Personal Wealth Management / Economics

Into Perspective: Renewed Fears of an EM Currency and Debt Crisis

Most Emerging Markets are in much better shape than headlines suggest.

The global bear market beginning in February left few asset classes unscathed. But the heightened risk aversion hit many Emerging Markets (EMs) particularly hard, with a surge in capital outflows and material currency weakness reigniting debt fears. This is a common narrative during times of stress—EMs have been plagued by multiple crises over the past 30 years, and memories of the late-1990s currency crisis loom large. But too often, pundits focus on fragile positions in a few countries, then extrapolate those fears to the broader category. A similar phenomenon is occurring today, with headlines dwelling on IMF bailouts and defaults. Yet most EMs are in relatively healthy shape, and the probability of a new currency and debt crisis remains low.

Fears surrounding debt tend to focus on absolute levels—think of the US national debt clock, currently over $25 trillion at the time of this writing. EMs as a whole owe even more—a massive $71 trillion.[i] Big numbers scare people, and there isn’t a person on Earth who thinks trillions of anything is a small figure. Overall debt levels have indeed risen globally in the past decade—but so has the size of the global economy and countries’ institutional defenses against financial trouble. In our opinion, it is more instructive for investors to focus on debt sustainability, which means scaling borrowings and better understanding their composition.

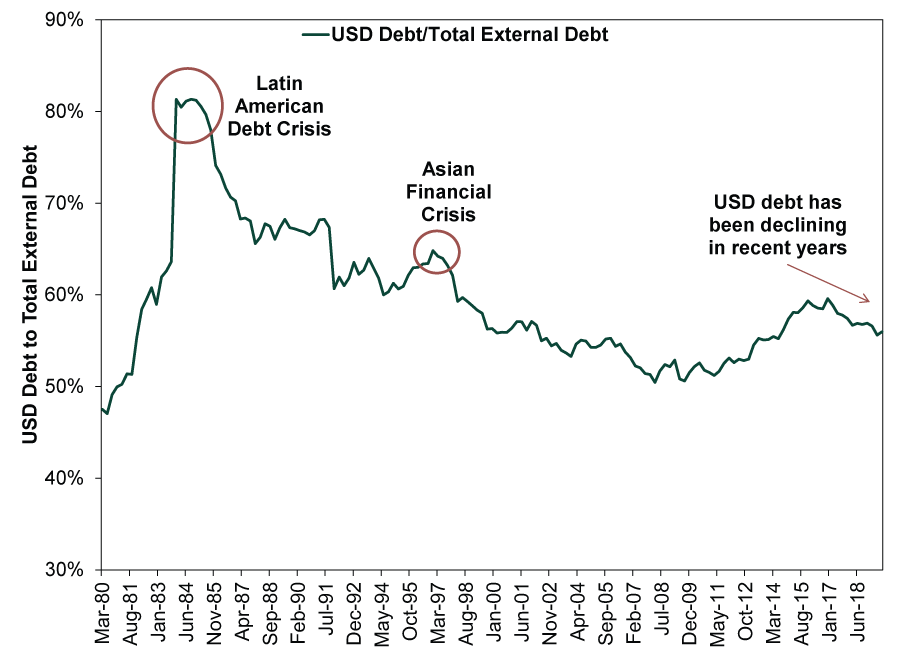

Historically, EM debt crises generally arise from currency crises. This is because EMs find it more difficult to raise funds domestically, so they lean heavily on financing abroad in foreign currency. The Asian Financial Crisis in 1997 – 1998—the last true debt crisis to ripple through EM—is a textbook case of what can go wrong. At that time, many countries pegged their currency to the US dollar to piggy back on its relative stability. They then heavily borrowed in dollar-denominated debt to finance booming economic growth, keeping few currency reserves to fend off speculators. When their currencies fell under pressure, they quickly ran out of firepower to defend the pegs and were forced to devalue. In doing so, their debt levels and service costs in local currency terms skyrocketed—and crisis ensued.

Much has changed today. As confidence in EM institutions (e.g., central banks and national treasuries) has grown over the past few decades, countries have been able to raise more debt in local currency, and their overall reliance on US dollar funding has declined. More importantly, the level of US dollar-denominated EM debt has been declining in recent years and remains well below levels of prior crises. Hence, currency volatility has less impact on overall debt burdens than in the past.

Exhibit 1: EM Aggregate US Dollar Debt

Source: Bank for International Settlements, FactSet and Fisher Investments Research, as of 4/30/2020. Aggregate ratio of US debt to total external debt for Brazil, Chile, China, Colombia, Czech Republic, Hungary, India, Indonesia, Korea, Malaysia, Mexico, Peru, Philippines, Poland, Russia, South Africa, Thailand, Turkey and Taiwan, 1980 – 2019.

