Personal Wealth Management / Market Analysis

Money Supply Trends Remain Disinflationary

Actual leading inflation indicators help put March’s uptick—and rate cut chatter—in context.

The world continued digesting March’s US Consumer Price Index report Thursday, with the American inflation uptick oddly featuring in … European Central Bank (ECB) interest rate discourse. Amid talk of stickier US inflation causing the Fed to hold off on rate cuts for a while longer, ECB head Christine Lagarde pushed back on the notion that this would have anything to do with her institution’s decision making. “We are data-dependent. We are not Fed-dependent,” she said, leaving headlines to keep June circled in the calendar.[i] With all this talk about rate timing and inflation wiggles, we think it is worth a quick look at some actual leading inflation indicators to see how short-sighted this debate really is and why stocks should soon look past it.

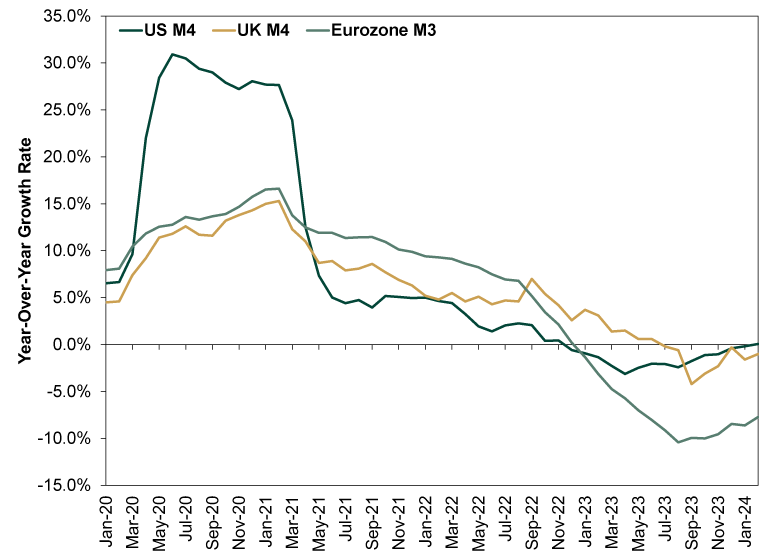

Those indicators: broad money supply growth in the US, UK and eurozone. Exhibit 1 shows the broadest measure in each since the beginning of 2020. You will of course see big spikes during lockdowns, when central bankers pumped new money to boost demand while businesses were shut and consumers housebound. These spikes played a big role in 2022’s inflation, as they meant a boatload of new cash was sloshing around major economies at a time production was limited. Too much money chasing too few goods and services is a classic recipe for inflation. But that was then. Now? Western economies have worked a lot of this excess out—partly through output growth and partly through monetary contractions.

Exhibit 1: A Broad Monetary Contraction

Source: Center for Financial Stability, Bank of England and ECB, as of 4/11/2024.

US money supply contracted for over a year before turning just barely flat in February. But that is the broadest measure, which includes US Treasury bonds. The Center for Financial Stability also publishes an alternate measure of M4 that excludes Treasurys, and it is still falling. Given this stuff tends to hit the real economy at a lag, we think it is fair to say economic conditions here are still disinflationary. The UK is in a similar boat, with money supply’s latest drops shallow. But the eurozone is another matter. Its decline is steeper and deeper. None of this predicts what the ECB will do, but we think it illuminates why officials there don’t think Fed policy should factor. A central bank’s job is to set policy for its home country or region, in the ECB’s case. The Fed will do what it thinks makes most sense based on conditions here, and the ECB does the same for the eurozone. Conditions are different on each side of the Atlantic, so the ECB’s calculus is different.

Note, we aren’t saying monetary contractions render rate cuts necessary. Falling money supply would ordinarily be a warning sign for the economy, but in the wake of 2020’s spikes, this downturn just evens out the prior excess and brings the level of money supply closer to its long-term trends. In our view, it is disinflationary and probably not the seeds of a deep recession, provided it doesn’t turn down again and get much deeper. That doesn’t look likely, but we aren’t blind to the probability.

More importantly in the here and now, the rate cut conversation surrounds what central banks will do in the next couple of months. Stocks don’t look that short-term. Markets look most to the next 3 – 30 months and how reality is likely to square with expectations over that entire span. To us, it seems quite unlikely that when any central bank makes its first cut will mean much to corporate earnings in this longer window, which is what stocks primarily care about. The rate cut timing debate may be a big deal for headlines, but for stocks, regardless of fleeting sentiment impacts, it should be a sideshow.

[i] “ECB Signals It’s Moving Closer to a Cut but Keeps Rates Steady,” Tom Fairless, The Wall Street Journal, 4/11/2024.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Quick Hit: The July Jobs Nothingburger2026-08-07

-

Expert Commentary This Week in Review | Record Highs, US Jobs, Yen Intervention

2026-08-07

2026-08-07 -

Market Analysis Western Oil and Gas Producers Are Ramping Up2026-08-06

-

Politics The Tenth Question Facing Alberta2026-08-06

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today