Personal Wealth Management / Market Analysis

A Big Surprise

Global stocks are up nicely in 2013, but the year could still have big returns ahead.

US and global stocks are up nicely in 2013 so far (up 16.4% and 12.7% respectivelyI), with many indexes hitting cyclical or all-time highs. Not too shabby when we’re not even halfway through the year yet! Yet, some posit we shouldn’t expect much over the rest of the year, perhaps because stocks have historically averaged about 10% over time. But history shows stocks normally don’t earn “average” returns in a given year—big returns are quite common, and in our view, big returns are likely in store for 2013.

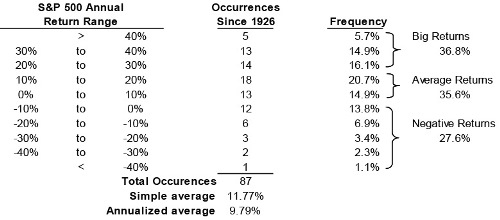

Exhibit 1 shows the ranges and frequency of S&P 500 annual returns. (We use US returns here instead of global for the longer data history—but the same holds for global returns.) First, note returns are positive much more than negative. Also, big positive returns are perfectly commonplace. US stocks have been up in excess of 20% in 36.8% of all years. Seen another way, of all positive years (63 since 1926), over half had big, 20%+ returns.

It may not feel that way, since the S&P 500 broke 20% just once in the past decade. But that’s the exception rather than the rule. From 1995-1999, for example, the S&P 500 returned 37.6%, 23%, 33.4%, 28.6% and 21% in consecutive years! That doesn't mean the next five years do the same thing, but it does speak to the probability of a gangbusters 2013 (which, like 1995, is the fifth year of a bull market).

Exhibit 1: S&P 500 Annual Return Range Since 1926

Source: Data through 12/31/2012. Global Financial Data, Inc; as of 1/17/2013.

Markets don’t move smoothly and gradually on predictable slopes—they’re volatile (corrections are always possible), can fluctuate wildly and don’t fit any kind of neat, measured pattern. If they did, stock returns would likely be lower. Moreover, while bull markets die for many reasons, neither age nor magnitude is among them, and there’s no reason this bull has to peter out in its fifth year.

In fact, there’s every reason for it to carry on. Earnings growth has outpaced stocks since the bull began, suggesting equities remain undervalued—and earnings are expected to keep rising, with less economically sensitive sectors leading the charge (bullish for mega-cap stocks). Corporate America’s gotten even stronger in recent months, with balance sheets healthy and flush with cash, business investment rising and stock buybacks accelerating. Another bullish feature—investor sentiment is only now shifting from skepticism to optimism. The more investors become optimistic, the more apt they are to bid stocks’ prices up—and they can do so for some time before the bull reaches its typically euphoric peak. Add to that fine yet still underappreciated global growth and tame inflation, and there’s plenty of room for reality to exceed still-muted expectations—and for this bull to march ahead.

I US stocks refers to the S&P 500 Total Return index. Global stocks refers to the MSCI World Total Return, net of dividends, index. Data is as of 1/1/2013 through 5/24/2013.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets — July 27 - July 312026-08-03

-

Market Analysis Digging Into Last Week’s Fed ‘Credibility’ Concerns2026-08-03

-

Expert Commentary 3 Things You Need to Know This Week | US Jobs, Trade Balance, Earnings Reports

2026-08-03

2026-08-03 -

Expert Commentary This Week in Review | Fed Meeting, US GDP, Eurozone GDP

2026-07-31

2026-07-31

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today