Personal Wealth Management / Market Analysis

Torturing Valuations Doesn’t Yield Actionable Insights

P/E ratios still aren’t predictive.

What a difference a month makes. After a hot January seemingly sparked some very cautious optimism that stocks’ worst times were behind them, a mildly negative February seems to have restored pessimism. Rate hikes, lingering inflation and geopolitics took turns weighing on sentiment, echoing last year, but they got a new friend: valuations. The latest example? A Wall Street Journal article this week arguing bonds will outperform as stocks take years to crawl back to breakeven—all because the S&P 500 and MSCI World Index’s above-average price-to-earnings (P/E) ratios imply returns will be weak from here.[i] But valuations aren’t predictive, especially early in a bull market.

We touched on the folly of emphasizing valuations early in a bull market a couple of weeks ago when we dove into concerns about stocks’ earnings yield (the P/E’s inverse) falling near and, depending on maturities, below bond yields. We think it is still too early to know for sure if October 12 marked the bear market’s low and a new bull market has indeed begun, but it is worth reiterating that stock valuations are behaving as we would expect early in a bull market. That is to say, they are up. A lot. Late in a bull market, a fast increase like this might indeed signal sentiment got too hot too quickly. But early in a bull market, it is mostly math.

Stocks are leading indicators. They move ahead of earnings, usually pre-pricing expected profitability about 3 – 30 months out. As a result, stocks usually start recovering from a bear market before the earnings decline has run its course. This happened in 2009 and 2020. And it may explain what is happening now. With 484 S&P 500 companies reporting as we write, Q4 2022 earnings are down -4.9% y/y.[ii] Analysts project another small decline for Q1 and Q2. This means that while the P is up, the E is dropping. A larger numerator divided by a smaller denominator yields a larger quotient—a larger P/E ratio.

