Personal Wealth Management / Economics

What to Make of November’s Dreary US Data

In our view, downbeat data to end the year don’t tell you where things are going next year.

What to make of the US economy? Sentiment measures and many financial commentators we follow portray conditions as quite bad. In our view, the latest economic data are mixed, with two of this year’s stronger American indicators potentially showing some cracks in November. In our experience, the consensus view amongst commentators we follow is: Things aren’t good and are about to get worse, with many pencilling in an American recession (a period of contracting economic output) next year. We won’t deny that a recession is possible. But from an investing perspective, we don’t think a US recession is an automatic market negative, as our research suggests stocks care more about how expectations align with reality. In our view, the popular reaction to the latest November data suggests positive surprise may not be hard to achieve.

Starting with the “Personal Income and Outlays” report, where the US Bureau of Economic Analysis (BEA) announced real (i.e., inflation-adjusted) personal consumption expenditures (PCE) were flat in November, stalling after October’s 0.5% rise.[i] Goods spending fell -0.6% m/m whilst services spending ticked up 0.3%.[ii] PCE price indexes showed inflation slowed, as headline prices rose 5.5% y/y following October’s 6.1%.[iii] November was headline PCE’s first month below 6% since January this year, continuing the deceleration since June’s high of 7.0% y/y.[iv] A big factor: energy prices’ ongoing slowdown. Though PCE energy goods and services prices continued rising at double-digit rates (13.6% y/y in November after October’s 18.4%), they have decelerated considerably from June’s 43.6% clip.[v] But energy prices aren’t the only ones slowing, as core PCE prices (which exclude energy and food) eased to 4.7% y/y from last month’s 5.0%.[vi]

Separately, the US Census Bureau announced November durable goods orders fell -2.1% m/m, a reversal from October’s 0.7%.[vii] The widely watched nondefense capital goods orders (excluding aircraft)—also known as core capital goods orders and which corresponds to the equipment segment of business investment—rose 0.2% m/m.[viii] Several commentators we follow had a similar take on all these data: Inflation may be easing, which is positive, but consumer spending and business demand are softening, which is bad.

In our view, November’s figures do imply some weakness. Take durable goods orders, which our research suggests are typically volatile from month to month. Ever since the US reopened from COVID lockdowns, they have steadily climbed, which we find rather unusual.[ix] But orders aren’t adjusted for inflation, so higher prices may have been masking the state of demand for a while. Another way to see this: Manufacturing of durable consumer goods—which is inflation-adjusted—has fallen in 5 of the last 7 months, whilst real consumer spending on durable goods is down in 7 of the past 12.[x] If slowing inflation allows weaker demand to be more evident in falling durable goods orders—provided they keep falling from here—we think that could counterintuitively give investors more clarity and ease the uncertainty inherent in a long run of mixed data.

But we think that is a big IF, and not just because less-volatile core orders grew whilst non-defense aircraft orders were the primary drag on headline orders.[xi] In our view, November’s PCE report put a spotlight on one of the primary drivers of weak durable goods output: autos. Yes, on the surface, the popular takeaway might seem correct—resilient services spending, coupled with falling goods consumption, suggest higher prices are weighing on some discretionary outlays. Most services are essential, after all, which we think is a big reason consumer spending tends to fluctuate much less during recessions than financial commentators we follow presume.[xii]

But the main drag on goods spending—in November as well as much of the year—was motor vehicles & parts, which fell -4.3% m/m last month.[xiii] Autos have been quite volatile since COVID lockdowns, which spurred supply shortages first as factories closed, then as semiconductors were scarce.[xiv] Auto shortages pushed prices far higher—one of 2021’s biggest inflation contributors—and drove up prices for used cars as well.[xv] If higher prices are now regulating demand in the face of tight supply, we don’t think that is necessarily a bad thing. Rather, it is a sign market fundamentals are reasserting themselves and probably aiding a return to normal, in our view. More importantly, we think it probably also signals heavy industry and consumption aren’t uniformly weak—instead, they may look worse than they are due to one noisy category.

