Personal Wealth Management / Market Analysis

The Dollar’s Reserve Currency Status Is No Sure Privilege

Reheated reserve currency fears remain overblown.

How do you know financial news has hit a slow patch? When pundits start musing about the dollar losing its reserve currency status and the big problems that would allegedly follow. This time, the chatter centers around China, India, Russia and rogue nations’ efforts to build dollar-less transaction networks in the wake of the West’s sanctions on Russia’s assets and international trade. Some argue China’s experiments with a central bank digital currency (CBDC) will accelerate the shift to a post-dollar world or a “bipolar” system where the US and Western allies stay dollarized and nations in China’s sphere don’t. Underlying all of it is the presumption that without its “exorbitant privilege” of reserve currency status, the dollar will sink, US interest rates will soar and market mayhem will ensue. We doubt it.

The dollar’s reserve currency role is two-pronged: It represents the majority of the world’s foreign exchange reserves, and it is the primary medium for international transactions. Last year, as the West responded to Vladimir Putin’s Ukraine invasion with sanctions, we theorized that cutting Russia off from its dollar reserves could incentivize a broader shift away from the dollar. That hasn’t happened: In Q3 2022, the latest data available, the dollar represented 55.5% of total reserves, up a smidge from 54.8% in Q4 2021.[i] The amount of dollars in reserve fell by $644 billion during this span, but that stemmed mostly from countries selling dollars to support their own currencies as the dollar strengthened, and it coincided with a $1.32 trillion drop in total reserves.[ii] So, this seems to us like typical currency management, not a preferential shift.

Where there has been a small but arguably notable shift is in the dollar’s transaction use—namely in Russia’s commodity sales to China, India and other partners. Rather than invoicing its clients in dollars to get hard currency, Russia has reportedly taken payment in rupees, yuan and the United Arab Emirates’ dirhams.[iii] India and China have also taken several steps toward internationalizing their currencies, and China is trying to drum up business for the Shanghai Petroleum and Natural Gas Exchange. Now, the Bank for International Settlements’ data don’t show much change yet. It shows the dollar’s share of global forex transactions hovering stable at just under 90%.[iv] (Note: This is out of 200%, as there are always two sides to a currency trade.) But there is an effort at least.

The digital yuan, supposedly, could accelerate this. In addition to being a shiny new toy that developed nations haven’t kept up with,[v] it is also a payment system that works outside the US-controlled global network. As one analyst explained, wider use of the digital yuan and other CBDCs “could enable central banks in the global east and south to serve as foreign exchange dealers to intermediate currency flows between local banking systems, all without referencing the dollar or touching the western banking system.”[vi]

In theory, this holds up well enough. But we think reality would prove much messier. For one, it seems far from certain that China wants the yuan to be a fully internationalized currency used in half the world’s transactions. Enabling this would mean surrendering the People’s Bank of China’s tight control over capital flows, which has long been key to the country’s economic management. Two, relying on digital yuan seemingly runs counter to Russia et al’s supposed motivation for getting away from the dollar. If the point is seeking freedom from another nation’s control over what you buy and sell, then why would you flock to a digital yuan that is completely under government control and tied to the country’s social credit system? It would arguably be even easier to disable digital currencies than it was to block Russia’s access to its overseas reserves and the SWIFT payment network. Those decisions required unanimity among Western powers. Hitting Russia with Computer Says No when it tries to access its digital yuan wallet seems easier. If predictability and stability are the goal, we don’t see how this qualifies.

And if we are wrong? If the dollar loses a lot of market share? Perhaps it would finally enable investors to get over one of their longest-running fears. Everyone draws parallels with the UK’s experience after the Suez Crisis ended the pound’s dominance. But that was all about an actual empire disintegrating and the defense of a currency peg, which is always inherently unstable. The US today isn’t analogous. Then too, losing its reserve currency status didn’t stop the UK economy from growing and thriving—nor UK stocks from rising—over the rest of the 20th century and beyond.

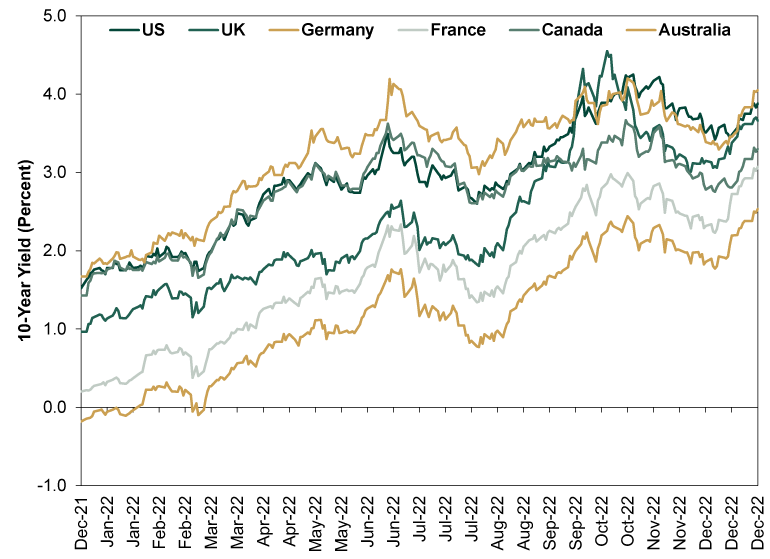

We suspect the US would do just fine if the dollar lost global market share. Contrary to widespread belief, there is precious little evidence that the so-called exorbitant privilege actually exists. For one, the US Treasury doesn’t get a brokerage fee every time other countries transact with the dollar. Two, “dollarization” doesn’t really translate to interest rates or the dollar’s strength. We think last year proves the point: The dollar remained top dog in international reserves, the dollar hit generational highs versus a broad currency basket, and the US … had some of the highest long-term interest rates among major developed nations for most of the year.

Exhibit 1: What Exorbitant Privilege?

Source: FactSet, as of 1/11/2023. Benchmark 10-year government bond yields, 12/31/2021 – 12/31/2022.

Some will inevitably say “yah, but the US’s would be higher if the dollar wasn’t the reserve currency.” Sure, maybe—counterfactuals are always question marks. But Germany and France would seem to suggest otherwise, given their lower yields. This is rather noteworthy given all the concerns about French debt these days. Ditto for UK yields, which surpassed US yields only when a very short fiscal policy freakout triggered margin calls and forced selling at pension funds. The UK has a weaker currency and far more chatter about current account deficits and general post-Brexit socioeconomic handwringing. The pound is also just 4.2% of the world’s forex reserves.[vii] If investors overall are so happy to buy UK Gilts despite all of the alleged (and in our view, misperceived) drawbacks, we suspect they would be delighted to continue owning the world’s biggest, deepest, most liquid government bond market.

[i] Source: IMF Currency Composition of Official Foreign Exchange Reserves, as of 2/6/2023.

[ii] Ibid.

[iii] Curiously, the dirham is pegged to the dollar. So the UAE likely holds a heckuva lot of dollars in reserve anyway.

[iv] “Revisiting the International Role of the US Dollar,” Bafundi Maronoti, Bank for International Settlements Quarterly Review, 12/5/2022.

[v] Not that we are arguing they should.

[vi] “Great Power Conflict Puts the Dollar’s Exorbitant Privilege Under Threat,” Zoltan Pozsar, Financial Times, 1/19/2023.

[vii] See Note i.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis The New Tariffs in Town Are Still Old News2026-07-24

-

Expert Commentary This Week in Review | Market Volatility, Tariffs, SpaceX

2026-07-24

2026-07-24 -

Economics A Summertime Check-in on US Consumers2026-07-23

-

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today