Personal Wealth Management / Market Analysis

Tying Up SLOOS Ends

On deposits, lending and bank size.

Monday’s Fed Senior Loan Officer Opinion Survey (SLOOS) was so chock full of interesting information that it was impossible to highlight all the relevant bits in a single article—so we didn’t. Yesterday we took a big-picture look at how banks were tightening credit standards after March’s regional bank failures and which risks they were eyeing. Today we will go a little more granular and square the survey responses with the latest lending and deposit data, which show how reality is stacking up against expectations—and thus help explain stocks’ resilience in light of bank fears.

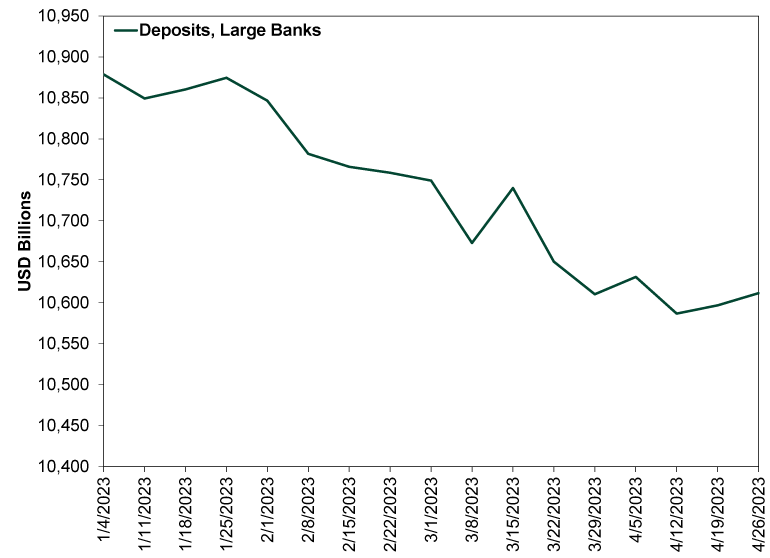

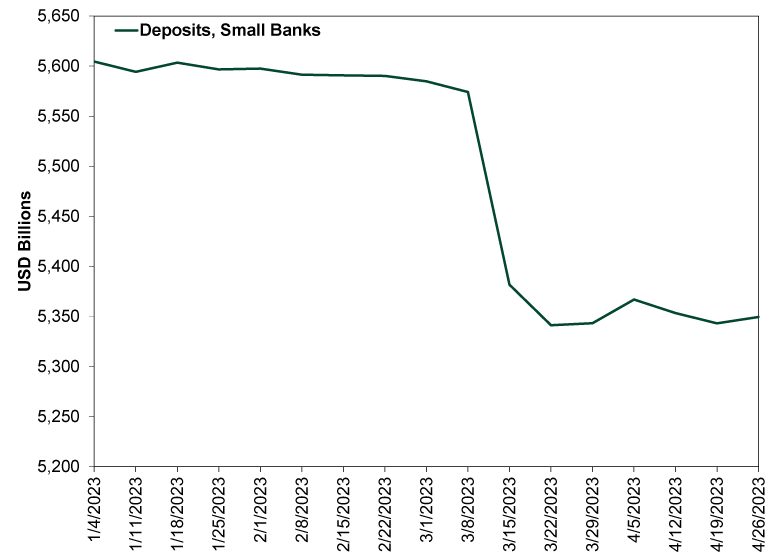

Let us start with deposits, which fell as large account holders reassessed deposits over the FDIC’s $250,000 per account holder maximum. Exhibits 1 and 2 show weekly deposits this year to date, broken down into large and small banks. As you will see, the flight from small banks was more pronounced, but seems largely like a one-time event. The flight appears to have stopped, which is yet more evidence a nationwide regional bank run didn’t happen. As for large banks, deposits have fallen throughout the year, with most of the decline happening before Silicon Valley Bank and Signature Bank failed in mid-March. That seems to us like a combination of depositors’ chasing higher rates in money market funds, consumers’ dipping into savings as prices rose and businesses’ drawing down cash reserves.

Exhibit 1: Large Banks’ Deposits

Source: St. Louis Federal Reserve, as of 5/9/2023. Deposits, large domestically chartered commercial banks, 12/31/2022 – 4/26/2023.

Exhibit 2: Small Banks’ Deposits

Source: St. Louis Federal Reserve, as of 5/9/2023. Deposits, small domestically chartered commercial banks, 12/31/2022 – 4/26/2023.

SLOOS added some interesting color to this. Each quarter, the Fed includes some “special questions” that seek to drill down on recent developments or areas of concern. This survey had three such sets, with one focusing on the myriad reasons banks tightened credit standards. When asked if “increased concerns about deposit outflows at your bank” led to tightening standards, 57.1% of all banks said it wasn’t relevant to the decision, while 30.4% said it was somewhat important and 12.5% very important.[i] But under the hood, there was a split between large and small banks. Nearly two thirds of large banks—62.5%—said it wasn’t a factor, with 28.1% calling it somewhat important and 9.4% very important.[ii] But among smaller banks, exactly half said it was somewhat or very important. How can we interpret this? Well, to us, it is more evidence that the longer-running slide in large banks’ deposits isn’t some abnormal sea change. If it were, nearly two-thirds of them wouldn’t call it a non-issue. As for the smaller banks, while there was more concern, only 4 of the 24 who answered the question called deposit flight very important to credit conditions now. So even there, it seems like most of the industry has taken the drop in stride, and it hasn’t had an outsized impact.

