Personal Wealth Management / Retirement

Digging Deeper Into the 4% Rule’s Alleged Demise

Is a long-running rule of retirement investing about to go extinct?

Is the long-running 4% retirement rule about to go the way of the dodo bird? Some industry experts think so, pointing to stocks’ high valuations today as cause for lower market returns tomorrow, thus requiring retirees to update their spending plans. But we think this makes an awful lot out of one academic exercise—and falls prey to classic fallacies. We think planning retirement cash flows requires more nuance than simply using rules, but the general premise is well worth exploring.

The 4% rule holds that a diversified portfolio can support withdrawals of 4% of the starting value annually, adjusted for inflation, without premature depletion. Yet a recent Morningstar analysis purportedly called this into question. When running Monte Carlo simulations (which combine thousands of results across stocks and bonds to calculate the probability that a given asset allocation will support a given cash flow rate), they found that in a quarter of simulations, a half-stock, half-bond portfolio depleted within 30 years if withdrawals stayed at 4%. Most coverage attached some alarm bells to this, but we see a few caveats.

One, if a quarter of simulations ran out of money, that means three-fourths of them didn’t, rendering a roughly 75% probability of not outliving the assets. Two, a modest failure rate isn’t exactly a breaking development. You can see this for yourself in Fisher Investments Founder and Executive Chair Ken Fisher’s 2013 book, Plan Your Prosperity. In it, there are a handful of similar simulations modeling how different asset allocations could support various withdrawal rates over 30 years—at a time when stock valuations were theoretically more favorable than they are now. There was no 4% simulation, but there was one for 5%, and it showed a 78.2% probability of avoiding depletion within 30 years—and, on average, portfolios supported 28.8 years of withdrawals.[i] There are always risks and unknowns in investing, but we aren’t inclined to buy the this time is different argument we have seen since this report broke.

The Morningstar report also states, “Because of the confluence of low starting yields on bonds and equity valuations that are high relative to historical norms, retirees are unlikely to receive returns that match those in the past.”[ii] This advances the fallacy that high valuations imply stocks are “expensive” and may be nearing a peak, raising the risk of portfolio depletion due largely to the sequencing of returns. If you have cash flow needs, taking out money during a bear market means having less invested in stocks when a new bull market begins, potentially handicapping long-term returns. This is a common concern and one that has inspired some seemingly clever approaches—most of which ignore the time value of money—but we digress.

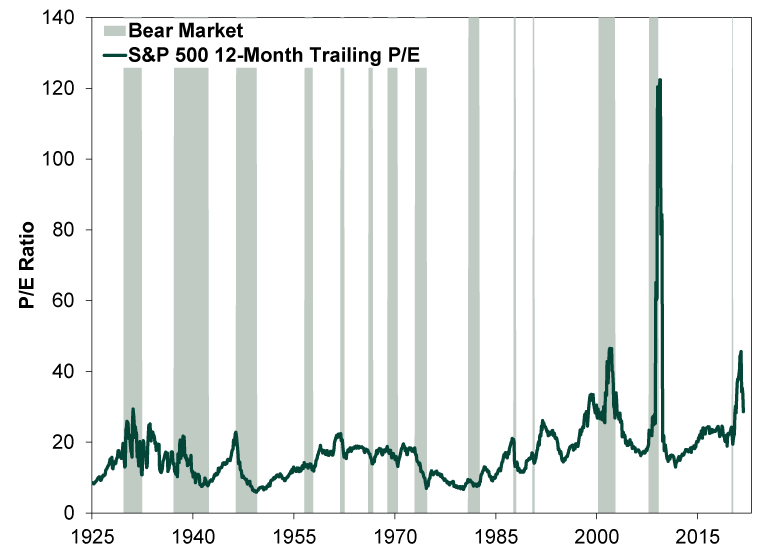

However, valuations aren’t market peak signals. They are backward-looking and reflect what just happened, not what is to come. Consider: Some widely watched valuation metrics (e.g., the trailing 12-month price-to-earnings [P/E] ratio) have actually come down in recent months, due largely to the denominator (earnings) growing faster than the numerator (price). Earnings skew can lead to extreme readings, but it isn’t telling about stocks’ direction. Go back 12 years, near the end of the 2007 – 2009 bear market. The financial crisis decimated earnings, which started showing up in the denominator in late 2008—and remained there for the next year or so. When a new bull market began in March 2009, rising prices sent the P/E skyrocketing. It was a math quirk, not an omen. (Exhibit 1)

Exhibit 1: Valuations Aren’t Leading Indicators

Source: Global Financial Data, Inc., as of 11/16/2021. S&P 500 12-Month Trailing P/E, monthly, January 1925 – October 2021.

There also isn’t much evidence weak long-term returns follow high valuations. October’s trailing P/E was 28.63, a level seen only in the late 1990s and early 1930s—not a huge data sample.[iii] But that 1931 breach happened when stocks were already well into the 1929 – 1932 bear market, again illustrating the denominator’s impact on the P/E calculation. Moreover, the S&P 500’s 30-year forward total return was 1543.7% cumulative, or 9.8% annualized—in line with the index’s long-term average annualized return of 10.2%.[iv] Obviously, we don’t have 30-year returns from 1998 yet, but thus far, the S&P 500’s cumulative return from 1998 to 2021 is 484.9% (8.0% annualized)—lower than average, but not alarmingly so, in our view.[v] Broadening the data sample, there are 290 months since good S&P 500 data begin in 1925 when the S&P 500’s trailing P/E exceeded 20. The median forward 30-year return is 1809.8% (10.3% annualized) while the median forward 20-year return is 356.5% (7.9% annualized).[vi] While past returns aren’t predictive, history suggests “expensive” stocks don’t automatically signal trouble looms for those seeking modest regular cash flows.