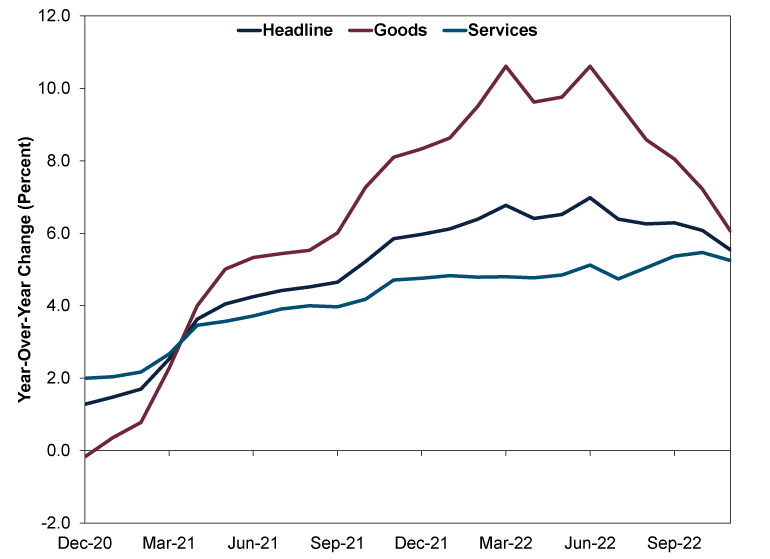

More positively, the price trends we highlighted earlier this month continued in November: goods prices kept slowing whilst services prices remained at similar levels from the past couple months.[xvi] To be sure, US inflation rates remain elevated.[xvii] But as supply and demand come into better balance, we think they will likely continue to ease. (Exhibit 1)

Exhibit 1: Ongoing Moderation in PCE Prices

Source: FactSet, as of 17/12/2022. PCE Price Indexes, Headline, Goods, and Services, year-over-year percentage change, December 2020 – November 2022.

Perhaps supporting the view things are more positive than perceived: The Atlanta Federal Reserve’s GDPNow, a mash up of actual incoming data that constitute gross domestic product (GDP, a government-produced measure of economic output) and estimates of data to come. The bank now expects Q4 GDP growth to be 3.7% annualised.[xviii] That is higher than December 20’s 2.7% estimate and a rebound from Q3’s -0.6% annualised contraction.[xix] Why the one-percentage-point jump? Based on latest data, the estimate for real gross private domestic investment flipped from a -0.2% annualised contraction to 3.8% growth.[xx] That may seem strange, considering the main data releases that feed into this weren’t fantastic, in our view. But it likely means the Atlanta Fed’s modelling was perhaps too negative initially—which we think encapsulates howmarkets work. Our research suggests even a dreary reality can be a positive surprise if expectations are low enough.

In our view, markets care less about whether the US enters recession and more about how reality aligns with expectations. In our experience, the general consensus for the US economy next year appears to be either a soft landing (i.e., a slowdown) or a mild recession—so we suspect it is unlikely a moderate downturn would pack much negative surprise power. If anything, the confirmation of recession may allow people to move on. And if reality turns out a bit better than projected? In our view, even tepid growth can positively surprise and provide some relief.

[i] Source: FactSet, as of 23/12/2022. Inflation refers to broadly rising prices across the economy.

[ii] Ibid.

[iii] Ibid. The PCE price index is a government-produced measure of goods and services prices. It is also the US Federal Reserve’s preferred inflation gauge and the indicator on which it bases its inflation target.

[iv] Ibid.

[v] Ibid.

[vi] Ibid.

[vii] Ibid.

[viii] Ibid.

[ix] Source: US Census Bureau, as of 30/12/2022. Durable goods orders, January 2021 – November 2022.

[x] Source: FactSet, as of 29/12/2022.

[xi] See note i.

[xii] Source: US BEA and National Bureau of Economic Research (NBER), as of 30/12/2022. Statement based on BEA quarterly GDP and consumer spending levels and NBER recession dates, Q1 1947 – Q3 2022.

[xiii] See note i .

[xiv] “The Chip Shortage Could Be Just About Done Pummeling the Auto Industry, Experts Say — So Cars May Get a Whole Lot Cheaper in 2023,” Alexa St. John, Insider, 5/12/2022.

[xv] Source: US Bureau of Labor Statistics, as of 30/12/2022. Month-over-month percent change in used car prices, January 2021 – December 2021.

[xvi] Source: FactSet, as of 30/12/2022.

[xvii] See note i.

[xviii] Source: Atlanta Federal Reserve, as of 23/12/2022.

[xix] Ibid.

[xx] Ibid.

Get a weekly roundup of our market insights.

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Markets Are Always Changing—What Can You Do About It?

Get tips for enhancing your strategy, advice for buying and selling and see where we think the market is headed next.

Related Resources

-

Macro Insights Q1 2026 Global Markets Review & Outlook2026-05-12

-

Macro Insights Why Global Small Cap2026-05-07

-

Market Analysis What to Think of Another Aussie Rate Hike2026-05-05

-

Market Analysis Europe’s Resilient Q1 GDP2026-05-01

Contact Us

Learn why 200,000 clients trust Fisher Investments and its affiliates to manage their money and find out how we may be able to help you achieve your financial goals.

As of 31/03/2026. Includes Fisher Investments and its affiliates.

New to Fisher? Call Us.

Contact Us Today