Personal Wealth Management / Politics

How to Break the Brexit Blues

Dour sentiment toward the UK isn’t warranted, in our view.

Based on recent headlines, the UK might not seem ok. Brexit talks are plodding along, leaving business leaders antsy. Conservative Prime Minister Theresa May is facing a rebellion from her own ministers. Projections are bleak on the economic front. Sounds bad! However, in our view, many investors fail to appreciate the UK economy’s strength—a sign of sentiment’s disconnect from reality—which sets up bullish upside surprise.

Brexit and its alleged negative consequences continue influencing just about every major economic and political UK narrative. Talks between UK and EU negotiators seem constantly stalled, frustrating both pols and businesses alike. Domestically, controversy has embroiled UK politics. Two ministers resigned from May’s government recently, prompting speculation that the prime minister has lost control—and rumblings of a leadership challenge have started. 20 Tory MPs have also threatened to revolt against a bill enshrining March 29, 2019 in UK law as the official EU exit date.

Beyond these developments, policymakers and experts bemoan the state of the UK economy. BoE Governor and metaphorical “unreliable boyfriend” Mark Carney said the economy would be “booming” if it wasn’t for Brexit. Analysts worry inflation’s 3.0% y/y rise in October—a repeat of September’s rate, which was the highest in five years—could choke consumer spending, especially since wages rose only 2.2% y/y in the same month (implying they fell in real terms). UK retail sales rose 0.3% m/m in October, beating expectations, but headlines dwelled on the first year-over-year contraction in four years.[i] UK industries have also expressed concern future trade deals could hurt them significantly in the long term. The underlying theme: Things are bad now, and they will only get worse when the UK actually exits.

While it is impossible to know what the post-Brexit future will look like, recent data show current concerns about the economy may be a wee bit overwrought. Q3 GDP rose 0.4% q/q (1.6% annualized), picking up from Q2’s 0.3% rate. The services sector continues expanding across the board. More recent numbers counter the notion the economy is flagging, too. Continuing on the services front, IHS Markit/CIPS’ UK October Services PMI picked up to 55.6 from September’s 53.6, the strongest reading in six months (PMI readings above 50 indicate a majority of surveyed firms expanded). New order growth rebounded from September’s 13-month low, a positive sign looking ahead. Also, input cost inflation eased to its lowest since September 2016—a benefit for service providers in the form of lower operating costs. This could suggest broader inflation pressures are easing, but CPI has yet to register it.

Not to be outdone, the manufacturing PMI also sped up from September’s 56.0 to 56.3, and IHS Markit noted this expansion was, “broad-based by sub-sector, with consumer, intermediate and investment goods producers all registering output growth.” Like services, manufacturing new orders bounced back in October. Elsewhere in industry, September industrial production rose 0.7% m/m (2.5% y/y), the strongest monthly rate in 2017 and easily exceeding estimates. The manufacturing subsector accelerated to 0.7% m/m from August’s 0.4%—the fifth straight positive month after starting the year with four consecutive declines. While the industrial sector is a small slice of the total economy compared to services, growth here reveals how broad-based the expansion is. For all the talk about manufacturing making up for services’ weakness, the fact remains the service sector, which accounts for about 80% of UK output, is still growing.

Despite these positive economic realities, negative attitudes persist. The European Commission downgraded its 2017 UK economic growth forecast to 1.5% (originally 1.8% in May), citing inflation constraints on consumption and uncertainty hurting business investment. Plus, stocks seem to be reflecting this dour mood. The MSCI UK is up just 6.7% year-to-date in GBP, trailing the MSCI World’s 10.2%.[ii] If UK equity markets are lagging, this means stocks—the ultimate leading indicator—are showing reality isn’t great, right? Not necessarily. While stocks are a better forward-looking indicator than most and very efficient in the long run, they can be irrational in the short term, when sentiment—driven by political uncertainty or myriad other factors—can weigh on returns.

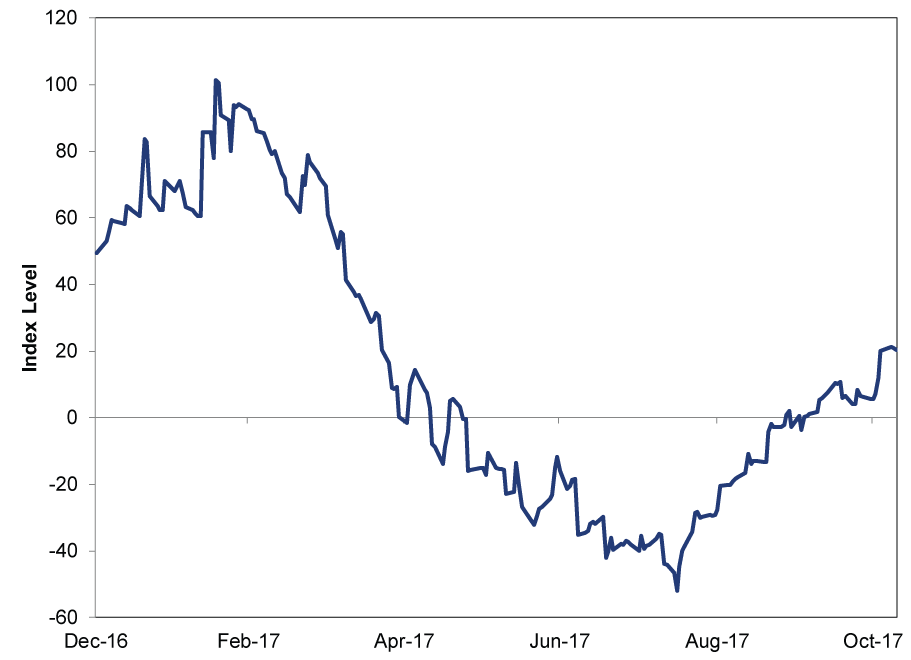

We don’t believe economic reality warrants the prevalent negative sentiment, and in our view, this disconnect creates room for upside. Consider the Citigroup UK Economic Surprise Index, which is a loose measure of how economic data relate to professional forecasters’ expectations. When the line is above zero, the economic data overall exceed economists’ consensus estimates (and vice versa when the line is below zero). After a spell of disappointment earlier this year, recent UK data have improved versus expectations—and are now mostly beating them.

Exhibit 1: Citi Surprise Gauge for the UK

Source: FactSet, as of 11/10/2017. Citi Surprise Index (daily), from 12/30/2016 – 11/9/2017.

While the political circus surrounding May and speculation about her future grabs the most eyeballs, UK politics remains largely gridlocked—an underappreciated positive. May is leading a do-little minority government that is struggling to deal with Brexit talks. This likely forestalls any big legislative changes—a positive that reduces the uncertainty stocks dislike.

[i] RULE: Never presume a year-over-year change more perfectly tells the tale of an economic data point than monthly changes, when available. The former is too subject to base effects and data from many months ago. While the latter is subject to choppiness, it is at least at now now. Said differently, you can’t debunk a monthly change by citing the year-over-year.

[ii] Source: FactSet, as of 11/13/2017. MSCI UK and MSCI World Total Return Indexes, net dividends, in GBP, from 12/30/2016 – 11/15/2017.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Why “War Winner” Trades Are Off Base2026-03-20

-

Expert Commentary This Week in Review | Energy Markets, Fed Meeting, Earnings Reporting

2026-03-20

2026-03-20 -

Market Analysis Around the World in Central Banking, Iran War Edition2026-03-19

-

Politics Beyond the War: A Political Roundup Covering America, Canada and Denmark2026-03-17

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today