Personal Wealth Management / Market Analysis

After the Shortest Bear Market Ever, How Long Can the Bulls Run?

A bear market’s length doesn’t predict how far the next bull market will run.

How long can this bull market last? That is a question we hear often, with the common presumption now being that the shortest bear market of all time, followed by the shortest-ever recovery to prior highs, must mean this will be a short bull market. Perhaps that is doubly true, considering this cycle has acted more like an oversized correction than a traditional bear market—and it all follows history’s longest bull market. But in our view, there is no realistic way to assess how long this bull market will last—you must assess conditions as they evolve. One thing, however, is clear: Age and the prior bear market’s length don’t really mean anything. All bull markets end one of two ways: when investors have run out of worries and developed irrationally high expectations, or when something wallops the expansion before its natural peak.

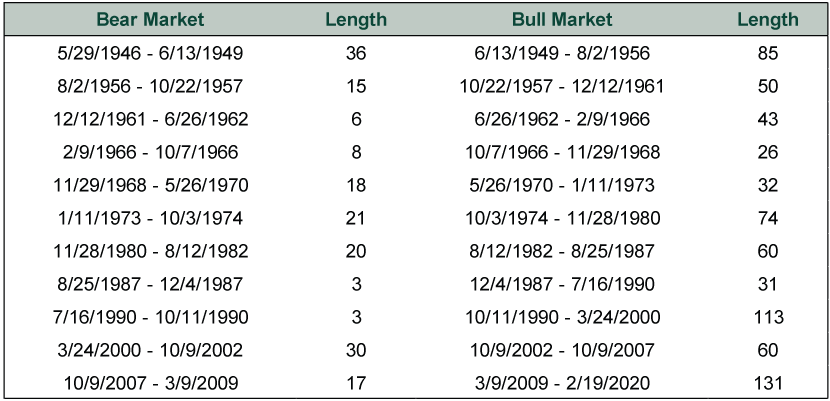

Exhibit 1 shows the length of every S&P 500 bear market—and ensuing bull market—since WWII ended. As you will see, short bear markets don’t mean much. Prior to 2020, the two shortest bear markets on record were 1987’s and 1990’s. The bull market that followed 1987’s crash was relatively short at 31 months. But 1990’s bear market was almost exactly as short. The bull market that followed the second was the 1990s’ boom—at 10 years, it is history’s second-longest. One short, one long, no pattern.

Exhibit 1: S&P 500 Bear and Bull Market Lengths (in Months)

Source: Global Financial Data, Inc., as of 3/24/2020. Length is rounded to the nearest whole month.

The bull markets above came in all shapes and sizes, but all ended in one of the two ways: either when euphoria made expectations unattainable or when hit by a huge, unseen negative. In March 2000, August 1987 and most others, euphoria ruled the day. Investors generally figured the party would last forever, and they overlooked or explained away any indicators hinting at negativity ahead. March 2000 was the height of the dot-com boom—the new economy, when boom and bust were declared dead and pundits sought new terms for economies that only grew. With Y2K having come and gone, many thought the coast was clear for more Tech-led economic growth and bull market. They overlooked the declining Leading Economic Index and inverted yield curve, not to mention the flood of IPOs by companies with no profits, no sound business plan and deep operating losses. Euphoria blinded investors to all of these, and a bear market began.

Bull markets that didn’t end in euphoria ended when a huge negative burst on the scene, surprised the world and walloped the global economy hard enough to knock a few trillion dollars off GDP, rendering recession. In October 2007, it was the imposition of mark-to-market accounting to illiquid assets banks never intended to sell, forcing them to take paper losses whenever a hedge fund or other entity sold similar holdings at fire-sale prices. That vicious cycle of writedowns and fire sales eventually transformed about $200 billion worth of actual loan losses into nearly $2 trillion of exaggerated and unnecessary writedowns. In this year’s bear market, the wallop was the global lockdown aimed at containing the spread of COVID-19, which caused the deepest and most rapid economic contraction in modern history.

For something to qualify as a wallop, it must be huge—trillions of dollars’ worth of huge—and surprising. The myriad alleged negatives percolating through financial headlines today don’t count, in our view, because they are either too small, too unlikely or too well-known. These aren’t wallops in waiting, but the first bricks in this bull market’s wall of worry. As for sentiment, we think most of the investment community is still waiting for the other shoe to drop, not envisioning perma-expansion.

If you are investing for long-term growth, the above is really all you need to know when it comes to deciding whether to own stocks. If you aren’t in a bear market, you are in a bull market, and capturing bull market returns is vital to achieving market-like returns over time. Whether this bull market expires in two years, three or more shouldn’t make any difference to your asset allocation today. Taking defensive positioning when you are actually early in a bear market can be beneficial, but we don’t think the day to make that decision is when stocks close at an all-time high. This year’s notwithstanding, the vast majority of bear markets roll over slowly, giving investors time to assess the situation carefully and avoid knee-jerk decisions.

So rather than sweat now about how long this bull market might last, just live in the moment while keeping your eye on your long-term goals. If you are in a diversified portfolio tailored to your needs and time horizon, take heart in knowing that stocks’ long-term returns include all bull and bear markets along the way. While we think it is prudent to watch for signs a bear market may be underway, trying to date a bull market’s end before you see them is a guessing game unlikely to yield success.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Corporate Information How You Benefit from Fisher Investments' Transparent Fee Structure

2026-08-04

2026-08-04 -

Corporate Information How Fisher Investments' High-Touch Service Helps You2026-08-04

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets — July 27 - July 312026-08-03

-

Expert Commentary 3 Things You Need to Know This Week | US Jobs, Trade Balance, Earnings Reports

2026-08-03

2026-08-03

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today