Personal Wealth Management / Market Analysis

Accounting for (Rule) Differences

A new accounting rule is skewing bank earnings, but stocks see through it.

Among the lesser-seen worries in the cornucopia garnering investors’ ire lately hides S&P 500 Financials earnings’ -19.9% y/y plunge in Q1 2022—a highly unusual development during a stretch where most economic indicators are on an upswing and the vast majority of sectors are enjoying earnings growth.[i] The culprit, as The Wall Street Journal examined last weekend, is both simple and complex: A relatively new accounting rule is distorting earnings math bigtime. Interestingly, unlike the last time an accounting rule change distorted bank earnings, US Financials are actually holding up better than the S&P 500 overall. That is a change from 2007 – 2009, when another accounting rule destroyed bank balance sheets, triggering the global financial crisis. Understanding the rules’ differences can help investors get a better grasp of both past and present, in our view.

The rule in question is known as Current Expected Credit Loss, or CECL. As the name implies, it requires banks to account for all reasonably expected losses in their loan portfolio based on current economic conditions. Before CECL came on the scene, banks had to recognize—and provision for—loan losses only when they were imminent. While this system worked well for decades, following the 2007 – 2009 financial crisis, some industry critics argued banks were late to acknowledge trouble in their loan portfolios. In our view, they were misinterpreting the havoc wreaked by another accounting rule—FAS 157, the mark-to-market accounting rule, and its illogical application to illiquid and hard-to-value assets that banks never intended to sell. But cooler heads rarely prevail in these matters, so regulators decided the best way to shore up banks’ defenses would be to require them to provision for all expected credit losses over a loan’s entire lifetime.

What this means, in practice, is that banks must constantly adjust a given loan’s probability of default, usually based on current economic and financial conditions—and on the presumption that these conditions will last indefinitely. This has led to some outsized swings in banks’ earnings—swings that don’t totally reflect actual economic reality. In early 2020, at the height of lockdowns, this led to banks ratcheting up default projections and beefing up loan loss reserves accordingly. That was a big contributor to falling bank earnings early that year, as these provisions are basically paper losses. But a year later, with economies more open and an alphabet soup of fiscal and monetary assistance programs in place, expected defaults plunged, enabling banks to reduce their loan loss provisions—a paper gain. Now, high inflation and rising interest rates are again raising default projections, contributing to S&P 500 bank earnings falling -30.7% in Q1 2022.[ii] At some point in the future this will flip again, delivering a paper fillip to earnings.

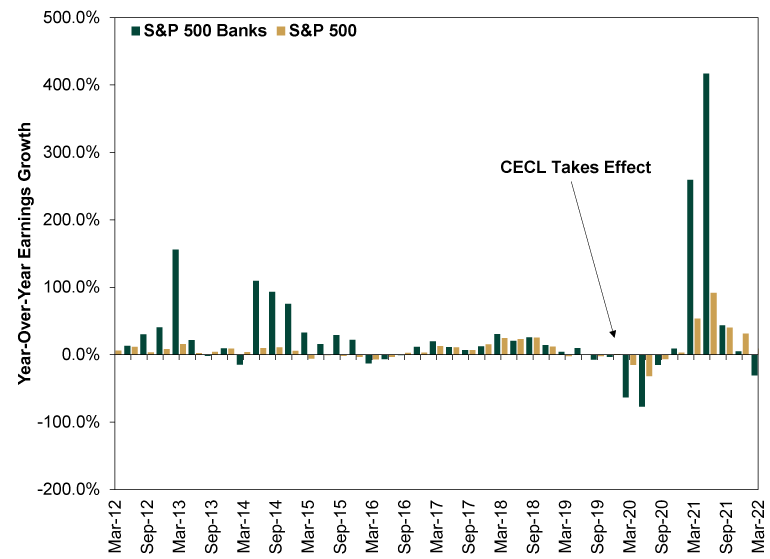

Before CECL took effect at the beginning of 2020, bank earnings rarely diverged sharply from total S&P 500 earnings—the main exception was in 2015 – 2016, when falling oil prices wrecked Energy earnings, skewing the total lower. But since CECL entered the fray, divergence has become the norm, as Exhibit 1 shows. Note the magnified swings during and after lockdowns, blowing away S&P 500 results to the up and down side.