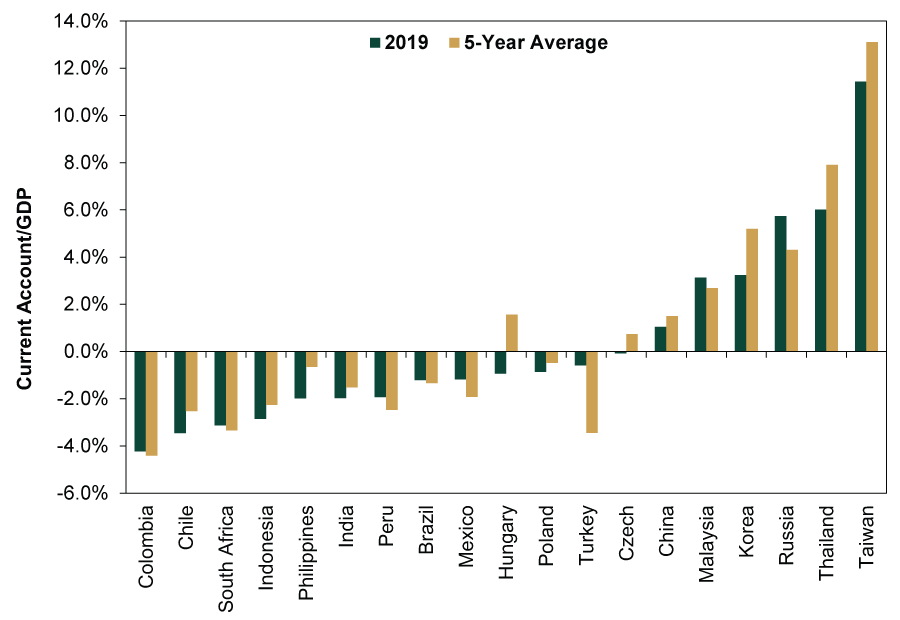

But EMs still need foreign capital, which often puts their current account deficits under the microscope. Balance of payments accounting records all transactions made between countries, and the current account and the capital account are the two major components. The current account is dominated by the trade balance (exports minus imports), while the capital account measures financial flows like investments. These two components must net to zero. That is, a current account deficit is exactly offset by a capital account surplus. This is why you hear concerns that foreign entities are “funding” the US given its large current account deficit—capital must come in from abroad to net out the current account. But many of the largest EM countries run either current account surpluses or small deficits. Only a few countries have meaningfully large deficits. Moreover, this metric hasn’t materially worsened in the past several years, and in many cases, it has improved.

Exhibit 2: EM Current Account Deficits

Source: IMF and FactSet, as of 4/30/2020. Current account deficit as a percentage of GDP for the countries shown, 2015 – 2019.

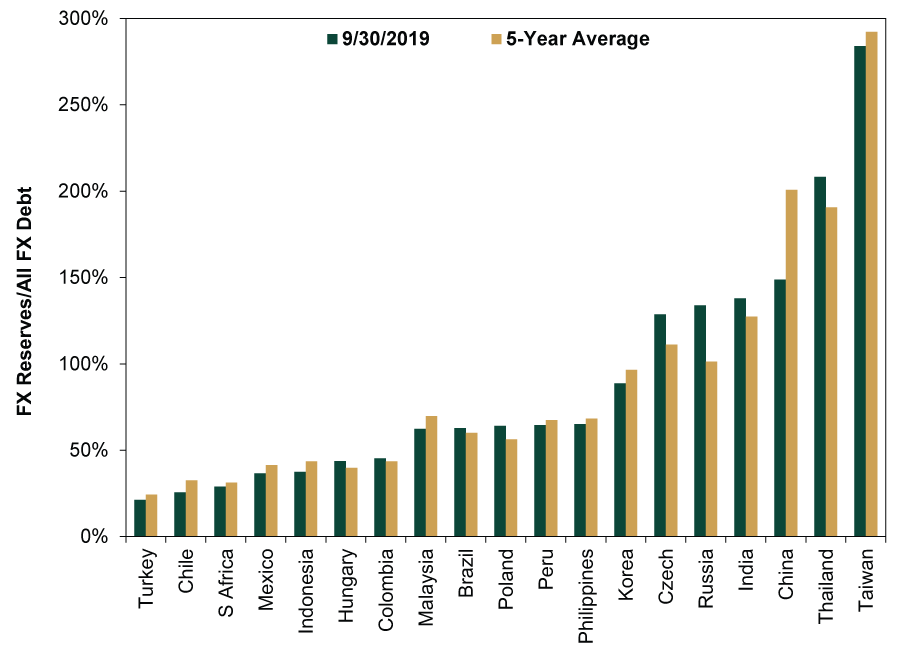

Institutional defenses also play a critical role in scaling a country’s ability to fend off crisis. This is typically measured with foreign currency reserves, which central banks can use to defend outflows and combat currency depreciation. Imagine an investor sells an Indonesian stock and buys a US Treasury bond. They are also selling Indonesian rupiahs and buying US dollars, putting downward pressure on the former and upward on the latter. The Indonesian central bank can use its reserves to buy its local currency, offsetting the depreciation. Scaling this metric by total external debt, some countries look vulnerable, such as Turkey and South Africa. But their problems are widely known and stem from unique domestic factors. Most EMs have substantial levels of reserves relative to debt burdens.

