Personal Wealth Management / Market Analysis

Will Emerging Markets Throw a Taper Tantrum?

Evidence suggests Emerging Markets can hold up just fine once quantitative easing ends.

Evidence suggests Emerging Markets’ party won’t stop when the Fed pulls the punchbowl. Photo by Feng Li/Getty Images.

Since Ben Bernanke suggested the Fed might soon wind down quantitative easing (QE), folks have fretted the potential impact on Emerging Markets (EM). Many believe massive amounts of “hot money” have flowed from the US and UK into EM assets since QE began (November 2008 for the US, March 2009 for the UK), and they fear QE’s end will prompt massive capital flight, hurting EM economies and cutting into revenue streams globally as a result—potentially triggering a bear market. Yet evidence suggests this fear is overwrought, and Emerging Markets should hold up ok once QE ends.

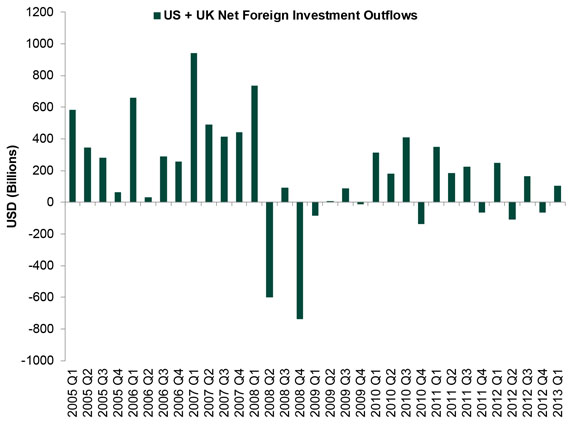

For one, data don’t support the notion of hot money from QE nations pouring into EM. As Exhibit 1 shows, the US and UK’s combined net investment outflows since QE began are far below pre-QE levels. What capital has flowed out needn’t automatically retreat once QE ends. It took a severe financial crisis to cause the last huge pullback—and QE’s end isn’t crisis fodder. In fact, it should be an economic and financial tailwind, as it allows the yield curve to steepen. That’s likely a large reason why UK economic data have accelerated since the BOE stopped purchasing assets in late 2012.

Exhibit 1: US Plus UK Foreign Investment Net Outflows

Source: Bureau of Economic Analysis, Office for National Statistics, as of 7/9/2013.

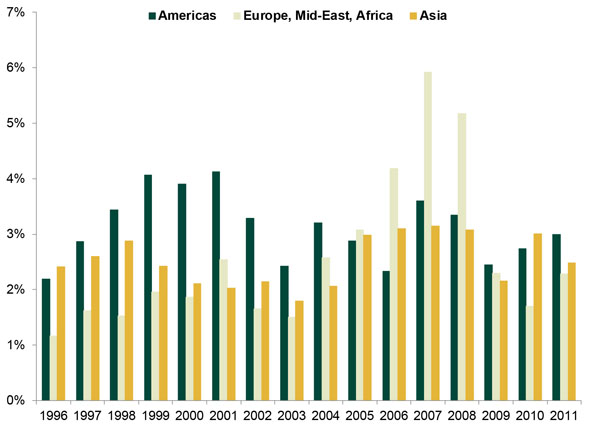

Plus, even when investment outflows from the US and UK plummeted in 2008, EM still saw strong net inflows, suggesting they could still attract plenty of capital from other areas even if US and UK investors were to retreat some. (Exhibit 2)

Exhibit 2: Emerging Markets Foreign Investment Net Inflows, by Region

Source: World Bank, MSCI as of 7/9/2013. Americas includes Brazil, Chile, Colombia, Mexico and Peru. Europe, Middle East and Africa includes Czech Republic, Egypt, Greece, Hungary, Poland, Qatar, Russia, South Africa, Turkey and United Arab Emirates. Asia includes China (including Taiwan), India, Indonesia, Korea, Malaysia, Philippines and Thailand.

Some say the real pain will come from investors globally—particularly institutional investors—moving from EM assets and development projects to higher-yielding US assets once interest rates rise. Some investors could very well chase US yields, but they likely won’t fully flip from EM to the US. For one, the theory assumes institutional investors have moved huge sums from low-yielding sovereigns to higher-yielding assets in recent years. No doubt some have, but EM assets aren’t the only, or even necessarily the biggest, recipients. Funds have also flowed to US infrastructure projects, which typically have similar risk profiles as US Treasurys, investment-grade corporate bonds and other comparable assets.

That’s no accident. Most institutional funds have strict bylaws stipulating how they invest, with each bucket of money assigned a certain risk profile and/or geographic/stylistic mandate. Moving funds from the developed world to EM assets likely would have required firms to adjust their mandates. Ditto for moving out of EM looking forward. This is typically a very long process—one most firms won’t undertake just for shorter-term plays. Institutions, like many individual investors, typically have very lengthy investment time horizons, and their strategies depend on their long-term objectives, not short-term bets.

Of course, this fear assumes foreign capital is vital for EM equities and economies—but it’s not. It does contribute some to growth, but overall and on average, federal and private domestic investment are more important. EM nations have created significant wealth, and much of that wealth underpins continued growth. That’s largely how Emerging Asia’s net foreign inflows have stayed low relative to GDP even as they’ve grown in absolute terms (Exhibit 3). Higher growth simply begets new investment opportunities for foreigners.

Exhibit 3: Emerging Markets Foreign Investment Net Inflows/GDP

Source: World Bank, United Nations Statistics Division, as of 7/10/2013.

Most EM nations—especially in Asia and the Americas—also have positive current accounts, providing extra insulation from departing foreign capital. Foreign outflows can get dicey in a fixed exchange rate regime, but few remain after the late-1990s Asian Currency Crisis. China does have a fixed float, but it also has strict capital controls, limiting the risk of fund flight, and $3.4 trillion in forex reserves.

Finally, for QE tapering to have a real impact on EM growth, I’d expect the reverse to be true—whopping economic growth since QE began. But it’s not! Brazil, China, India, Korea, Mexico and Peru have slowed since 2010. Malaysia and Indonesia have stayed firm but not accelerated. So many other variables impact growth in these nations, and these factors will continue influencing their economies after QE ends. With QE’s existence not a huge positive driver, its end is likely similarly immaterial.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis On the June Inflation Cooldown2026-07-14

-

Expert Commentary 3 Things You Need to Know This Week | US Inflation, China GDP, US Retail Sales

2026-07-13

2026-07-13 -

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—July 6 - July 102026-07-13

-

Expert Commentary This Week in Review | Global PMIs, SpaceX, RMD Planning

2026-07-10

2026-07-10

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today