Personal Wealth Management / Market Analysis

What to Make of the Disbelief Towards July’s Jobs Numbers

The reaction to July’s jobs report suggests the pessimism of disbelief remains strong.

Amid the dog days of summer, we received some good economic news late last week: a strong July jobs report. A handful of observers cheered the month's figures, saying they suggested recession isn’t underway after all. However, most experts worried the unexpectedly robust numbers would motivate the Fed to keep hiking interest rates—increasing the risk of an economic hard landing. In our view, the largely dour reaction to overall positive, if backward-looking, data says more about the state of sentiment today than anything about the US economy going forward.

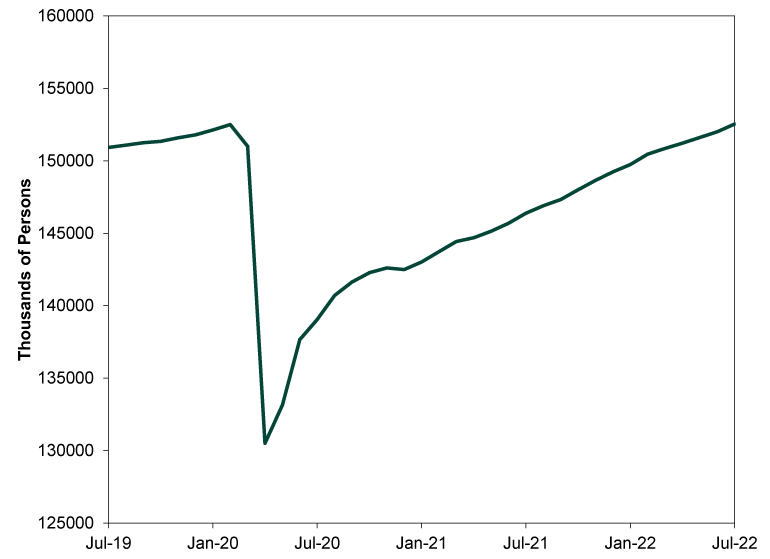

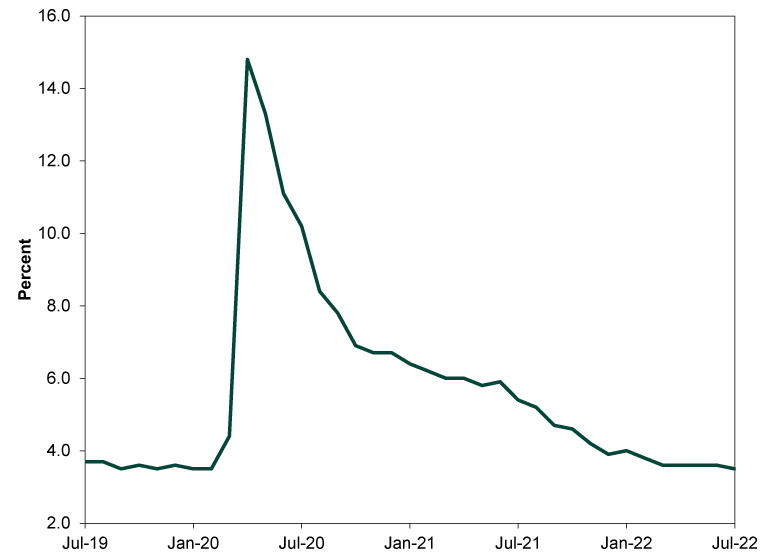

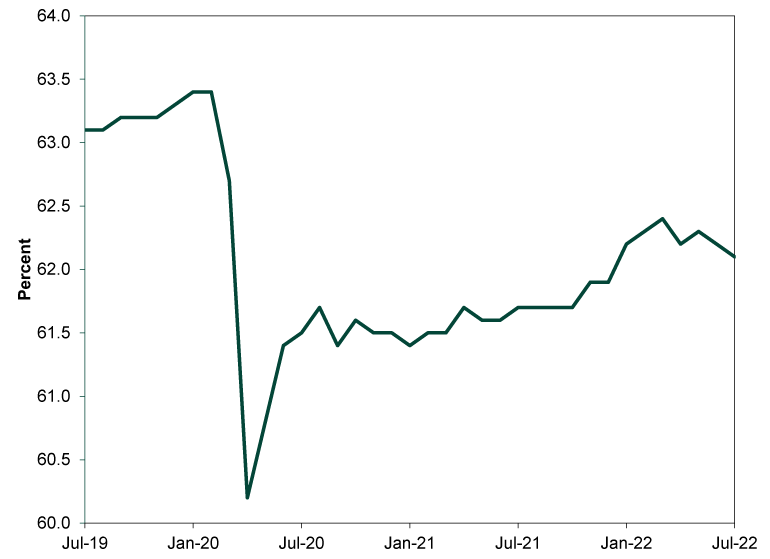

Widely watched jobs measures showcase the labor market’s recovery from the pandemic-driven downturn. July nonfarm payrolls rose by 528,000, better than expectations of 250,000, and bringing total payrolls to 152.54 million—a tick higher than February 2020’s pre-pandemic reading of 152.50 million. (Exhibit 1) The unemployment rate ticked down to 3.5% from June’s 3.6%, returning to February 2020’s level. (Exhibit 2) The one laggard is the labor force participation rate: It slipped to 62.1% from June’s 62.2% and has been drifting further away from February 2020’s 63.4% for months. (Exhibit 3)

Exhibit 1: Nonfarm Payrolls, July 2019 – July 2022

Source: FactSet, as of 8/8/2022.

