Personal Wealth Management / Market Analysis

Q2 Earnings in Focus

They mostly just confirm what sector returns already reflect.

Q2 earnings season is winding down, with the vast majority of S&P 500 companies having reported. The results? Three-fourths of those reporting so far beat expectations, and revenues did much of the heavy lifting. Yet while Energy earnings soared, profits in the other 10 sectors overall fell, echoing the split among sector returns during the bear market. We think this is a good reminder that stocks look forward.

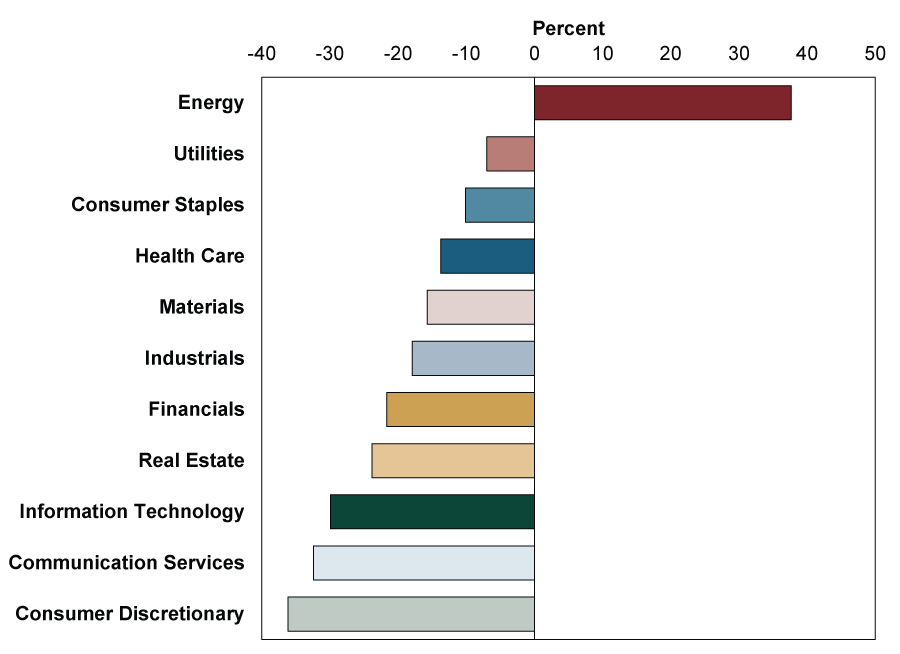

As Exhibit 1 shows, sector returns from their early peak this year through the year’s low point to date on June 16 mostly previewed how earnings turned out. While S&P 500 earnings overall rose 6.7% y/y, much of that came from Energy earnings soaring 299.2%. Excluding Energy, they fell -3.7%.[i] So while headline earnings growth was near its 7.1% annualized average historically, it masks some underlying weakness.[ii] Yet first-half sector returns largely captured the earnings dynamic below the surface, with only Energy positive through Q2. Markets anticipated high oil prices’ impact on Energy earnings well in advance of official reports.

Exhibit 1: S&P 500 Sector Returns, 1/3/2022 – 6/16/2022

Source: FactSet, as of 8/11/2022. S&P 500 sector total returns, 1/3/2022 – 6/16/2022.

Note that we aren’t arguing the bear market fell on earnings weakness outside Energy—in our view, sentiment, not fundamental problems, was the bear market’s primary contributing factor. Moreover, while investors’ anticipation of high oil prices driving big earnings growth probably drove Energy’s singular outperformance, it isn’t as if non-Energy sectors’ earnings fell and surprised negatively across the board. Excluding Energy, five sectors’ earnings rose (Industrials, Materials, Real Estate, Health Care, Tech), and five fell (Financials, Consumer Discretionary, Communication Services, Utilities and Consumer Staples). Of the former, Industrials, Health Care and Tech earnings are coming out ahead of consensus expectations at Q2’s end. Meanwhile, Financials, Consumer Discretionary and Communication Services earnings have been materially worse than expectations indicated.

But there are some nuances here as well. For example, Financials companies’ setting aside loan loss provisions due to a new accounting rule appears to be driving the sector’s earnings negativity. However, this is mainly precautionary—whether actual loan losses result is questionable—and releases could boost earnings later. To see how distortionary this may be, S&P 500 earnings excluding Financials would be 14.2% y/y, more than doubling the headline growth rate.[iii] As for Consumer Discretionary and Communication Services, it isn’t a secret categories that saw huge growth during the pandemic (e.g., Internet & Direct Marketing Retail) are giving some of it back as travel and in-person services industries (like Hotels, Restaurants and Leisure and Automobiles) resume normal operations. In Communication Services, Interactive Media & Services drove its earnings decline as businesses’ online advertising failed to match last year’s strong post-COVID boom.

