Personal Wealth Management / Market Analysis

Needed Context for China’s ‘Disappointing’ Data

The latest Purchasing Managers’ Indexes match the long-term trend.

Is China’s economic recovery going into reverse? After April’s monthly indicators showed slower-than-expected growth, May’s official Purchasing Managers’ Indexes (PMIs) inspired more gloom as manufacturing’s contraction deepened from 49.2 to 48.8 and services slowed from 55.1 to 53.8 (readings over 50 indicate expansion).[i] So much for a post-pandemic reopening bounce, headlines moan. Thing is, best we can tell, China is following a pretty normal reopening course: returning to long-term trends after an initial, short-lived boom, with the boom getting smaller in each cycle of lockdown to reopening. Perhaps some folks’ expectations were too high entering this spring, as we wrote, but with pessimism quickly returning now, a slow-growing China should be fine for stocks.

Most of Wednesday’s PMI commentary lacked meaningful long-term context. The articles we read looked back, but only to 2020, comparing now to the rebound from the first wave of lockdowns. Then, manufacturing stayed positive for over a year before slipping back into contraction as the autumn 2021 COVID wave prompted fresh restrictions. When the rebound from that and successive waves fizzled, headlines logically blamed the COVID recurrences in Shanghai and other major metro areas—setting expectations for a lasting boom now that China has abandoned Zero-COVID.

That expectation has long seemed a bit off base to us, as it differs from the developed world’s experience. In the US, UK and eurozone, the first reopening brought the biggest boom simply because it followed the most draconian lockdown—and when society hadn’t learned how to live with restrictions and keep them from hampering commerce as severely. That is key context. When restrictions returned later in 2020 and 2021, activity didn’t fall as much as in February and March 2020, so there wasn’t as much ground to regain when things reopened. Accordingly, the subsequent rebounds were smaller and shorter, with longer-term trends reasserting themselves swiftly.

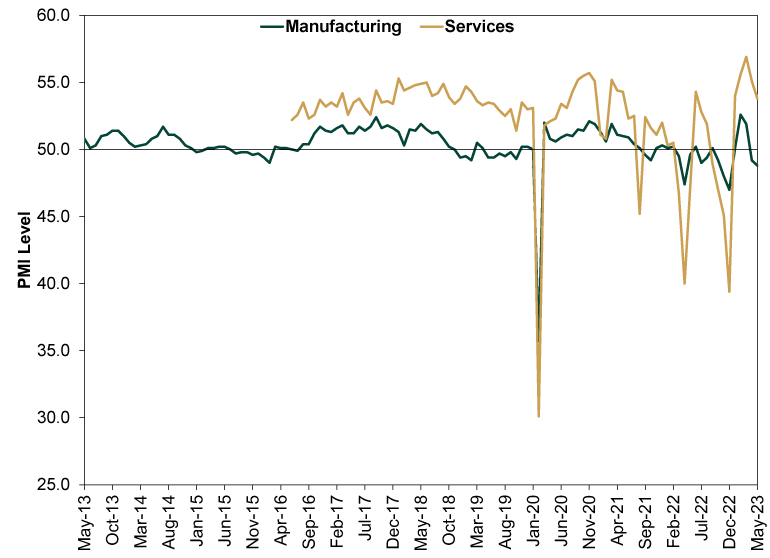

We think this is what China is now experiencing. Exhibit 1 shows this with the official Manufacturing and Services PMIs. These indicators emphasize larger companies, so they aren’t a complete indicator of how all Chinese businesses are doing. Caixin’s PMIs include smaller and private businesses, but they aren’t out until later this week. Regardless, the official PMIs are a solid look at the long-term trends. Manufacturing, you will see, has been in and out of contraction for the past decade, with long stretches below 50. Services growth has been much steadier since those data start in mid-2016, but it has rarely topped 55, and May’s reading is in line with the pre-COVID average of 53.6.[ii]

Exhibit 1: Putting China’s PMIs in Context

Source: FactSet, as of 5/31/2023. Official Manufacturing PMI, May 2013 – May 2023, and official Services PMI, June 2016 – May 2023. Note: The Non-Manufacturing PMI, which includes Services, has a longer history but is sometimes skewed by mining and oil drilling, so we use Services here for a more focused look.

So we don’t buy the criticism that China’s economy is lapsing into an unprecedented funk with high local government debt and weak demographics weighing on output. Those are convenient scapegoats, but they ignore the longer history. In proper context, it looks more like China is returning to its longer-term trend where heavy industry continues giving way to services and consumption. This is right in line with both the normal course of economic development and the government’s ambitions. Officials have long seen export-driven manufacturing as an unreliable economic engine, too subject to the rest of the world’s ups and downs to generate long-term prosperity and the economic mobility necessary to ensure continued one-party rule. Services-led growth that harnesses domestic demand has long been the solution, and services has grown and thrived alongside struggling manufacturing for many years now.

That combination has been just fine for the global economy. Low-cost manufacturing has shifted more to Vietnam, Mexico and other nations. Meanwhile, rising Chinese consumption has boosted demand for companies the world over. The world’s second-largest economy has added nicely to global GDP, helping support developed-world stocks. If China’s modest services growth and contracting manufacturing didn’t derail global markets in the 2010s, we don’t see a logical case for their being suddenly bearish now. Rather, we see the disappointment over May’s PMIs as a helpful sentiment reset that should make expectations easier to top.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary 3 Things You Need to Know This Week | US Inflation, UK GDP, RBA

2026-08-10

2026-08-10 -

Market Analysis Four Overlooked Costs With Dividends2026-08-10

-

Market Analysis Rechewing Fed Independence Fears2026-08-10

-

Market Analysis Quick Hit: The July Jobs Nothingburger2026-08-07

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today