Exhibit 2: Unemployment Rate, July 2019 – July 2022

Source: FactSet, as of 8/8/2022.

Exhibit 3: Labor Force Participation Rate, July 2019 – July 2022

Source: FactSet, as of 8/8/2022.

July’s numbers also extended a longer-running theme: the return to normal. On a sector basis, leisure and hospitality led with an added 96,000 jobs, highlighted by growth in food services and drinking places (+74,000)—in line with a development we touched on last month.

Overall, we see this jobs report as a late-lagging, backward-looking confirmation of the post-pandemic recovery. But most coverage focused on the labor market’s alleged forward-looking implications for the US economy. There was a small contingent of optimism, as some saw strong labor market numbers as a sign of businesses’ resiliency and willingness to hire despite recent Fed rate hikes—implying recession fears are overwrought. But the popular take was much gloomier, with most worrying a sizzling labor market would keep the Fed on its tightening path. The logic: If the Fed doesn’t cool the jobs market (via rate hikes that slow economic growth), inflation will remain hot. Yet if the central bank hikes too aggressively, Fed chair Jerome Powell and co. may send short rates above long rates, inverting the yield curve—historically a recession harbinger. Some attributed last Friday’s morning stock selloff—which reversed and turned into a flat finish by the end of the day—to this fear.

We also saw several examples of people looking for the cloud in a silver lining. Some argued that despite strong jobs growth, pandemic distortions continue preventing a true economic recovery. Others zeroed in on low labor force participation, arguing it makes companies believe they must hold on to workers even as times get tough, lest labor shortages make it impossible to hire later. Supposedly, this staves off the labor market weakness that might otherwise materialize after two sequential GDP contractions—making growthy jobs data something of a false positive. Still others worry a low labor force participation rate feeds inflation via faster wage growth, and while that is good news for workers now, it stores up future economic trouble.

In our view, most of these reactions overstate what jobs say about the economy’s prospects or central bankers’ future actions. As we have long written, labor data are lagging economic indicators, as hiring follows economic growth. Businesses usually add workers only when necessary—typically after firms maximize output with current headcount. As for the Fed, nobody knows how jobs data influence officials’ decision-making. Each voting member can interpret the same labor measures differently—not to mention consider other variables other voters don’t. Trying to predict Fed decisions based on speeches, interviews and other words is a mistake, in our view, since officials could always change their mind based on new information. Consider, too, they already broke their pledge to stop forward guidance, less than two weeks after making it.

However, the broad response to July jobs reveals a snapshot of the mood today. In our view, the reaction is another example of what Fisher Investments founder and Executive Chairman Ken Fisher calls “the pessimism of disbelief”—a common, late-downturn sentiment feature. When the pessimism of disbelief is prevalent, investors zero in on negatives and ignore good news—or view the latter as bad news in sheep’s clothing. Said another way, positivity receives a “yeah, but” objection. For a recent example, go back to the early days of the bull market that began in March 2020. The May 2020 jobs report, released in early June, showed nonfarm payrolls rising by 2.5 million jobs, trouncing expectations of an 8-million job decline. Yet, as we noted then, rather than herald the positive shock, many worried Congress and the Fed would prematurely end their economic “support,” torpedoing the recovery. We never thought policymakers’ efforts were actual stimulus, but it was telling so many pundits overlooked the simple benefit of lifting lockdowns and allowing businesses to reopen, which then led to growth (and jobs). Instead, they feared any positivity would be fleeting absent government action.

We see similar behavior today. In the latest iteration of the pessimism of disbelief, yeah, jobs are rising—especially in pandemic-ravaged services industries—but it is a Pyrrhic victory since strong labor data will lead to Fed rate hikes that drive recession. Jobs aren’t alone in receiving this negative interpretation, either. Headlines debated whether US GDP’s contraction spelled recession, and some experts found proof for their case in the mixed readings from the latest business surveys.

We agree not all is peachy. Some previously fast-growing industries are slowing as reopening-related booms fade, and other areas face ongoing headwinds. But the pessimism of disbelief’s prevalence is a strong sign stocks have already digested these obstacles and fears of worse to come. That suggests it shouldn’t take much for reality to deliver the sort of positive surprise that helps fuel a market recovery—whether that recovery is already underway or close by from here.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Politics Blunting Burnham?2026-07-21

-

Market Analysis Why the SOX “Bear Market” Isn’t Foreboding2026-07-21

-

Expert Commentary 3 Things You Need to Know This Week | Q2 Earnings, ECB Meeting, Trump Accounts

2026-07-20

2026-07-20 -

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—July 13 - July 172026-07-20

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today