Exhibit 1: CECL’s Bank Earnings Skew

Source: FactSet, as of 6/9/2022.

To understand why these swings represent some less-than-ideal side effects of the new rules, we will have to use a wee bit of jargon. When it comes to shoring up bank balance sheets, beneficial measures are usually what industry insiders would call “counter-cyclical”—banks would build up rainy day reserves in good times and draw them down in bad times. That is the purpose of a buffer: It is a cushion against illiquidity and insolvency in a crisis. This is what all the bank capital changes applied globally after the financial crisis sought to accomplish. CECL, by contrast, is what econ-types call “pro-cyclical”—it releases reserves in good times and adds them when conditions get tough. As a result, it makes net income look extra-good in happy times and extra-bad when things go south.

FAS 157 was also pro-cyclical. It required banks to value every asset on their balance sheet at comparable assets’ most recent market value—regardless of how hard these assets were to value, and regardless of whether banks intended to sell. So when hedge funds and other banks sold illiquid mortgage-backed securities at fire sale prices, it forced all banks to mark down similar assets on their balance sheets at similar discounts. That destroyed bank capital, forcing some banks to sell their own mortgage-backed securities in a pinch, which triggered more writedowns, then more fire sales, then more writedowns. Lather, rinse, repeat—with some institutions failing, others bailed out, and chaos reigning on Wall Street and Main Street alike until regulators suspended the rule’s application to hold-to-maturity assets. This was the vicious cycle that did in Lehman Brothers in September 2008.

CECL and FAS 157 both had outsized impacts on bank earnings. So why did FAS 157 cause a crisis while CECL has mostly generated sighs and annoyed soundbites from bank CEOs? For one, as mentioned earlier, FAS 157 wiped out bank capital. CECL doesn’t—it is a paper loss reflecting an increase in cash reserves earmarked to guard against expected future defaults. Two, loan losses weren’t at issue in the global financial crisis. According to former FDIC head Bill Isaac, who crunched the numbers in his excellent book on that period, Senseless Panic, total loan losses at this time were only about $200 billion. That is big in a vacuum, but not inherently large enough to wallop the global economy. But FAS 157 magnified this figure into nearly $2 trillion in exaggerated and unnecessary writedowns—that was the wallop. It destroyed bank capital used to underpin lending capacity. Credit froze. CECL just doesn’t compare.

Overall, we are inclined to agree with JPMorgan Chase CEO Jamie Dimon’s assessment of the situation. When announcing bumper results in Q1 2021, tied largely to the release of loan loss provisions set aside under CECL rules during lockdowns, he put it bluntly: “We don’t consider it profit. It’s ink on paper.”[iii] In our view, markets see this too. In 2008 and 2009, the fire sales and writedowns were a giant shock hitting a core aspect of banks’ operations. So were the government’s haphazard attempts to manage the situation, which stoked more uncertainty. But under CECL, markets are pretty good at sussing out how banks’ models will extrapolate current conditions into expected defaults. They can also delineate between actual and paper profits and losses, and they know CECL isn’t erasing capital in tough times.

Mind you, we don’t think CECL is the smartest rule ever applied. In addition to its pro-cyclicality, it essentially requires banks to forecast future loan losses by extrapolating the present economic and financial conditions in perpetuity. The past two years’ swings show the folly in this, as rapidly changing conditions brought rapidly changing CECL provisions. Then too, any number of variables could affect a borrower’s default risk over the entire lifespan of a loan. Far-future developments like this are simply unknowable.

So, it is a rather unhelpful rule. But thanks to markets’ efficiency and some key differences with FAS 157, it isn’t inherently destructive. Mostly, it is an academic curiosity that we encourage investors to be mindful of when assessing banks’ earnings.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis The New Tariffs in Town Are Still Old News2026-07-24

-

Expert Commentary This Week in Review | Market Volatility, Tariffs, SpaceX

2026-07-24

2026-07-24 -

Economics A Summertime Check-in on US Consumers2026-07-23

-

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today