Personal Wealth Management / Financial Planning

The ABCs of BDCs: A Primer on Business Development Companies

Even if you are bullish on often high-dividend yielding business development companies, we'd suggest your exposure should be very limited.

In recent years, low global interest rates have some retirement investors wondering exactly how they can fund withdrawals, leading many to search for yield in tiny, obscure corners of the marketplace. While we've discussed some of these corners before, one we haven't discussed is business development companies, or BDCs. Without further ado, here is our primer on BDCs and why we don't believe they should play a big role in most investors' portfolios, regardless of their withdrawal needs.

What Are BDCs?

In 1980, Congress amended the Investment Company Act of 1940 establishing the BDC structure (begins in Section 54) as a means to drive long-term capital to small businesses. These firms pool capital raised from investors to fund debt or equity stakes in small- to mid-sized private businesses. They are sometimes described, a bit inaccurately, as ETFs of private companies.[i] The approach is similar to Real Estate Investment Trusts (REITs), although BDCs obviously are investing in a wide range of underlying assets and types of firms, not merely real estate related assets. Like REITs, some investors have been attracted to BDCs in recent years because many sport lofty dividend yields.

The private companies these firms fund vary dramatically in type. Some are pure-play BDCs specializing in one industry or another. Others fund an array of business types without a discernible specialty. While this will drive some differences from BDC to BDC, the important thing to remember is the business BDCs are involved in: banking.

While it isn't traditional banking, consider that banks are in the business of funding other businesses. Loan portfolios differ from one another fairly dramatically. While this can clearly mean certain banks are more subject to specific drivers (e.g., a Texas oil patch bank likely has much more exposure to the oil industry than, say, a megabank), in a fundamental way, the business model is the same: Banks employ expertise in assessing a borrower's credit quality to determine whether or not the reward of extending them credit justifies the risk. BDCs do the same thing, with the major difference being that they take either a debt or equity stake, aren't subject to the same regulation and are required to pass profits (and taxes) through to shareholders. But as a core model, funding is basically banking, and, as we'll discuss later, the similarities to banks do not stop here.

Differentiating BDCs

Before we go further, let's make an important distinction. There are two main types of BDCs: Traded BDCs, which are listed on a major exchange and trade like stocks, and non-traded BDCs. Non-traded BDCs aren't listed on any exchange, instead raising capital through private markets-reminiscent of non-traded REITs. Also reminiscent of non-traded REITs, they lack liquidity and are subject to vastly different regulatory oversight. And, as noted here, non-traded BDCs (again, like non-traded REITs) often pay salespeople high commissions while providing the investor no discernible structural edge over traded BDCs. These factors make non-traded BDCs unattractive, in our view. The rest of our commentary will exclusively address traded BDCs, as we do not see a logical, compelling reason to buy a non-traded BDC.

BDCs and Dividends

While not universally true, BDCs frequently have high dividend yields-currently, the median is 12.4%.[ii] That is likely what attracted some yield-chasing investors during the current bull market. Hence, in all likelihood, why fully 30 of the 52 BDCs we identified listed or adopted the structure in the last five years, while interest rates were at zero. When Wall Street senses rising demand, it boosts supply.

Now, maybe those yields seem attractive, but there are a few key caveats. First, consider tax treatment. BDCs qualify under special IRS statutes that require them to distribute most of their earnings, like a mutual fund or REIT. This has downstream implications for investors, too. For good and, occasionally, ill, BDC dividends can be taxed:

- As income. The share of the BDC dividend that is sourced from fees and/or interest is taxable at ordinary income rates.

- As dividends. This is the same rate at which standard US dividends are taxed, which could be either qualified or non-qualified. Qualified dividends are taxed at a preferential rate in line with long-term capital gains. Non-qualified are taxed at ordinary income rates.

- As a return of capital. This isn't investment return. It is a return of money you put in, and as such, isn't taxed. However, it will reduce your cost basis, exposing you to greater potential capital gains taxes should you sell.

