Personal Wealth Management / Market Analysis

A Quick Look at Sentiment’s January Surge

January’s jump in US consumer sentiment adds to a longer-running trend.

Headlines are heralding the big January jump in the University of Michigan’s (U-Mich) widely watched consumer sentiment measure, which rose to its highest level since 2021—the second-straight sharp rise and biggest monthly gain since 2005. The survey’s director said warming sentiment would “provide some positive momentum for the economy.” We are bullish and think the US economy’s prospects are solid, but this viewpoint is a stretch, in our view. Sentiment surveys may provide a look at where sentiment is at a given moment, but their forward implications are limited. The latest data are a case in point.

The U-Mich consumer sentiment gauge soared 13.1% m/m in January’s preliminary estimate, as all five index components rose—led by the short-run outlook for business conditions (27% m/m).[i] Over the past two months, the index climbed a cumulative 29%, the biggest two-month jump since 1991, and improvement was broad demographically and politically (Democrats and Republicans reported their most favorable readings since the summer of 2021).[ii] People are also more optimistic on inflation: Respondents think inflation will be 2.9% higher 12 months from now, the survey’s lowest reading since December 2020.[iii]

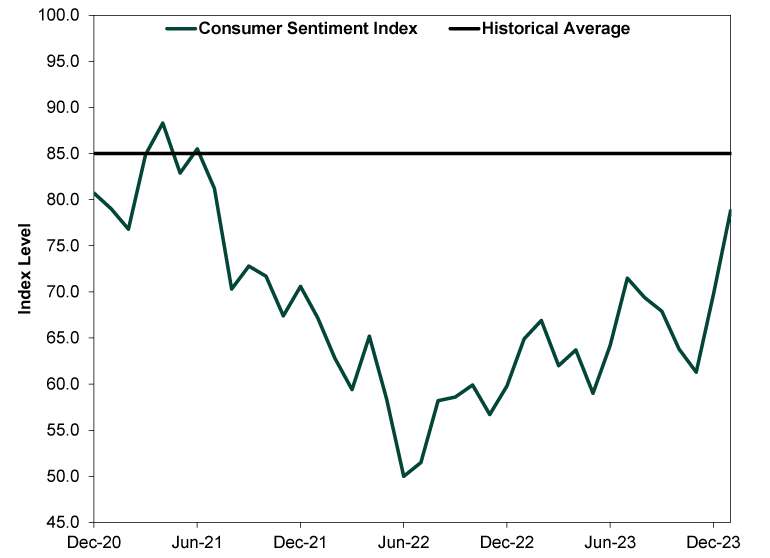

Those hyperfixating on the last two months’ sharp gain miss a broader point: The U-Mich gauge’s headline reading and underlying subindexes have shown material improvement over the past year. The headline index gets the most attention and is clawing its way back to its long-term average. (Exhibit 1)

Exhibit 1: Headline U-Mich Consumer Sentiment Index, December 2020 – January 2024

Source: University of Michigan, as of 1/19/2024. Long-term average based on average monthly reading, January 1978 – January 2024.

