Personal Wealth Management / Economics

Inflation’s Fix: Patience, Not Policy

The Fed still can’t do anything to fix the supply shortages driving inflation.

Friday, the US Bureau of Labor Statistics (BLS) unveiled November’s Consumer Price Index (CPI) report, which has been a key focus for investors and analysts all year, given lofty readings. The report didn’t disappoint all the antsy analysts, with the CPI rising 6.8% y/y, the fastest rate since June 1982.[i] It all compounds inflation fears, which have many pushing the Fed to respond with a faster wind-down of quantitative easing bond purchases and rate hikes. But in our view, the likelier fix for quick-rising prices of late is simply patience, not monetary policy—much of the influence on prices is outside the Fed’s control.

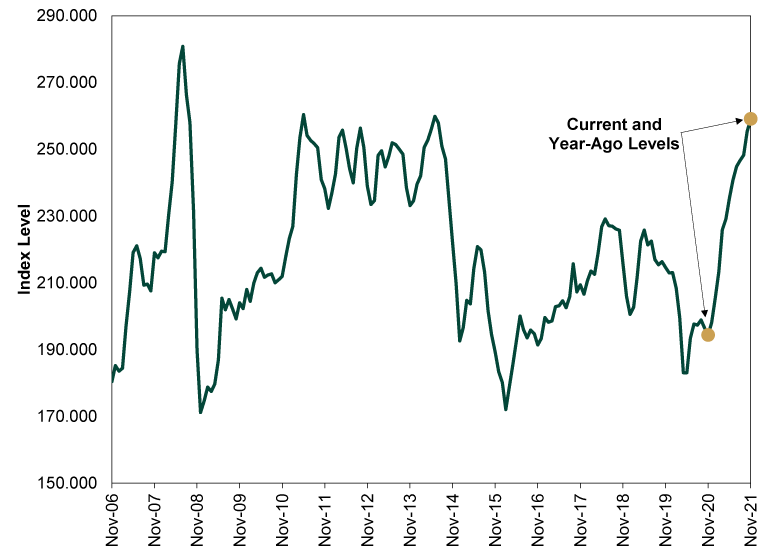

That 6.8% y/y rate got most of the media attention this morning, but it isn’t all that meaningful. As we have noted many times on these pages, calculation quirks in year-over-year mathematics are inflating the headline figure. Consider energy prices. As Exhibit 1 shows, November 2021’s CPI Energy component notched an index level of 259.1. This has risen steadily over the past year as oil prices ticked up. But in November 2020, the index level was 194.4—down markedly from the January 2020 pre-pandemic mark of 213.0.

Exhibit 1: CPI Energy Index’s Lingering Base Effect

Source: FactSet, as of 12/10/2021. US CPI Energy index level, November 2006 – November 2021. Figures are not seasonally adjusted.

BLS data show energy’s 33.3% y/y rise added 2.01 percentage points to the headline CPI rate—the biggest contribution since September 2005 (in the wake of Hurricane Katrina) and an unusually big addition given energy comprises 7.5% of the CPI’s basket of goods and services.[ii]

But even if you look at core CPI, which strips out food and energy, lingering pandemic effects still skew the 4.9% year-over-year rate. New and used cars, hit hard by the well-publicized semiconductor shortages, are up 11.1% and 31.4% respectively over the past year—adding 1.3 percentage points to the headline rate.[iii]

None of this is to totally dismiss the impacts of inflation lately, but we think it is far more proper to set aside the headline-grabbing year-over-year rate that so many point to as notching records. Instead, look to month-over-month figures. In November, CPI rose 0.8% m/m, down slightly from October’s 0.9%.[iv] (Excluding food and energy, prices rose 0.5% m/m, down from 0.6%.) These are still relatively quick rates by historical standards, and the headline rate has accelerated sharply since slowing to 0.3% m/m in August, which matched the historical average. But that acceleration stemmed primarily from energy’s autumn surge. Moreover, November’s headline and core month-over-month rates are a slight deceleration and aren’t at the 39-year highs the more skewed yearly gauges are. Furthermore, they still show influence from the pandemic’s effects: Energy and transportation goods (think: cars) were the first and third biggest contributors to the headline rate of change, areas showing great influence from the lockdown and reopening trends (and energy prices are down of late, which may lower future readings, if this trend holds). They added 0.26 and 0.14 percentage point to the monthly headline CPI change. That is about half the month’s overall rise—in two categories that total about 15% of the overall CPI basket.[v] That trend—outsized increases in narrow categories—underpins much of the recent spate of high headline inflation readings.

Second was shelter costs, including rent and the government’s attempt to estimate changes in home ownership costs (owners’ equivalent rent), which no one actually pays. While rents likely are climbing for some, very few people see price changes in rents on a monthly basis. Homeowners see even less impact, considering the vast number of homes owned outright or via fixed mortgages.

Regardless, the fast-rising metrics have many clamoring for the Fed to dial back QE faster or hike rates sooner. Now, we have long argued QE isn’t inflation fuel to begin with. But even if you disagree, ask yourself: If the Fed slows bond purchases and/or hikes rates, will that somehow boost semiconductor production, easing the pressure on car prices? Will it boost wind power production in Europe, easing demand on natural gas and oil as substitutes? We think the answers are no and no, illustrating how the present issues are on the supply side, not tied to hotly inflationary Fed policy. While we have no reason to think dialing back QE or hiking rates threaten the bull market, we also think they are unlikely to quell CPI’s climb.

No, accomplishing that will take something more complex: Market forces. High and rising prices in certain categories encourage more production, which should ultimately cool inflation. We are already seeing this in energy production and semiconductor investment. It may take a little time, but, in our view, patience while market forces work is the path to slowing inflation—not Fed policy shifts.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis The New Tariffs in Town Are Still Old News2026-07-24

-

Expert Commentary This Week in Review | Market Volatility, Tariffs, SpaceX

2026-07-24

2026-07-24 -

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23 -

Economics A Summertime Check-in on US Consumers2026-07-23

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today