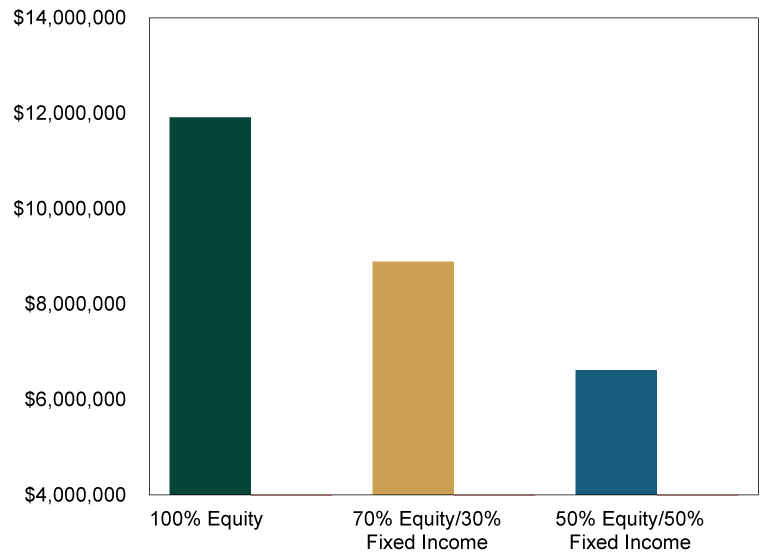

Which brings us to the second big hole: basing a projection on a 50/50 portfolio. Regardless of valuations, a 50/50 portfolio will generally have a lower expected long-term return than a 70/30 portfolio—or one 100% allocated to stocks. Exhibit 2 shows the cumulative growth of $1 million in three different asset allocations (50% stocks/50% bonds, 70% stocks/30% bonds and 100% stocks) from 1990 – 2020, a period that included the 1990s boom, two brutal bear markets and one of history’s best expansions in the 2010s. This projection also includes annual withdrawals of 4% of the starting portfolio value, adjusted annually for inflation.

Exhibit 2: Cumulative Growth of $1 Million With 4% Annual Withdrawals, 1990 – 2020

Source: Global Financial Data, Inc., as of 11/18/2021. Average annualized rate of return for S&P 500 Total Return Index and USA 10-Year Government Bond Index, based on monthly returns and rebalanced annually, 12/31/1990 – 12/31/2020. Annual inflation rate of 3.0% based on US CPI, January 1926 – December 2020.

In our view, a 50/50 portfolio isn’t right for everyone, as investors’ asset allocation depends on their specific investment goals, time horizon, cash flow needs, comfort with volatility and other personal factors. Bonds are less volatile in the short term but have lower long-term returns. Stocks are more volatile in the short run but have higher long-term returns that vary less from long-term averages than bonds’. There is a tradeoff between the two. More bonds means less expected short-term volatility, but it comes at the expense of limited return potential. In Plan Your Prosperity, that same 5% simulation showed a 50/50 portfolio had a 44.3% probability of having a balance greater than $1 million past 30 years—lower than the 54.5% for 70/30 and 58.7% for 100% equity.[vii]

A 50/50 portfolio might be most beneficial for those who require cash flow now to fund daily needs and have a shorter time horizon. For them, equity-like short-term volatility may be counterproductive. People with longer time horizons have more time to reap stocks’ long-term returns, and that growth can be key to supporting cash flow needs over time. Portfolio growth can help offset money you take out, buttressing your principal. It also can prepare you financially for the greater cash flow needs that can loom late in life, when medical expenses often soar.

What is right for you personally will depend on your circumstances. If you are age 65 today and have even just an average life expectancy—which is presently about 17 additional years for males and nearly 20 more years for females—along with modest cash flow needs in the neighborhood of 4%, then you will probably find that a 50% weighting in bonds is counterproductive for you.[viii] If a bear market strikes, you remain invested and your once-modest cash flow needs risk representing a larger share of your portfolio value, there are steps you can take on the fly to mitigate the impact. Reducing discretionary expenses is one. Keeping some projected distributions in cash, insulated from market volatility, is another. You can also prepare in advance by resisting the temptation to increase your withdrawals during big positive bull market years, as we think it is important to stay disciplined and keep future needs in mind.

There is no silver bullet for investors, and no one investing approach is foolproof. However, we think you can increase your probability of success by identifying the strategy with the highest likelihood of helping you reach your investing goals—and accepting the tradeoffs—while maintaining as much flexibility as your situation allows. Rather than marry general rules of thumb like the 4% rule, we think investors must dive deeper to figure out the plan that works best for them.

[i] Source: Plan Your Prosperity, Ken Fisher, pg. 112.

[ii] “The State of Retirement Income: Safe Withdrawal Rates,” Christine Benz, Jeff Ptak and John Rekenthaler, Morningstar, November 2021.

[iii] Source: Global Financial Data, Inc., as of 11/16/2021. S&P 500 Trailing 12-month P/E, October 2021.

[iv] Ibid. S&P 500 Total Return Index, February 1931 – February 1961 and January 1926 – December 2020.

[v] Ibid. S&P 500 Total Return Index, June 1998 – June 2021. P/E reached October 2021’s level in June 1998 (28.68).

[vi] Ibid.

[vii] See note i.

[viii] Source: The 2021 Annual Report of the Board of Trustees of the Federal Old-Age and Survivors Insurance and Federal Disability Insurance Trust Funds, accessed on 11/22/2021.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis The New Tariffs in Town Are Still Old News2026-07-24

-

Expert Commentary This Week in Review | Market Volatility, Tariffs, SpaceX

2026-07-24

2026-07-24 -

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23 -

Economics A Summertime Check-in on US Consumers2026-07-23

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today