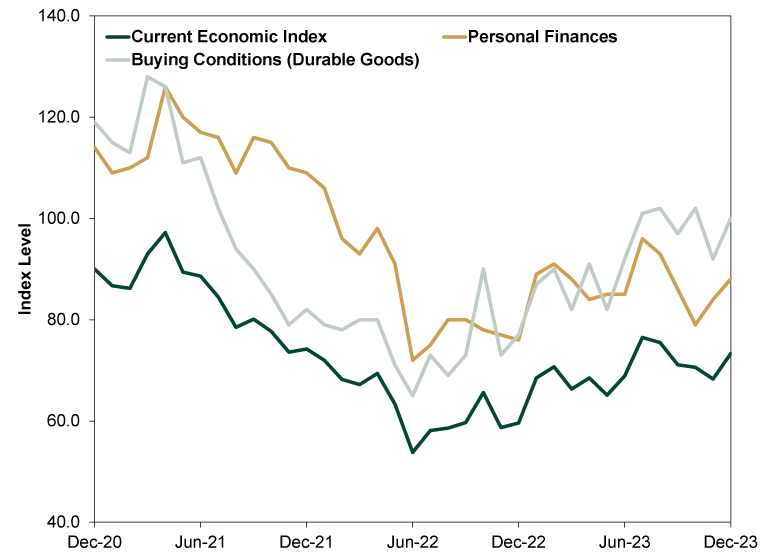

The survey’s subindexes show similar improvement. Respondents' views of the current economic situation (both of their personal finances and general buying conditions) have also improved since June 2022. (Exhibit 2)

Exhibit 2: Current Views of Economic Conditions, December 2020 – January 2024

Source: University of Michigan, as of 1/19/2024.

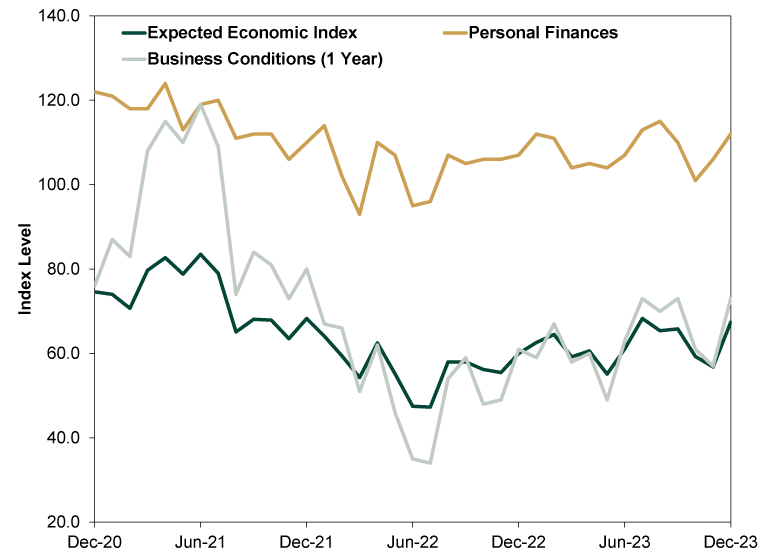

Moreover, as Exhibit 3 shows, future expectations have rebounded over the same timeframe (albeit, more modestly).

Exhibit 3: Expected Views of Economic Conditions, December 2020 – January 2024

Source: University of Michigan, as of 1/19/2024.