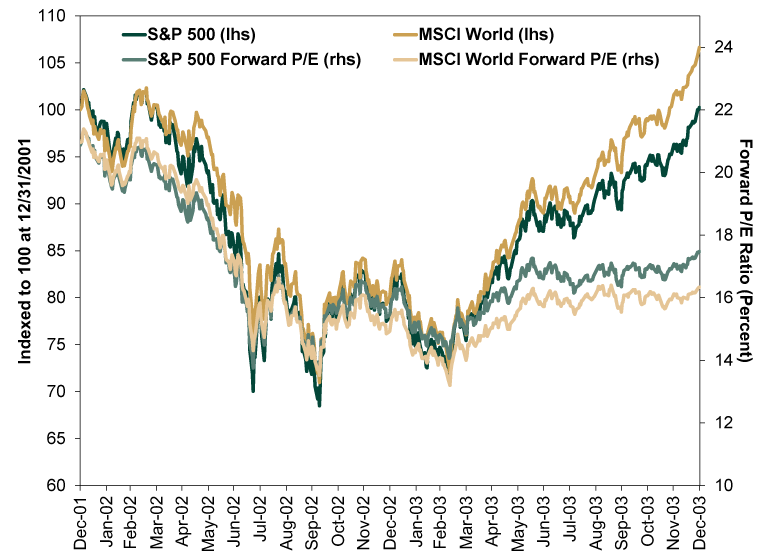

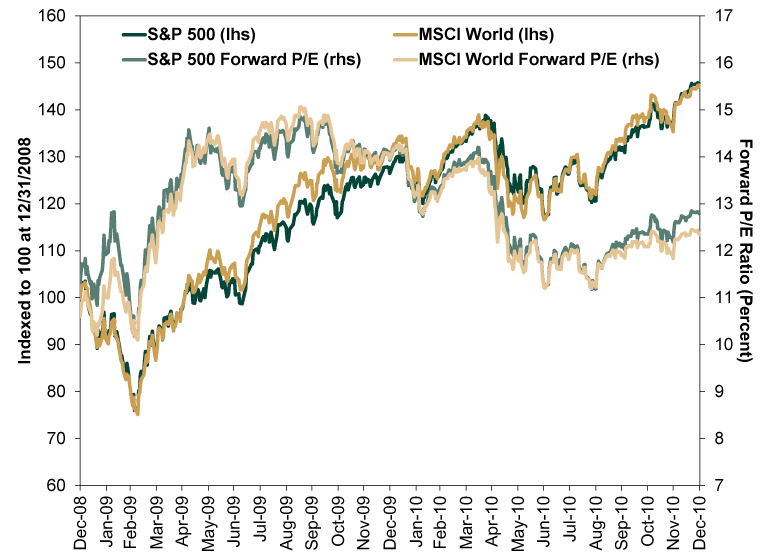

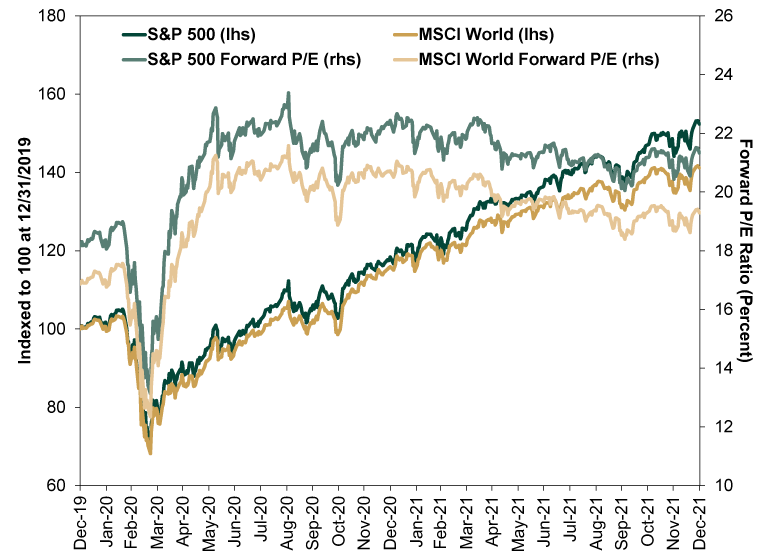

We saw this in 2002, 2009 and 2020—the early stages of the previous three bull markets. The effect was most apparent in trailing P/Es, which compare prices to the past 12 months’ earnings. But it also showed up in forward P/Es (price divided by expected earnings over the next 12 months), as recent earnings tend to influence expectations. Exhibits 1 – 3 show S&P 500 and MSCI World Index forward P/Es and returns in these young bull markets—note the immediate spike in P/Es, followed by a long drift lower—despite rising stock prices. Contrary to popular belief, stocks don’t need to fall for valuations to come down. Sometimes, it is just a matter of the E catching up to what the P already priced in.

Exhibit 1: Stocks and P/Es After the 2000 – 2002 Bear Market

Source: FactSet, as of 2/28/2023. MSCI World Index return with net dividends, S&P 500 total return, and S&P 500 and MSCI World forward P/E ratios, 12/31/2001 – 12/31/2003.

Exhibit 2: Stocks and P/Es After the 2007 – 2009 Bear Market

Source: FactSet, as of 2/28/2023. MSCI World Index return with net dividends, S&P 500 total return, and S&P 500 and MSCI World forward P/E ratios, 12/31/2008 – 12/31/2010.

Exhibit 3: Stocks and P/Es After the 2020 Bear Market

Source: FactSet, as of 2/28/2023. MSCI World Index return with net dividends, S&P 500 total return, and S&P 500 and MSCI World forward P/E ratios, 12/31/2019 – 12/31/2021.

So suffice it to say, we don’t view valuations today as a sign stocks will crawl over the foreseeable future, never mind take eons to recapture their January 2022 peak. Even in the Wall Street Journal piece, the main evidence for a long slog was inflation-adjusted returns, which are a meaningless construct. If inflation is a factor influencing returns, then we don’t think it makes sense to adjust returns for inflation—it isn’t even clear what you would use. CPI? PPI? The PCE price index? GDP deflator? Then too, stocks are a reflection of corporate earnings, which are also nominal. We all earn nominal returns, take nominal cash flows, pay taxes on nominal capital gains and pay nominal expenses. Inflation-adjusting historical returns anchors them to the past and distorts the present. In our view, it is an academic exercise with no real-world relevance.

So if your basis to shift out of stocks now is valuations and a forecast for low inflation-adjusted returns looking forward, we don’t think that is rock-solid. And, mind you, we say this having nothing against bonds—particularly for investors who have shorter time horizons, higher cash flow needs and/or less comfort with short-term volatility. But that is a long-term asset allocation decision and, in our view, shouldn’t hinge on a market outlook. Rather, your asset allocation should be designed to reach your goals regardless of the market’s wobbles along the way. And, to us, the main reason to own bonds is to mitigate expected short-term volatility, not to maximize returns.

Rather than get hung up on valuations and the near-term outlook, we think it is best to ask and answer a simple question: If you need equity-like returns to reach your long-term goals, does it make sense to sit out of stocks during a bull market? To earn stocks’ returns, you must actually own stocks, particularly when they are going up. Dialing down stock exposure now—and raising bond exposure—could mean reducing long-term return potential for that pool of money. If your goals haven’t changed, we doubt that is a beneficial move.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary This Week in Review | Fed Meeting, US GDP, Eurozone GDP

2026-07-31

2026-07-31 -

Economics Q2 US GDP’s Stealthy Strength2026-07-31

-

Market Analysis Don’t Fret the EU’s Low Summertime Gas Storage Levels2026-07-31

-

Economics On Fires and GDP2026-07-30

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today