Personal Wealth Management / Behavioral Finance

You Get What You Pay For

Index funds have many fine features, but they can’t help investors fight the biggest stumbling block to long-term success: emotion.

What’s the secret to long-term investment success?

According to the godfathers of passive investing, it’s simple: Pay as little as you can for something that mirrors the market’s return. As if investing is as simple as walking into the store, seeing shelves full of products offering a given long-term annualized return, and picking the one with the lowest fee relative to its long-term return (and having it magically match your long-term goals, objectives, cash flow needs and time horizon, but that’s a topic for another day). Or, in their own words:

“You can't control what markets can do, but you can control the costs you pay. The less you pay to the purveyors of investment services, the more there will be for you. The quintessential low-cost investment vehicles are index funds, which should comprise the core of every investment portfolio. The high fees charged for active management cannot be justified.” –Burton Malkiel, writing in The Wall Street Journal

“Whether markets are efficient or inefficient is beside the point. The cost matters hypothesis is all that is needed to explain why indexing works: gross return in the market as a whole, minus the costs of obtaining that return, equals the net return investors actually receive.” –Jack Bogle, writing in Financial Times

In other words, buy a cheap index fund, kick back, relax and enjoy outperforming all the supposed suckers who fall for active management. It’s a fine theory, but as ever, theory isn’t reality. And as with anything that sounds too good to be true, there is a problem. It assumes the only thing you pay for is a strategy’s return—while ignoring the many other variables that will determine your own return. Including the biggest variable of them all: Yourself. The low fee you pay for an index fund won’t help you there.

I won’t quibble with any of the studies showing passive investments outperform most active investments. I will quibble with the notion using these passive products guarantees success. Time and again, investors fail at this exercise—the investments are passive, but the investors aren’t. They’re active! They trade often and at precisely the wrong times.

Whether you’re using passive products, mutual funds, active management or just picking stocks on your own, success takes discipline—steeling yourself against the emotional impulses to trade when markets are volatile. Study after study shows investors’ biggest enemies are their own psyches. Index-fund investors are no less vulnerable than anyone else. The more volatile stocks are, the more they trade.

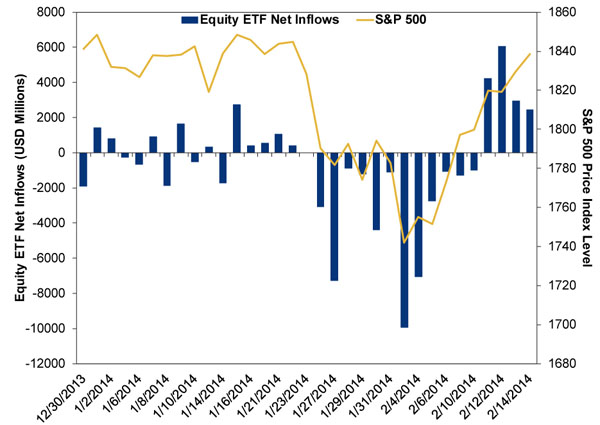

Consider how they’ve behaved since late January—one of the more volatile stretches we’ve seen in a while. As stocks fell, folks yanked money out. On February 3, as the S&P 500 fell -2.3%, investors pulled nearly $10 billion from equity ETFs—the biggest outflows came during the biggest drop. Folks kept pulling money over the next five days, even as stocks recovered.

Exhibit 1: Equity ETF Net Inflows & S&P 500, 12/30/2013 – 2/14/2014

Source: ETF.com, Federal Reserve Bank of St. Louis, as of 2/18/2014. Daily ETF flows not available for 1/23/2014 due to the Lunar New Year holiday.

Sell out during one blip and it’s not so bad—not as long as you get back in quickly, learn your lesson and stay disciplined from then on. But many investors do this over and over, during corrections and not-quite corrections. They sell when the going gets rough, assuming the downside of a few days or weeks will carry forward indefinitely. They forget stocks aren’t serially correlated, and what goes down has a better than 50% chance of going up the next day. They wait until things look better—until a seemingly stable recovery is in place—before they get back in. Again and again, folks sell low and buy high—and over time, the transaction costs and missed upside take a big bite out of their long-term return, putting their financial goals at risk.

Passive products don’t come with a magic pill to turn you into a passive investor. Owning an index fund won’t turn you into a robot or a carefree person who never even thinks to check on the market. If you use index funds, you still face all the same struggles, temptations, fear and greed you face with mutual funds and individual stocks. You just own different securities. They’re passive. You aren’t.

This is why folks pay for investment advice when they could just buy a cheap index fund—why they find the service valuable and worth the cost. When you hire an adviser, assuming they have a vested interest in helping you reach your goals rather than simply taking orders, you hire someone to help you stay disciplined when markets wobble and remind you of your long-term goals. To remind you of the risks of selling at the first sign of a drop, remind you dips and corrections are over before you know it, and remind you that if nothing in the market environment has fundamentally changed, it’s probably not the time to sell. Yes, that advice probably costs a bit more per year than an index fund, but the potential impact on your long-term return is unquantifiable.

The simple cost/return analysis touted by the index fund braintrust misses this. It’s binary. But life isn’t binary! You aren’t binary! A proper cost/benefit analysis of any investment product or strategy should at least try to account for the many intangible factors that determine whether or not it helps you reach your long-term goals.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23 -

Economics A Summertime Check-in on US Consumers2026-07-23

-

Market Analysis Why the SOX “Bear Market” Isn’t Foreboding2026-07-21

-

Politics Blunting Burnham?2026-07-21

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today