Personal Wealth Management / Market Analysis

The Bank of Japan Keeps Swimming Upstream

The weak yen is increasingly a sore spot with Japanese businesses.

Central banks worldwide are raising interest rates fast and furious, with even the Swiss National Bank getting in on the action. Yet there is one major outlier: Japan, where the Bank of Japan (BoJ) remains wedded to negative interest rates and its yield-curve control (YCC) program even as the weak yen creates big headaches for businesses and politicians alike. Meanwhile, Japan isn’t really playing its traditional defensive role during global stocks’ bear market, and we think the BoJ’s misadventures go a long way toward explaining why. Let us discuss.

The BoJ implemented YCC—which sets targets for 10-year Japanese Government Bond (JGB) yields—in September 2016. Then, the BoJ targeted a 0% 10-year yield, though most thought officials allowed fluctuations within a bandwidth of +/- 0.1 percentage point (10 basis points, or bps). The BoJ pursued this strategy in part because Japanese banks complained the BoJ’s quantitative easing (QE) and negative policy rate—which pulled 10-year yields below zero—made it all but impossible to lend profitably. At the time, we called the BoJ’s policy update a “stealth taper” since it required the bank to let 10-year yields rise, implying fewer bond purchases. Since its implementation, the BoJ has widened its target trading bandwidth twice: in July 2018 (up to +/- 20 bps) and March 2021 (up to +/- 25 bps).

This target is effectively an interest rate peg, which is inherently unstable. Pegs work as long as the targeted rate isn’t far off what the market-driven rate would be. Once markets start moving, though, it takes extraordinary intervention to preserve the fixed value—and that is happening now. As bond yields globally climbed this year, 10-year JGB yields followed, reaching the BoJ’s 0.25% ceiling. Market forces have tried to push Japanese yields even higher, prompting the BoJ to announce in late March that it would buy an unlimited amount of 10-year JGBs to keep yields at or below 0.25%. Without that extraordinary intervention, 10-year JGB yields would likely be far higher than where they are today.

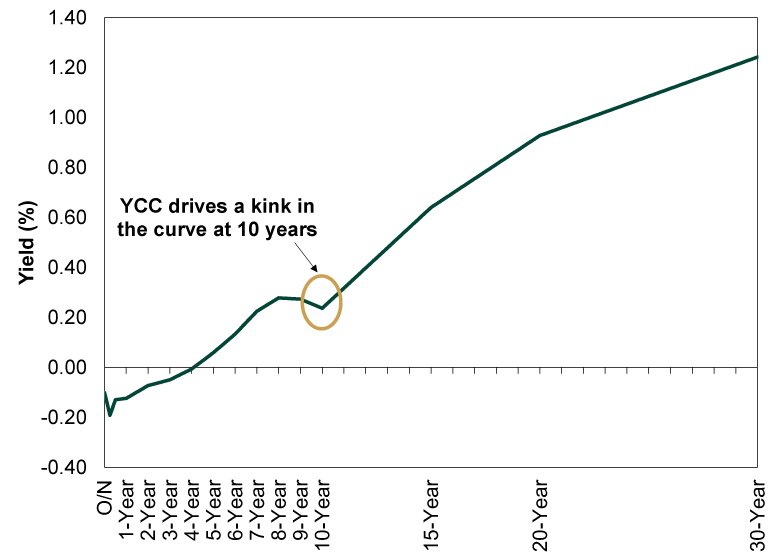

One way to see this: dislocations in Japan’s yield curve. Typically, central banks set the short end of the curve, with market forces mapping out the rest according to inflation expectations, perceived credit risk and other factors affecting demand. Even in nations that have ongoing QE programs, market forces retain influence. But in Japan, the 10-year yield is pegged while other maturities are market-set. This has created a weird kink, where 7 – 9 year JGB yields are right around 10-year yields—and longer maturities are much higher. It is easy to imagine that, left to its own devices, Japan’s 10-year yield would be at least 0.50% by now, if not higher. (Exhibit 1)

Exhibit 1: The BoJ Is Distorting the Japanese Yield Curve

Source: FactSet, as of 6/23/2022. Yields as of 6/22/2022.

Maintaining the cap has also caused yen to weaken. All else equal, money flows to the highest-yielding asset. By artificially keeping yields down, the BoJ has prompted investors to ditch JGBs for higher-yielding securities elsewhere in the developed world, wrecking demand for yen.

