Personal Wealth Management / Market Analysis

Your Obligatory Tariff Update

Even with the latest developments, the trade spat with China likely remains too small to wallop the bull market.

The Trump administration’s ongoing trade spat with China went another few rounds in recent days, spooking investors as headlines once again framed the issue with big numbers. Some previously threatened tariffs are now scheduled to take effect on July 6, and if the administration makes good on its latest threat, more may be in the offing. Yet our view is unchanged: Even with the latest developments, the scope and impact of all tariffs implemented or threatened thus far remains too small to derail the US, Chinese or global economies—or wallop the bull market.

The latest tit-for-tat started last week, when the US government released the list of Chinese goods (primarily industrial products benefiting from the “Made in China 2025” policy) that will be subject to 25% tariffs. Lost in most media coverage, however, was that tariffs on only $34 billion in goods are expected to take effect by July 6. The remaining tariffs on $16 billion worth of goods (largely related to semiconductors) likely face another round of hearings before implementation. In response, China’s government immediately provided further detail about its retaliatory tariffs on $50 billion of US goods. Mirroring the US’s approach, tariffs on only $34 billion in goods (mostly agricultural goods and autos) are scheduled for implementation on July 6, with the adoption of tariffs on the remaining $16 billion (largely energy products, chemicals and medical equipment) to be determined.

This week, in retaliation against China’s retaliation, President Trump replaced his prior April threat of a 25% tariff on an additional $100 billion in Chinese goods with an order to draw up plans for 10% tariffs on $200 billion in Chinese goods. If these take effect, a total of $250 billion in goods would be subject to tariffs. Since the US exports only about $130 billion in goods to China, the Chinese government can’t respond with an equivalent threat. Consequently, Beijing said it will respond with both quantitative and qualitative measures, which presumably means a combination of import tariffs and regulatory actions against US companies operating in China.

