Personal Wealth Management / Economics

Jobs and the Pessimism of Disbelief

What to glean from the “good jobs news is bad for stocks” mentality.

Coming into Friday’s US employment situation report, fear abounded. But, perhaps counterintuitively, the fear wasn’t that the data would support widespread recession narratives. No, most onlookers feared the opposite: that data would show a big payroll gain, suggesting labor markets remain tight—in turn, fostering more Fed hikes. There are myriad presumptions that underlie this good-data-are-bad-news theory, but above all, we think the inconsolable mood illustrates the “Pessimism of Disbelief” (PoD) in action—a sign sentiment is too low relative to reality.

Ahead of the release, we saw many headlines say signs of strong economic growth entail further Fed tightening. Those Fed hikes, proponents argue, will surely pummel stocks even more. As the thinking goes, ongoing labor shortages and supply constraints mean any growth in payrolls is inflationary. To fight inflation, the Fed has to crush job growth and induce recession if need be to bring prices to heel. Under these conditions, pundits argue the outlook for earnings isn’t great. Hence, good news is really bad news.

That was the general zeitgeist entering the release. Never mind that the link between jobs and inflation is tenuous at best. Never mind that rate hikes aren’t automatically bearish and that markets are very well aware the Fed is trying to tighten policy, limiting surprise power. Never mind that the Fed isn’t as powerful as many think.

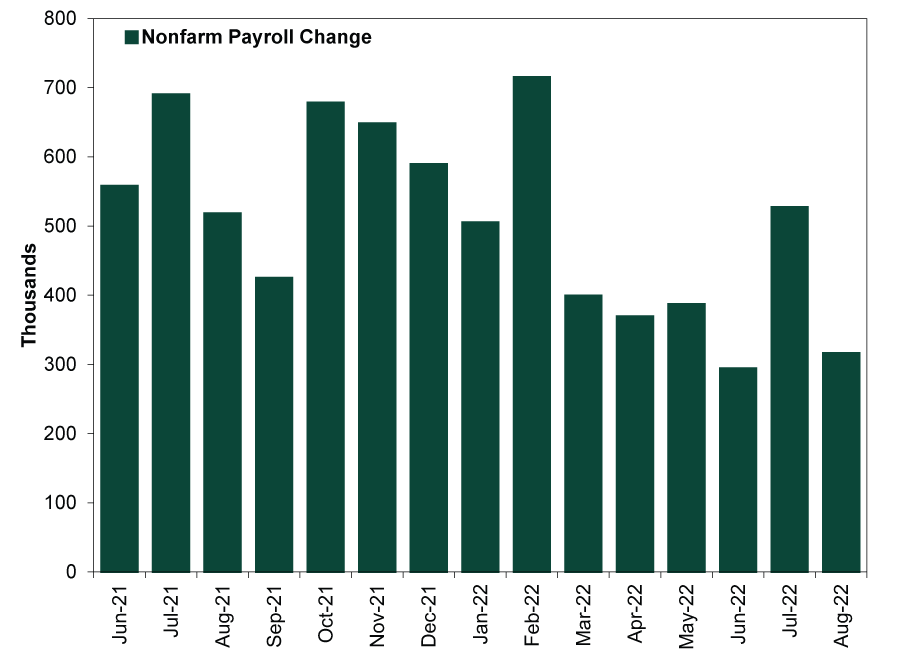

Regardless, Friday’s data should have eased those fears, as the unemployment rate rose (for positive reasons) while hiring cooled. August nonfarm payroll gains of 315,000 slightly beat expectations for 300,000 (although the BLS revised the previous two months down by 107,000, so eye-of-the-beholder and all that). And, as Exhibit 1 shows, overall job growth has decelerated irregularly lately. The three-month average has noticeably slowed toward 300,000 from around 600,000 at the year’s start.

Exhibit 1: Employment Growth Has Generally Slowed From Last Year

Source: Federal Reserve Bank of St. Louis, as of 9/2/2022. Nonfarm payrolls, June 2021 – August 2022.

Meanwhile, the unemployment rate edged up to 3.7% from 3.5%, as labor force participation rose by a whopping 786,000—an increase not generally seen outside economic recovery from recession. More people are being drawn into the pool of available workers, but prospective employers aren’t immediately hiring them. A greater labor supply, one would think, should assuage pundits’ tight labor market concerns somewhat, considering it suggests the labor market has more slack than feared.

Yet pundits’ takes turned immediately to how the Fed would react. Most of the chatter surrounded the likelihood of another “jumbo” rate hike September 21 supposedly to quell inflation, “regardless of the potential economic fallout.”[i] Will it be a third-straight three-quarter point hike or just a half-point one? Presuming to know the collective mind of the Fed, they surmise “... policymakers at the Federal Reserve believe that the job market is effectively overheated: With twice as many open jobs as job seekers, employers are competing for workers by pushing up wages and, ultimately, prices. The Fed is hoping that by raising interest rates, it can cool off the job market enough to bring down inflation, but not by so much that unemployment skyrockets.”[ii] Still others cast the data negatively, arguing August’s tiny uptick in unemployment is evidence Fed hikes have already pushed the economy into recession—with the outlook for stocks bleak—as headlines warn: “The summer rally is over.”[iii]

We think all the Fed fear smacks of the Pessimism of Disbelief, a regular phenomenon we see near bear market troughs. Rather than take objectively good news as good, PoD either dismisses it or argues it is fleeting and sure to morph into even worse negatives. But a focus on false negatives—like solid, but late-lagging employment data with little implication for forward-looking stocks—shows how low expectations are now. Such downtrodden sentiment means relief and positive surprise—the forces that power early bull markets—is easier to attain. To us, it is one example showing the foundation of a market recovery is in place.

[i] “Solid August Jobs Report Leaves Another Jumbo Fed Rate Hike on the Table in September,” Megan Henney, FOXBusiness, 9/3/2022.

[ii] “U.S. Job Growth Slows From Red-Hot Pace,” Ben Casselman, The New York Times, 9/2/2022.

[iii] “Recession Watch: Stock Market Rally ‘Is Over’ as Unemployment Starts Rising and Fears Intensify,” Jonathan Ponciano, Forbes, 9/3/2022.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis The New Tariffs in Town Are Still Old News2026-07-24

-

Expert Commentary This Week in Review | Market Volatility, Tariffs, SpaceX

2026-07-24

2026-07-24 -

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23 -

Economics A Summertime Check-in on US Consumers2026-07-23

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today