1.0% of total US imports last year. On its own, this shouldn't prove problematic for stocks. For those who want to blame China for US steel's woes, consider: China, in part due to existing tariffs, only accounts for 4% of US steel imports. Producers in Canada, South Korea, Brazil, Mexico and Japan account for a far bigger share.

Industry-specific tariff actions are fairly common and don't usually impact markets much. Why? Scale. To wallop the economy would likely take a negative worth trillions in economic activity. Getting to that scale would seemingly necessitate a broad-based trade war, the likes of which we have not seen since the 1930s, when the sweeping Tariff Act of 1930 (aka Smoot Hawley) passed. Intended to bolster agriculture, the bill wound up slapping large tariffs on hundreds of manufactured goods. Nearly 900 US imports were hit with new tariffs, and within a couple years, US imports were down roughly 40%. Now, part of that was due to generally weak global economic conditions brought by the Depression. But folks respond to incentives too, so it would be a mistake to think a tariff jacking up import prices had nothing to do with it. After Smoot Hawley, many of our major trading partners-the UK, France, Italy and Canada (our largest partner then and now)-responded with tariffs of their own. While its government stayed neutral, Swiss consumers boycotted US products.

Although it is possible steel tariffs could spur retaliation that spreads like wildfire, it is beyond a stretch to say that is probable or certain to follow whatever Commerce does. Even if the rumors of retaliation play out, the more likely outcome is a minor tit-for-tat-not an outright trade war. There just doesn't seem to be enough economic heft involved here for steel tariffs to trigger a broader downturn.

This policy shift probably would create winners and losers in a small segment of the global economy-as with any government meddling in free markets. US steel producers might notch a small, near-term win. The benefits are questionable-remember, we've seen this over and over, yet politicians still argue steel needs their "help." Consumers of steel could in theory face higher prices, which they may pass on to their customers; to the extent they have the ability to pass costs on. Producers in affected countries would suffer a bit.

But for markets, all the media hype bakes fear into stock prices, setting up a potential positive surprise. Take April's Canadian lumber saga, for example. Fears ran high when Secretary Ross unveiled a tariff on softwood imports from our northern neighbor, culminating a decades-old dispute. Many news articles presumed this was bad, but markets had oodles of time to price in opinions and fears over how bad the tariff could be. In the end, the tariff didn't live up to the fear baked into stock prices-and the stocks impacted jumped. Now, this isn't an argument to buy non-US steelmakers-the impact here was very short-lived. Our point, however, is a microcosm of how trade war fears play out.

The same thing has been happening at a macro level for much of 2017, and in our view-one reason why global and US stocks are having a nice year. For example, Mexican stocks and the peso were pounded after Trump won, due to that anti-NAFTA talk. Yet six months in, talk is much friendlier-and Mexican stocks and the peso have bounced back sharply. Moreover, according to campaign rhetoric, China should have been dubbed a currency manipulator roughly 160 days ago (on "day one") of a Trump administration. Yet here we are, and no such declaration. All these positive surprises on trade suggest fearing big fallout now is a very speculative bet. With all the media chatter about steel tariffs triggering a trade war, it seems unlikely reality matches those fears. That should be another positive surprise on trade, further bolstering global equities.

Until we get clarity from Secretary Ross, there is nothing to stop media from painting all sorts of scary what-if scenarios recalling the 1930s. But buying the hype seems unwise.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Economics On Fires and GDP2026-07-30

-

Economics Quick Hit: Durably Broad-Based Growth2026-07-29

-

Market Analysis On the Chop in the Oil Market2026-07-29

-

Politics Takaichi Raises Japan’s Wall of Worry2026-07-27

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today