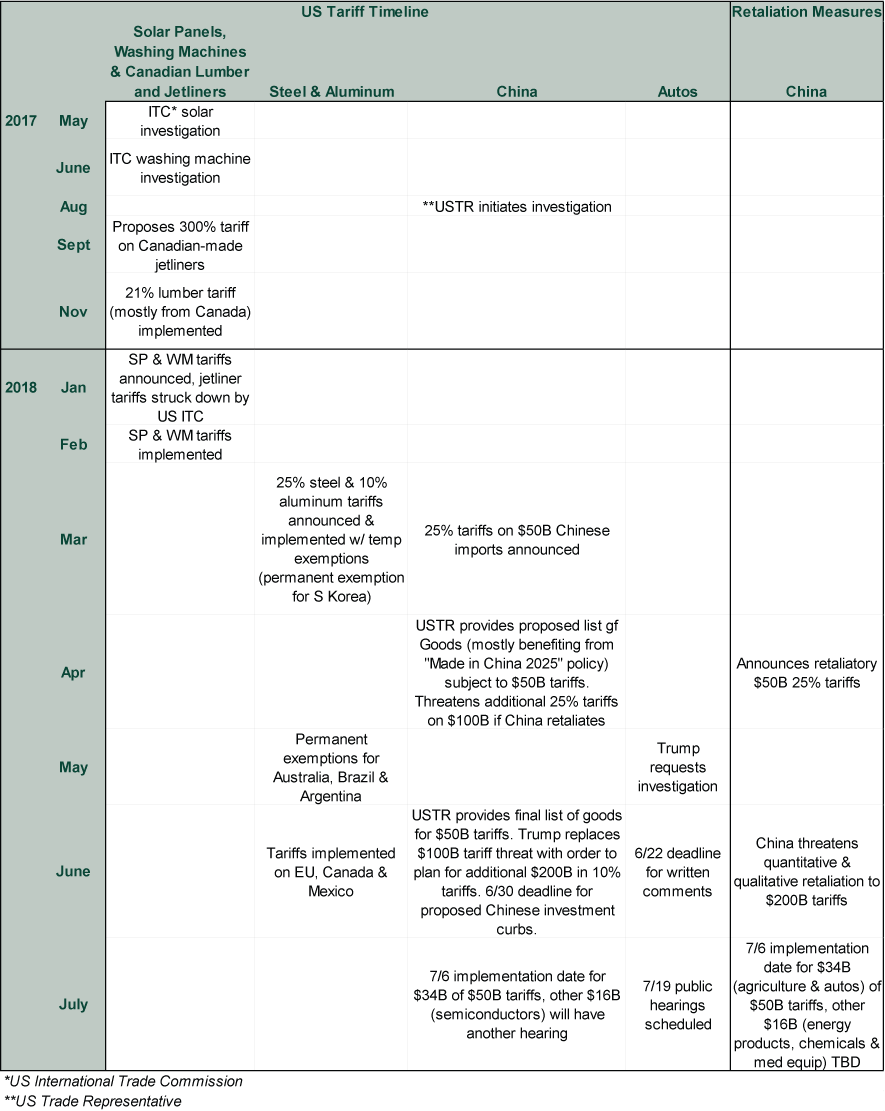

While not completely comprehensive, Exhibit 1 chronicles the major tariff-related events of the Trump administration along with Chinese retaliation. Last year and early this year, the administration implemented a variety of small tariffs on solar panels (30% rate applying to about $4.5 billion in imports), washing machines (20 – 50% rate applying to about $1 billion in imports) and Canadian lumber (21% rate on $5.6 billion in imports). These tariffs are in effect, but a US International Trade Commission (ITC) panel struck down a 300% tariff on Canadian jetliners. On the steel and aluminum front, these metal tariffs launched in March on a small scale due to major exemptions. However, after the temporary waivers expired, the tariffs hit the EU, Canada and Mexico on June 1. Overall, these tariffs currently apply to roughly $40 billion in imports. As mentioned above, tariffs on China aren’t in effect yet, but the initial tariffs on $34 billion are scheduled to take effect July 6. A few weeks later, public hearings about potential auto tariffs will occur. Apart from President Trump’s tweet threatening 20% tariffs on EU auto imports, the details about potential auto tariffs are vague, but the US imported $192 billion worth of vehicles in 2017 that could potentially be subject to tariffs.

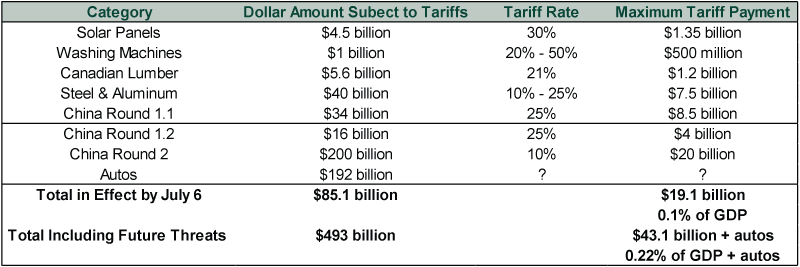

All told, presuming the July 6 implementation goes ahead as scheduled, the Trump administration will have applied new tariffs to approximately $85 billion worth of goods, representing 2.9% of imports and 0.4% of US GDP—tiny.[i] The future threats don’t change the calculus dramatically for the worse. If the tariffs on the remaining $16 billion of those initial $50 billion in Chinese imports, the additional $200 billion in imports and a theoretical $192 billion of auto imports were to take effect, the total goods subject to tariffs would be roughly $493 billion—16.9% of US imports and 2.5% of US GDP. Yet even these scaled figures probably overstate the impact. Applying tariffs to 2.5% of GDP doesn’t automatically delete that economic activity. Rather, it adds taxes that consumers or businesses must pay. The amount of those tariff payments, as Exhibit 2 shows, is much smaller than the big numbers being thrown around—amounting to less than half a percent of GDP, which is nowhere near large enough to spark a recession in the US or global economy or knock the bull market off course. A true wallop requires shocking, huge measures capable of wiping trillions of dollars off the global economy. Tariffs, though a small negative, don’t come close.

Exhibit 1: A Brief History of Tariffs

Source: US Trade Representative and China Ministry of Commerce, as of 6/19/2018.

Exhibit 2: Scaling the Tariffs

Source: US Trade Representative, China Ministry of Commerce, the American Action Forum and US BEA, as of 6/20/2018. Based on nominal GDP in 2017.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Economics Quick Hit: Durably Broad-Based Growth2026-07-29

-

Market Analysis On the Chop in the Oil Market2026-07-29

-

Politics Takaichi Raises Japan’s Wall of Worry2026-07-27

-

In The News Why Kevin Warsh should think twice about hiking interest rates — even as anxiety over the Iran war grows2026-07-27

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today