Exhibit 3: EM Forex Reserves to Debt

Source: Bank for International Settlements, IMF, FactSet and Fisher Investments Research, as of 4/30/2020. Foreign exchange reserves as a percentage of all foreign currency debt for the countries shown, 2015 – 2019.

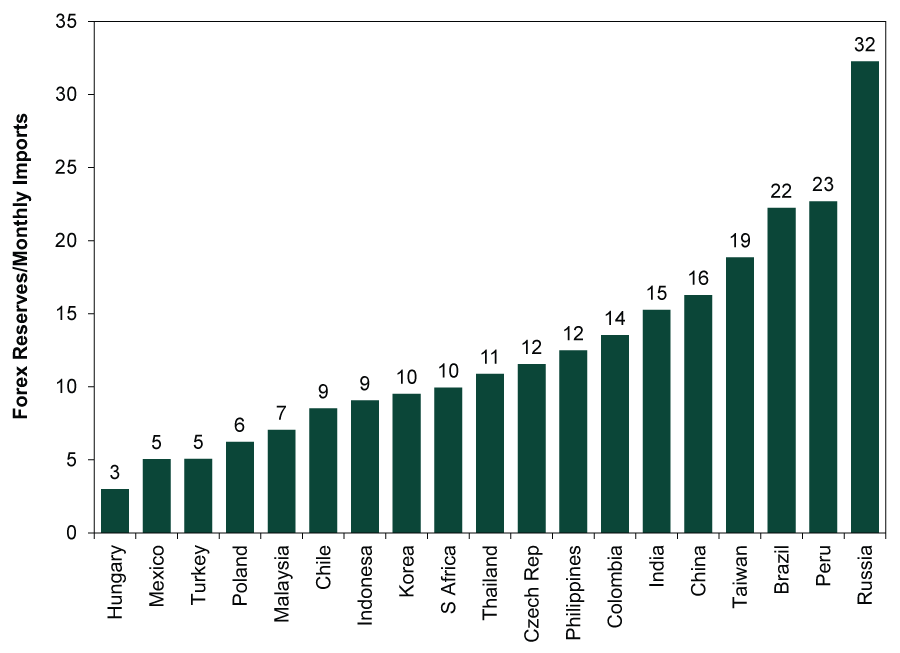

Another common vulnerability metric measures the level of reserves to imports. The idea here: If all flows cease because of capital markets volatility, how long can a country sustain its current consumption of imports? Historically, a rule of thumb has been that countries need at least three months of import cover. But even if a stricter threshold is applied, most EMs have adequate reserves.

Exhibit 4: EM Forex Reserves to Imports

Source: FactSet, as of 4/30/2020. Foreign exchange reserves as multiple of monthly imports for the countries shown. Data are the latest available for each country—either February 2020 or March 2020, except for China, which is current as of December 2019.

The final important consideration is the maturity composition of outstanding debt. Short-term shocks raise concerns about countries’ ability to refinance maturing bonds. One proxy for stability is the level of reserves relative to debt due in the next one to two years. Argentina is a clear outlier, with sovereign and corporate borrowings due through 2022 constituting more than 150% of reserves—a clear reason the country is on the brink of its ninth sovereign default.[ii] But vulnerability drops off significantly from there. Only Turkey and South Africa have bonds due through 2022 worth more than 50% reserves.[iii]

Using these metrics, several countries appear more vulnerable than others. This includes usual suspects like Argentina, Turkey and South Africa, which have long histories of external debt fragility as well as deep-seated, widely known present-day issues. These countries may face continued headwinds. But they represent a relatively small portion of EMs and stand in contrast to the rest of the category, whose debt burdens appear relatively sustainable.

[i] “Why the Coming Emerging Markets Debt Crisis Will Be Messy,” Colby Smith and Robin Wigglesworth, Financial Times, May 12, 2020.

[ii] Source: UBS, as of 4/30/2020.

[iii] Ibid.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Volatility By the Numbers: 2026’s ‘Volatility’2026-06-12

-

Expert Commentary This Week in Review | IPOs, US Inflation, ECB Rate Hike

2026-06-12

2026-06-12 -

Market Analysis Are World Oil Reserves Dangerously Low?2026-06-11

-

Expert Commentary Think Twice Before Buying an IPO

2026-06-11

2026-06-11

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today