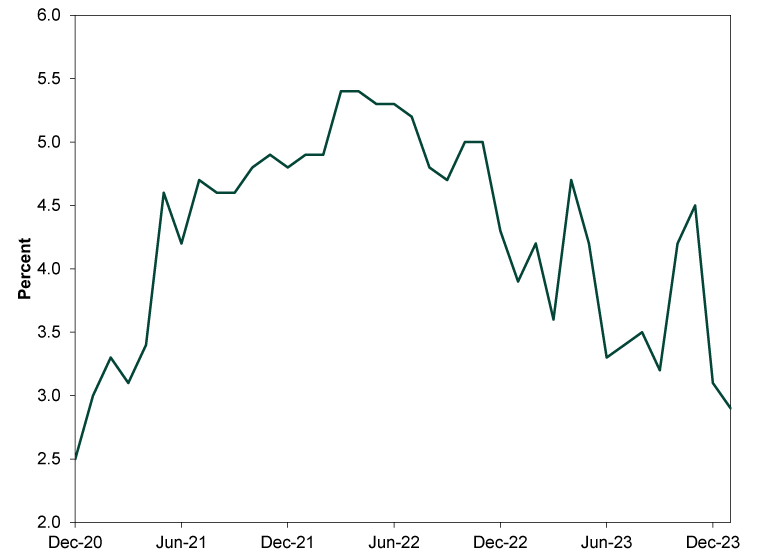

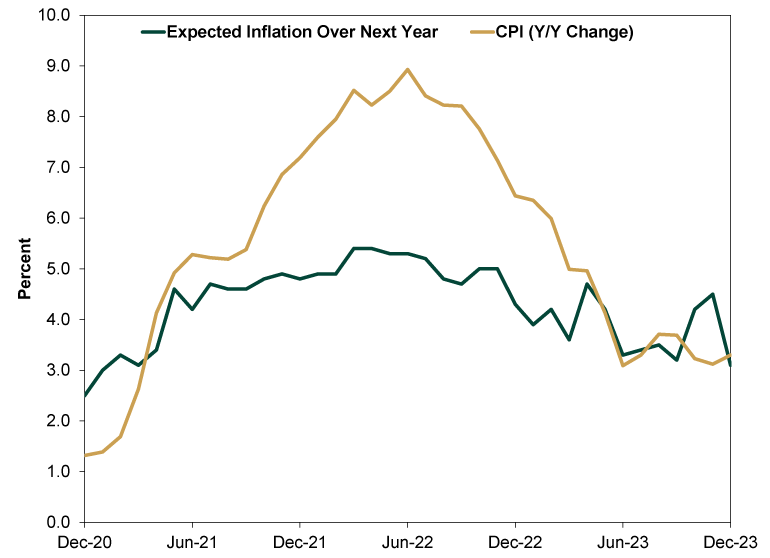

Another way to see this: falling expectations in expected annual inflation. After peaking at a 5.4% y/y rate in April 2022—as elevated prices dominated headlines—survey respondents’ expected price changes have trended downward. (Exhibit 4)

Exhibit 4: Expected Change in Inflation Rate Over Next Year, December 2020 – January 2024

Source: University of Michigan, as of 1/19/2024.

The U-Mich survey’s January pop has stoked chatter that brighter moods will buoy growth. Since people are feeling more chipper about the economy, the thinking goes, they will be more willing to spend (thereby supporting growth). But in our view, sentiment follows or, at best, coincides with economic growth. Said another way, moods aren’t a leading economic indicator.

See how survey respondents’ inflation views tracked with actual inflation over the past three years. As Exhibit 5 shows, consumers didn’t anticipate hot inflation in 2021 and 2022 and then prices soared. Nor did they think inflation would slow starting in mid-2022, and then it magically happened. Rather, expectations followed the disinflation trend.

Exhibit 5: Expectations Don’t Lead Reality

Source: University of Michigan and FactSet, as of 1/19/2024.

We think the improvement in sentiment makes sense. With inflation moderating and other data suggesting economic fundamentals are better than appreciated going into this year, some long-running investor worries may be losing some power—and that relief can boost moods. But improved moods don’t tell you where spending or economic activity are headed. We won’t necessarily see some sharp acceleration merely because consumers say they feel better.

To us, the chief takeaway from all this: Folks aren’t as pessimistic as they were. They still don’t seem rosy or even optimistic—especially with so many thinking the economy and markets depend on future Fed rate cuts. Some also warn the S&P 500’s run to records is hollow. That suggests a smaller-but-still-bullish gap between reality and expectations remains.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

See Our Investment Guides

The world of investing can seem like a giant maze. Fisher Investments has developed several informational and educational guides tackling a variety of investing topics.

Related Resources

-

Market Analysis Market Perspective on the Data, Jobs and Debate Over July’s Employment Report8/1/2025 12:00:00 AM

-

Expert Commentary This Week in Review | Tariff News, US Jobs Data, GDP Insights, Q2 Earnings (Aug. 1, 2025)

8/1/2025 12:00:00 AM

8/1/2025 12:00:00 AM -

In The News The Omnibus Trade News Roundup You Need8/1/2025 12:00:00 AM

-

Market Analysis Episode V: The Meme Stocks Strike Back7/31/2025 12:00:00 AM

Learn More

Learn why 185,000 clients* trust us to manage their money and how we may be able to help you achieve your financial goals.

*As of 6/30/2025

New to Fisher? Call Us.

Contact Us Today