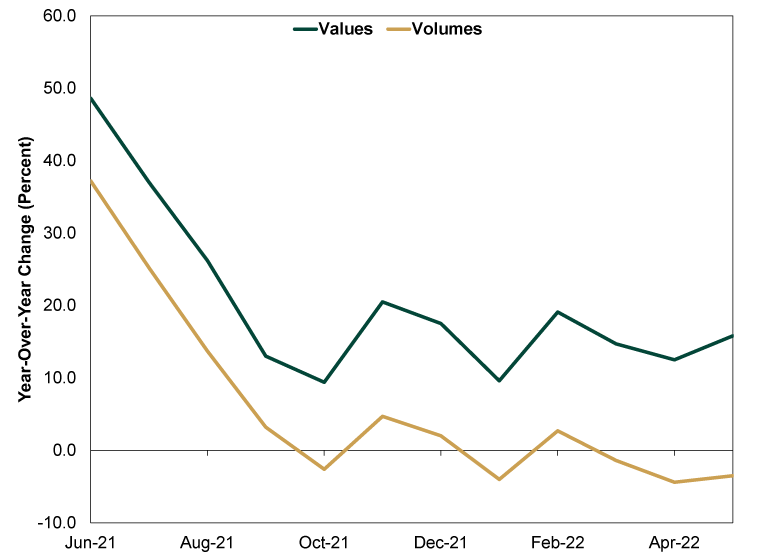

There once was a time when policymakers would have cheered this. The BoJ sought a weak yen a decade ago through QE—part of former Prime Minister Shinzo Abe’s “Three Arrows” economic revitalization program. According to the BoJ’s thinking, a weak yen would boost exports while also helping lift the country out of its entrenched deflation. That didn’t happen. Rather than cut prices to spur demand in foreign markets and buoy export volumes (amount of stuff traded), Japanese exporters kept prices constant. That gave them more yen for every dollar of merchandise sold overseas (which boosted export values). The upshot: The weak yen didn’t lead to higher production or economic growth at home then, and it doesn’t seem to be doing so now. Japanese companies still appear to be living off currency translation profits instead of increasing production to grab overseas market share. (Exhibit 2)

Exhibit 2: Japanese Exports, June 2021 – May 2022

Source: Ministry of Finance, as of 6/16/2022.

But the real trouble comes on the import side. A weak yen makes imports more expensive—a big deal for Japan since the country imports most of its oil, which is priced globally in dollars, and other energy products. Today’s elevated costs of energy, food, metals and other commodities are driving prices higher broadly: Japan’s headline CPI rose 2.5% y/y in May, the first time it topped 2% since 2008.[i] But while policymakers wanted inflation—they have long struggled to hit their annual target of 2%—they wanted it as a byproduct of a faster-growing economy, not a side effect of energy costs. Consider: Excluding volatile food and energy prices, May CPI rose just 0.8% y/y.[ii]

High energy prices combined with a weak yen are weighing on businesses and households. A recent survey found nearly half of respondents reported the yen’s weakness as bad for business, and the government is on notice, as inflation is set to be a major campaign issue in July’s upper house elections.[iii] In the Liberal Democratic Party’s (LDP) campaign manifesto, one of the top two items is to take “powerful and flexible” steps to ease the pain from rising prices. Prime Minister Fumio Kishida’s government has created a task force to curb food prices and energy bill burdens. BoJ chief Haruhiko Kuroda apologized recently for comments about inflation’s impact on households—indicating how politically sensitive inflation has become in Japan. It wouldn’t surprise us if this all showed up in next month’s election results, though to what extent remains unclear.

With the rest of the developed world raising interest rates, Japan is the proverbial salmon swimming upstream. For globally minded investors, the strong US dollar relative to the Japanese yen matters, as there is a sharp divergence in Japanese stock returns based on currency. The MSCI Japan is down -6.5% in yen compared to -20.9% in dollars.[iv] Moreover, with the headwinds looming over businesses, Japan isn’t playing its typical defensive role during bear markets—it was roughly in line with global stocks year to date as of Wednesday’s close. Now, we think owning big Japanese multinationals still makes sense from a diversification standpoint. They can use their profits from currency conversion to offset some energy and import costs, so they won’t necessarily suffer as big a haircut as domestic-oriented businesses. However, Japanese stocks aren’t likely to provide the same cushion we would expect during a global market downturn.

[i] Source: FactSet, as of 6/23/2022.

[ii] Source: Japan Cabinet Office, as of 6/23/2022.

[iii] “Nearly Half of Japan Firms See Weak Yen as Bad for Business, Survey Shows,” Staff, Reuters, 6/14/2022.

[iv] Source: FactSet, as of 6/22/2022. MSCI World Index returns with net dividends, in JPY and USD, 12/31/2021 – 6/21/2022.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets — July 27 - July 312026-08-03

-

Expert Commentary 3 Things You Need to Know This Week | US Jobs, Trade Balance, Earnings Reports

2026-08-03

2026-08-03 -

Market Analysis Digging Into Last Week’s Fed ‘Credibility’ Concerns2026-08-03

-

Expert Commentary This Week in Review | Fed Meeting, US GDP, Eurozone GDP

2026-07-31

2026-07-31

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today