Like any firm, BDC dividends are far from set in stone. BDCs can-and have-cut dividends during periods of economic stress. When the 2008 financial crisis intensified in Autumn 2008, many BDCs cut their dividends. Some large BDCs outright eliminated dividend payments after the crisis hit. This is yet another similarity to banks, whose dividends were stressed during the crisis.

A Niche Investment

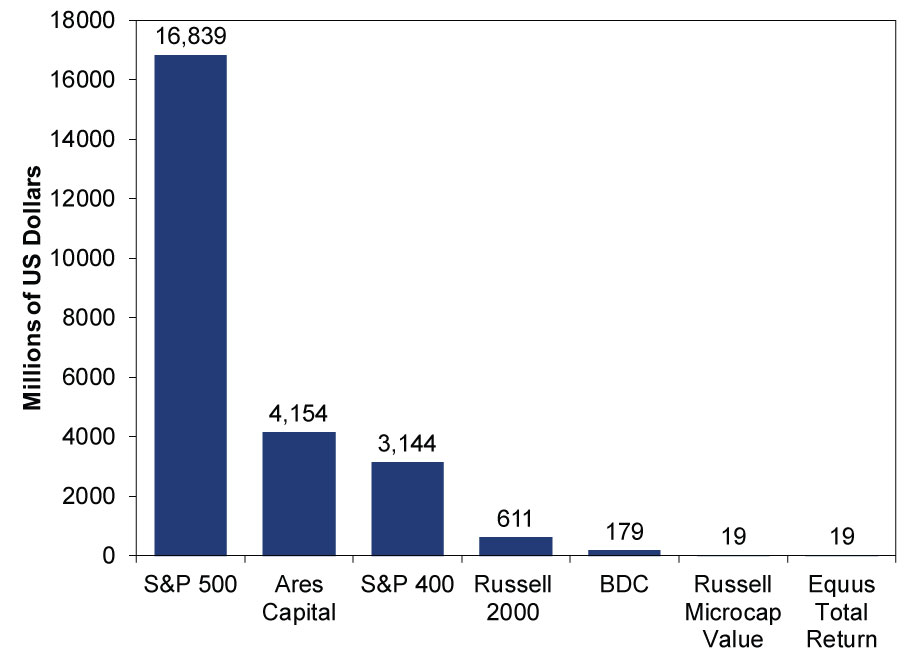

Traded BDCs are not new, but they are a niche investment. Most of these firms are extremely small. Median BDC market capitalization is $178.9 million-tiny. The largest firm by market cap is Ares Capital at $4.15 billion-the size of a typical mid-cap stock. Only six exceed $1 billion-American Capital, Apollo Investment Corp., Ares, FS Investment Corp., Main Street Capital Corp. and Prospect Capital Corp. The smallest listed BDC is Equus Total Return at $19.1 million. Cumulatively, the entire BDC marketplace has a capitalization of under $27 billion, big enough to rank 147th in the S&P 500. These are small firms in a small subsector. Exhibit 1 puts this in perspective, comparing these largest and smallest BDCs to the median market capitalization of the BDC universe and a few stock indexes.

Exhibit 1: BDCs Are Small Cap

Source: Fisher Investments Research, FactSet, Russell Indexes, Standard and Poor's, as of 2/18/2016. Index figures are median market capitalization; BDC is the median of all 52 listed BDCs.

BDCs and Diversification

Given the small footprint in markets, we believe any investment in BDCs should be limited to an extremely small portion of your portfolio. As we often note on these pages, yield chasing is a dangerous and unnecessary practice for investors, even those with cash flow needs. In the case of BDCs, a heavy weighting to BDCs means a huge overweight to equity-like securities that amount to about 0.1% of listed US market capitalization.[iii] And a group that is extremely biased to small-cap securities that trade like banks.

Since its 6/29/2007 inception, the correlation coefficient between the Market Vectors US Business Development Company Index (a gauge of 22 major BDCs) and the Russell 2000 Financial Services sector is 0.86.[iv] High! Another measure of how related two indexes are, the R-squared, is 0.74.[v] This is slightly higher than BDC's correlation to stocks generally, suggesting BDCs trade more like bank stocks than the general market.

