Personal Wealth Management / Economics

Why We Don’t Fear Deflationary Doom Is Here

Fears of deflation doom seem like typical correction ghost stories.

Stocks had a wild ride Wednesday, with the S&P 500 Price Index down as much as -3% before climbing back to finish the day down just -0.8%. Perhaps the correction many have long awaited is here-at one point, the S&P 500 Price Index was about one percentage point removed from correction territory (10% lower than a prior high point)-but it's only clear in hindsight. Such moves are sentiment-driven and tend to come and go fast. There is usually a host of negative headlines, surrounding a spooky story or stories. But corrections can be caused by virtually anything. Or nothing. Such headlines abound today.

Let's consider one of the day's big fears: global deflation. To many observers, the evidence prices are about to spiral downward is stacking up. Chinese consumer inflation slowed to just 1.6% y/y in September-the lowest since 2009-and Chinese producer prices slid faster, hitting -1.8% y/y. September US producer prices fell -0.1% m/m. UK CPI slowed to 1.2% y/y, also the slowest since 2009. 10-year US Treasury yields briefly dipped below 2%. Oil prices continued tanking.[i] Market-driven future inflation gauges, including five-year US TIPS spreads and the eurozone's five-year/five-year inflation swap, are falling. German inflation is stuck at 0.8% y/y. The eurozone's final September inflation estimate hits Thursday, and no one expects improvement from the 0.3% y/y first read.

Two primary interpretations emerged from this data bonanza. One, the slow ebb in prices will be a self-fulfilling prophecy, and deflation will choke off the global expansion. Two, low inflation/deflation will make debt more burdensome-another growth headwind. These are big, popular, scary stories, but we don't think either carries much weight-problematic deflation doesn't appear to be in the cards.

If inflation is always and everywhere a monetary phenomenon of too much money chasing too few goods and services, then deflation is a monetary phenomenon of too little money chasing too many goods and services. When we have seen prolonged deflation in history, it is generally for one of two reasons: Central banks are sucking money out of the financial system, or efficiency gains and technology are making goods and resources cheaper and more abundant. The first is generally bad. The second is generally good-the US and UK experienced it for long stretches during the industrial revolution, a period of fantastic growth. There is nothing wrong with productivity and technology boosting the supply of goods and services way above money supply growth-it means more things are more affordable for more people, a vast overall improvement in quality of life.

For investors, the question today is whether we're at risk of yucky, broad-based deflation and shrinking money supply or whether certain goods are just getting cheaper because of technology or rising supply. Evidence strongly suggests door number two.

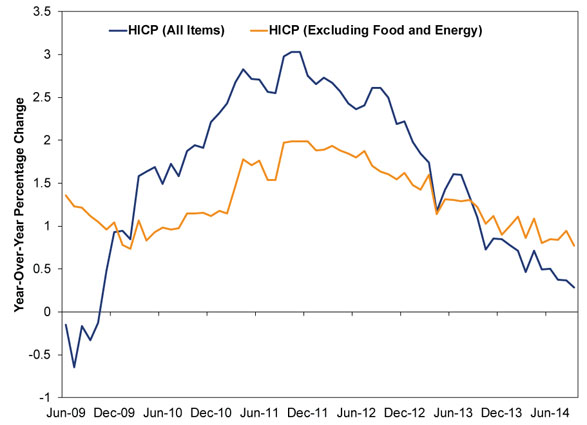

First, core inflation-which excludes volatile food and energy prices-hasn't slipped nearly to the degree headline inflation has in the UK and eurozone.

Exhibit 1: Eurozone Inflation

Source: FactSet, as of 10/15/2014. Eurozone Harmonized Index of Consumer Prices, All Items and All Items Excluding Energy and Unprocessed Food, June 2009 - September 2014.