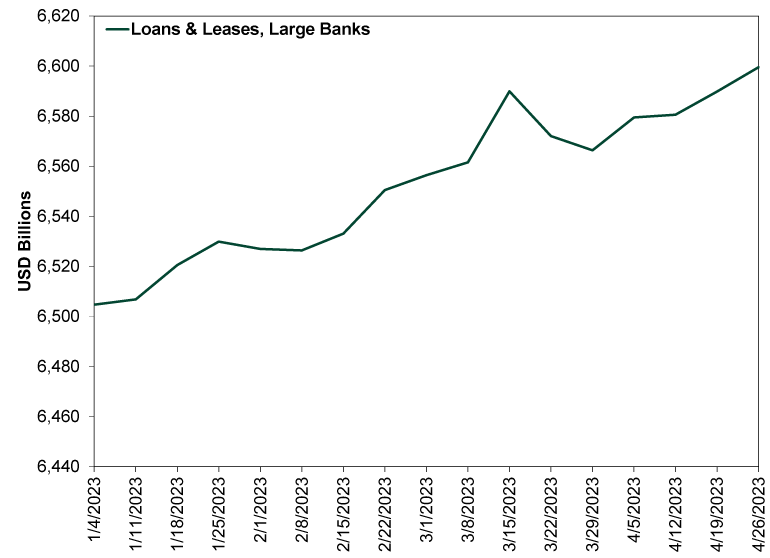

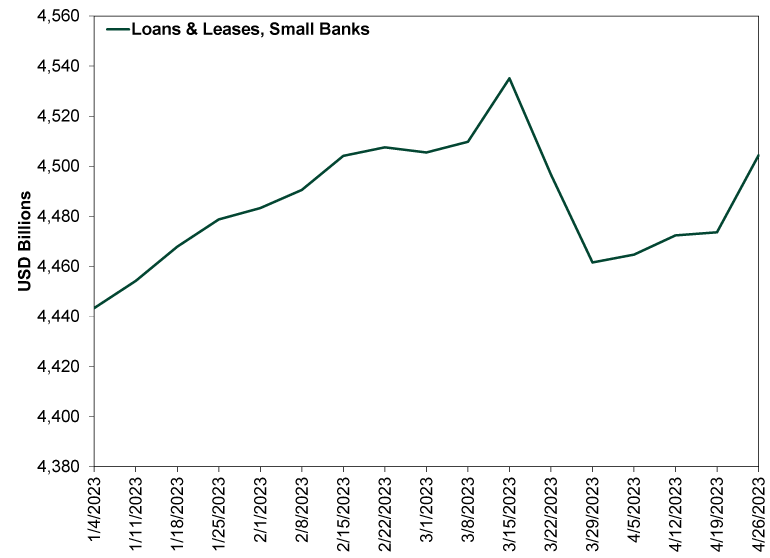

Lending data sort of prove all this out. Exhibits 3 and 4 show large and small banks’ weekly loans outstanding this year. Both took a hit in the March failures’ immediate aftermath. But large banks’ lending has since recovered to new highs, while small banks’ is about halfway back. The latter should look even better when you consider that much of the initial drop was tied to the accounting treatment of Signature Bank’s failure, which moved its loan portfolio to the FDIC’s books.

Exhibit 3: Large Banks’ Lending

Source: St. Louis Federal Reserve, as of 5/9/2023. Loans and leases in bank credit, large domestically chartered commercial banks, 12/31/2022 – 4/26/2023.

Exhibit 4: Small Banks’ Lending

Source: St. Louis Federal Reserve, as of 5/9/2023. Loans and leases in bank credit, small domestically chartered commercial banks, 12/31/2022 – 4/26/2023.

Tightening credit standards contributed to springtime lending weakness, but so did weaker demand. Among large banks, 51.5% cited moderately weaker demand for loans from large and mid-market firms, with 9.1% calling demand substantially weaker.[iii] Among small banks, those figures were 63.3% and 6.7%, respectively—suggesting businesses pulled back across the board amid the uncertainty and recent higher rates.[iv] Small businesses’ loan demand weakened similarly. Commercial real estate loan demand also dropped across the board. Over two-thirds of large banks and three-fourths of smaller banks reported weaker demand for construction and land development loans. About three-fourths of large and small banks said demand for non-farm nonresidential real estate loans—e.g., the much-maligned offices—was down. Demand for loans secured by multifamily properties fell most of all.

Yet across all categories, the net percentages of banks reporting tighter supply and weaker demand weren’t hugely changed from January’s survey. Credit standards were a smidge tighter and demand a mite lower, with many banks citing supply and demand factors (commercial real estate and rates) that have long been widely discussed. So here, too, it doesn’t look like March’s events threw a huge wrench in things. A sudden supply drop set against high rising demand would be concerning, but that didn’t happen. Instead we got a lending recovery in an overall slower credit environment.

So to us, it looks like reality is stacking up pretty well against expectations that everyone would retrench amid an alleged regional banking crisis. The weakness was short-lived, and the conditions contributing to it weren’t out of line with consensus expectations. Rather, banks and customers reacted about as anticipated, and they weren’t stuck in the doldrums long enough for lending to slide indefinitely. Instead, while—as yesterday’s article highlighted—banks are concerned that politicians’ reaction to the failures could create headwinds, they are more in the mode of watchful waiting. All seems consistent with how quickly stocks moved on.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Economics Q2 US GDP’s Stealthy Strength2026-07-31

-

Expert Commentary This Week in Review | Fed Meeting, US GDP, Eurozone GDP

2026-07-31

2026-07-31 -

Market Analysis Don’t Fret the EU’s Low Summertime Gas Storage Levels2026-07-31

-

Economics On Fires and GDP2026-07-30

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today