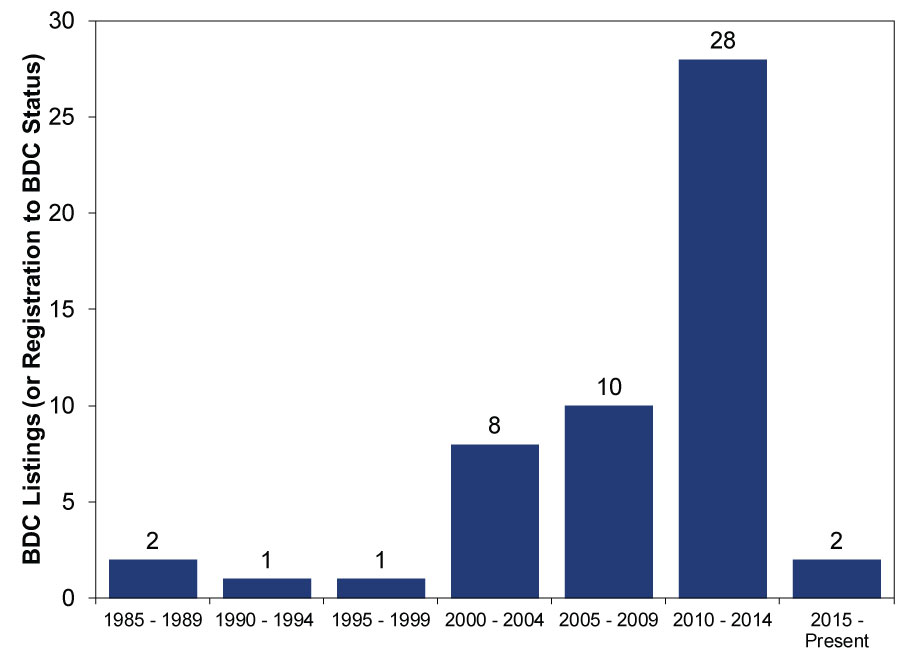

Now, a drawback to these data is they cover only nine years, so we can't test these correlations any further than 2007, and that includes a period when bank fears were the dominating theme. That may skew the above-noted correlations, but it isn't possible to know. This is yet another limitation of BDCs, which lack a deep history to draw on. By our count, only five currently trading BDCs have existed through more than one recession, and the vast majority of currently traded BDCs have listed since 2005. (Exhibit 2) There isn't a large enough dataset doing back far enough to test correlations further with any confidence.

Exhibit 2: Most BDCs Are Relatively New

Source: FactSet, SEC.gov's Edgar Database. Date of first trade after filing for BDC status.