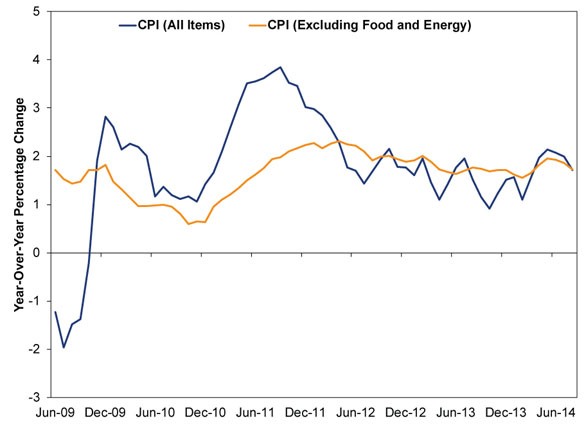

Exhibit 2: UK Inflation

Source: FactSet, as of 10/15/2014. UK Consumer Price Index, All Items and All Items Excluding Energy and Seasonal Food, June 2009 - September 2014.

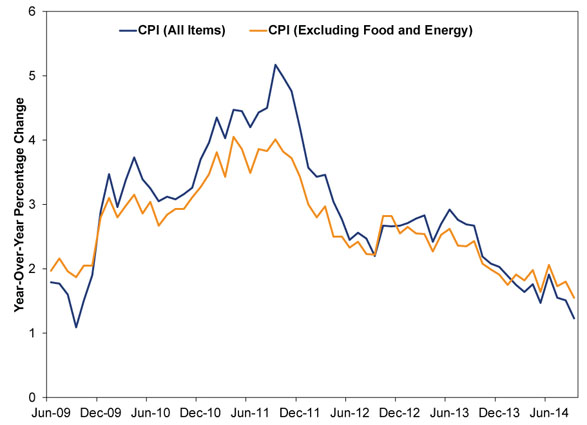

In the US, core and headline inflation are fairly steady.

Exhibit 3: US Inflation

Source: FactSet, as of 10/15/2014. US Consumer Price Index, All Items and All Items Excluding Energy and Food, June 2009 - August 2014.

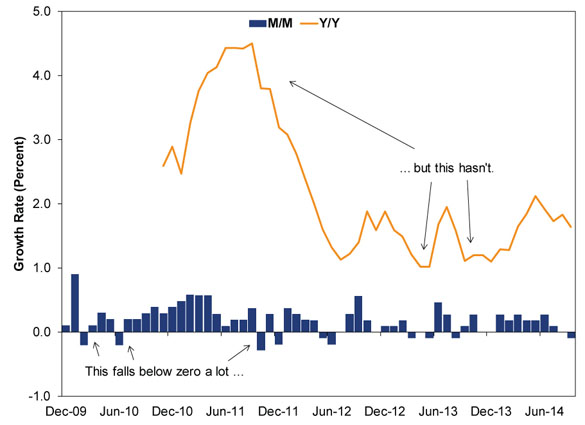

Folks worry US CPI will take a September tumble because PPI fell. However, there isn't much evidence of actual deflation in Wednesday's PPI report. Producer prices did fall -0.1% m/m, but they're up year-over-year. Plus, that monthly decline is largely tied to a -0.7% drop in the energy component of PPI. Core PPI was flat.

Besides, September is one month. In this series' short lifespan (it begins in November 2009), there have been plenty of negative blips-and no broad based deflation.

Exhibit 4: US PPI

Source: Federal Reserve Bank of St. Louis, as of 10/15/2014. Producer Price Index, Final Demand, m/m and y/y percentage change, December 2009 - September 2014.

Anyway, so far, it seems to us folks' fear falling energy prices-usually something people like. Energy prices are down largely because production is surging. US production jumped 5.1% between July 25 and October 3 (the closest these weekly data can come to approximating August and September), and OPEC didn't drop output to offset, breaking with tradition-Saudi Arabia decided maintaining market share mattered more than propping prices. (This might have something to do with that oil tanker carrying 400,000 barrels of crude that set sail from Houston to Korea in July.) Libya is also irregularly ramping back up. In other words, this is just more of the same-the shale boom showing up in various datapoints. The size of the move is likely sentiment simply overshooting reality.

What about core prices? We won't deny they're falling-the charts above make that plain as day. Some of it is down to falling commodity prices globally, as years of high mining investment created a supply glut-this would be the primary reason Chinese producer prices are falling. Moreover, falling inflation doesn't mean deflation lurks. Core eurozone inflation fell to roughly today's levels in early 2010, then turned up. Core US inflation fell to 0.63% y/y in December 2010, then bounced.