With Q2 earnings more mixed under the hood, the narrative that only Energy is seeing profits at the expense of all else breaks down. Also notable and cutting against widespread inflation and energy price-fueled recession fears: Every sector’s revenues rose in Q2. S&P 500 revenue growth was 13.6% y/y, and even excluding Energy, sales rose 8.8%.[iv] Corporate America has varying degrees of pricing power, but we think this demonstrates its overall resilience—and why stocks typically keep up with, or outpace, inflation over time (notwithstanding this year’s bear market, of course).

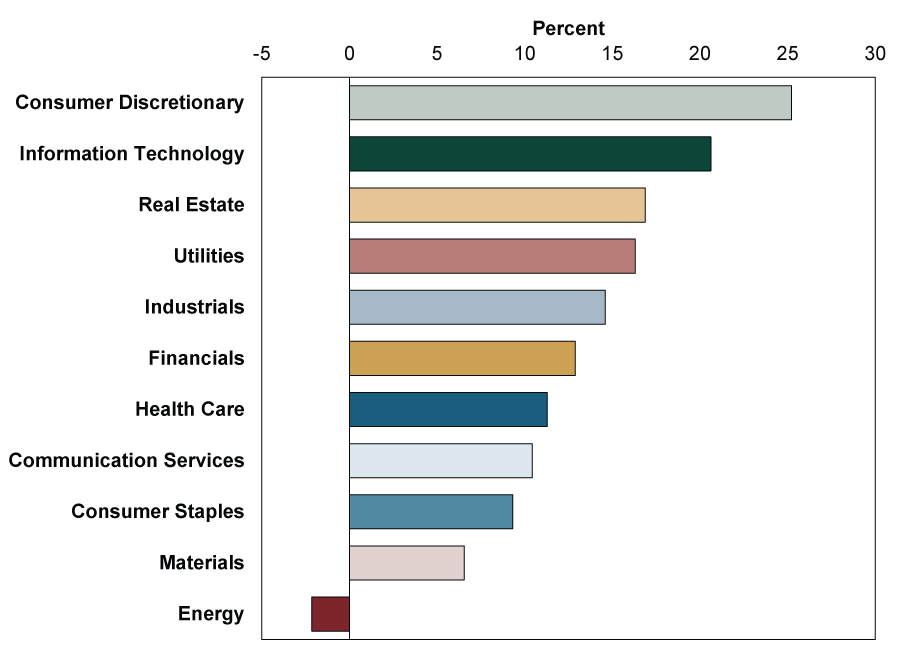

Overall, stocks seem to be looking beyond Q2’s pockets of earnings weakness. While markets swing on sentiment in the short term, over the longer term they look forward 3 to 30 months and assess how likely earnings outcomes compare with present expectations. Since June 16, the market’s assessment of future reality seems to have shifted markedly—if not turned a corner. Exhibit 2 shows Energy down -2.1% since stocks’ year-to-date low point, as crude oil’s price has fallen -25.7% from its March 8 peak.[v] It seems likely to us that markets are suggesting it may be harder for Energy to beat expectations. Conversely, though, the gains for every other sector since then suggest the expectations bar was low for them, particularly the ones hit most in the first half. Judging by ongoing earnings skepticism amid widespread recession chatter, a big gap between expectations and reality still exists.

Exhibit 2: S&P 500 Sector Returns, 6/16/2022 – 8/10/2022

Source: FactSet, as of 8/11/2022. S&P 500 sector total returns, 6/16/2022 – 8/10/2022.

We don’t know whether stocks’ rally from mid-June will mark a bull market recovery. That can be said only in hindsight, but it appears to us the conditions are in place. Sentiment remains dour, yet the evidence increasingly shows expectations have overshot reality to the downside. From here, we think that is what matters for stocks’ direction going forward: How will Q3 earnings—and beyond—fare against expectations? In our view, that is what investors should be focusing on, too.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis The New Tariffs in Town Are Still Old News2026-07-24

-

Expert Commentary This Week in Review | Market Volatility, Tariffs, SpaceX

2026-07-24

2026-07-24 -

Economics A Summertime Check-in on US Consumers2026-07-23

-

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today