BDC Returns

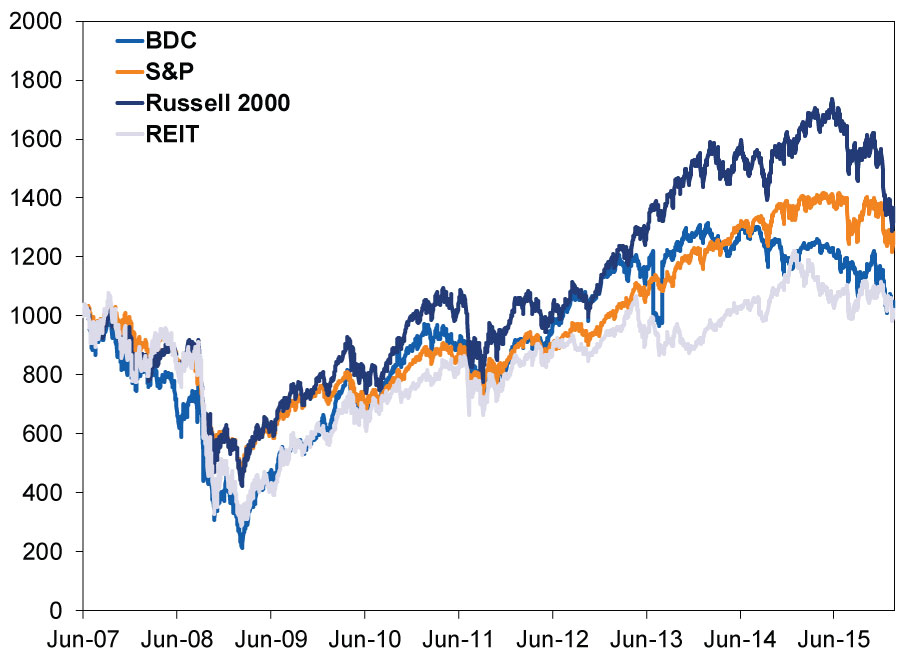

In the last downturn, the industry was hard-hit, falling more than stocks and REITs. Exhibit 3 shows the Market Vectors US BDC Index since its June 29, 2007 inception plotted against the S&P 500, Russell 2000 and MSCI US REIT Index. All include reinvested dividends and are indexed to 1000 at the period start.

Exhibit 3: BDC Returns

Source: FactSet, as of 2/18/2016.

Now, that chart's long time frame may obscure your ability to see the year-by-year returns. Exhibit 3 unpacks this into annual total returns from 2008 - 2016 (to date).

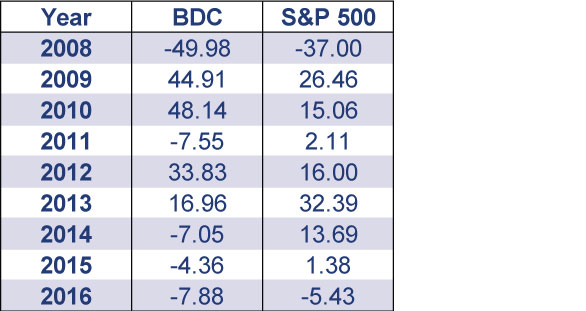

Exhibit 4: Annual Total Returns

Source: FactSet, as of 2/18/2016.

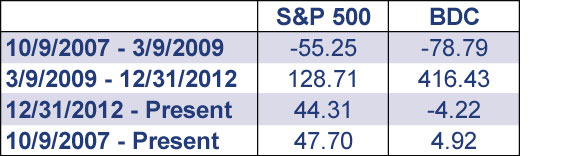

You may note the huge BDC returns in 2009, 2010 and 2012. Since this bull market began on March 9. 2009, BDCs have cumulatively outperformed the other categories shown. However, quite literally all of that outperformance was in the early stages of the bull-in part, likely a rebound from their huge, nearly -80% decline in the 2008 bear market. Also, it's fairly likely some were attracted to dividends. Others may have seen BDCs as well positioned to capitalize on healing credit markets, given they didn't face the regulatory overreach confronting banks.

However, since 2012's close, including dividends, they've lagged. Cumulatively, from the pre-financial crisis stock market high, BDCs have trailed both the S&P 500 and the Russell 2000. As with any narrow, undiversified investment, BDCs have seen massive volatility in both directions, a tough ride for anyone to stomach.

Exhibit 5: Cumulative Total Returns, S&P 500 and BDCs

Source: FactSet, as of 2/18/2016.

As bull markets mature, small cap tends to fall out of favor and the largest firms gain primacy. This suggests tiny firms like BDCs won't come back into favor any time soon. However, perhaps you disagree. That's fine! But given the nature of BDC's businesses, the tiny size of this market segment and other factors, even those bullish on the sector should limit their exposure to a tiny slice of their overall portfolio.

[i] We are not a huge fans of this description, as ETFs are designed to give you instant diversification. BDCs are designed to give you entry into an illiquid and usually inaccessible asset class. And, many BDCs acknowledge their investment strategy is not diversified in their SEC filings.

[ii] Source: FactSet, as of 2/18/2016.

[iii] Total market capitalization of all 52 listed BDCs as a percentage of the MSCI USA Investible Market Index market capitalization.

[iv] Source: FactSet, as of 2/18/2016.

[v] Ibid.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis The New Tariffs in Town Are Still Old News2026-07-24

-

Expert Commentary This Week in Review | Market Volatility, Tariffs, SpaceX

2026-07-24

2026-07-24 -

Economics A Summertime Check-in on US Consumers2026-07-23

-

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today