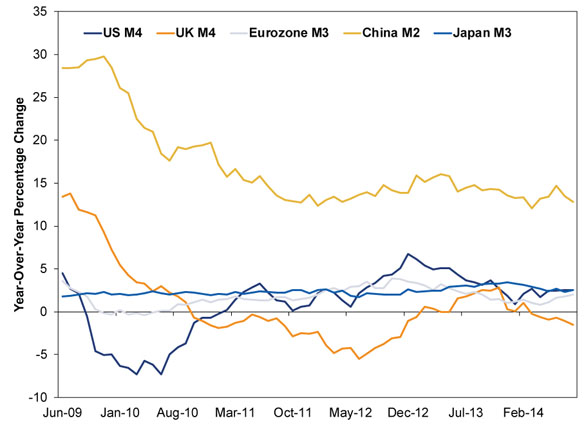

The key, as ever, is money supply. The broadest measures of money are rising in the US, eurozone and Japan. China's main gauge, M2, is consistently up double digits. UK money supply looks wobbly, but this is tied largely to some big one-off monthly drops in March and December-monthly data have ticked up since June. And anyway, falling money supply for long stretches in the UK and US didn't tip the world into deflation.

Exhibit 5: Money Supply Growth in Big Places

Source: FactSet and Center for Financial Stability, as of 10/15/2014.

The quantity of money isn't gangbusters by any stretch, but this isn't the 1930s when many central banks' rigid adherence to the gold standard sucked money out of the world. This is a modestly growing money supply, which is consistent with modest inflation-which is what we have in most of the world today. Contrary to media spin, those five-year market inflation expectation gauges in the US and eurozone square with this, too-both signal actual honest-to-goodness inflation over time. Granted, the expected rates are below central banks' targets, but those targets are arbitrary.

As for those big related fears-weak prices weakening the world economy and making debt scarier-neither really holds. Price changes are after-effects of money supply and economic growth, not drivers. Contrary to what you will read many places, deflation doesn't drive down consumer spending by encouraging folks to wait forever and a day for a better deal. That assumption goes against basic economics-as we all learned from supply and demand curves in high school, demand rises as prices fall. If central banks did suck money out of the economy, that would be bad, but that isn't deflation causing a recession. That is a fall in the quantity of money putting the world at risk-deflation is a side effect. Again, the quantity of money is rising today.

Moving on to fear number two, lower inflation does make debt repayment a tad more of a pain-higher inflation makes fixed payments (like a fixed mortgage) less expensive over time-but it is a stretch to say this would be a massive overhang on growth. It kind of goes without saying that low inflation means most other goods and services would be relatively less expensive than they otherwise would be if inflation were higher. This helps counterbalance the impact of low inflation on mortgage and other fixed debt repayments. Mortgage and other debt is just one variable in people's cost of living, and incomes matter, too. If wages and prices grow slowly while debt repayments are slowly devalued a bit and incomes gradually tick higher, that sort of seems like a Goldilocks economy, no? We aren't trying to say the world economy is in perfect shape, but this particular fear seems like an invented risk, not a real one.

Rollercoaster days-and pullbacks in general-will often have big scary stories like this. Sometimes those scary stories will have lots of data backing them. But anecdotal evidence doesn't make a thesis true. Markets might be too irrational to see this over extremely short periods like a day, week or even month, but over time, markets should see this and other similar fears for what they are: ghost stories, not signs of something deeply, fundamentally negative.

Stock Market Outlook

Like what you read? Interested in market analysis for your portfolio? Why not download our in-depth analysis of current investing conditions and our forecast for the period ahead. Our latest report looks at key stock market drivers including market, political, and economic factors.

[i] Pun intended.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Politics The Tenth Question Facing Alberta2026-08-06

-

Market Analysis Western Oil and Gas Producers Are Ramping Up2026-08-06

-

Corporate Information How You Benefit from Fisher Investments' Transparent Fee Structure

2026-08-04

2026-08-04 -

Corporate Information How Fisher Investments' High-Touch Service Helps You2026-08-04

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today