Personal Wealth Management / Market Analysis

A Maturing Bull Market Likely Favors Big Growth

The bull market looks likely to continue, but with changed leadership.

In Fisher Investments’ view, 2012 likely features the continuation of the bull market, now in its fourth year. We anticipate full-year returns will be robust; however, we believe we’re also in the early stages of a leadership change wherein big growth takes primacy over small value.

Early stages of bull markets tend to be led by small cap value stocks, which in a capitalization-weighted index means a larger percentage of stocks outperform the broad market. The portion of stocks outperforming the overall market is known as market breadth. Lower valuation, capital intensive firms also tend to lead in the initial, V-shaped surge characteristic of early bull markets—hence small cap value’s tendency to lead early on. However, as the bull market matures, investors focus on a decreasing number of “high quality” big cap growth stocks. This is manifested in two primary ways—falling market breadth and the tendency for big cap growth stocks to outperform small cap value.

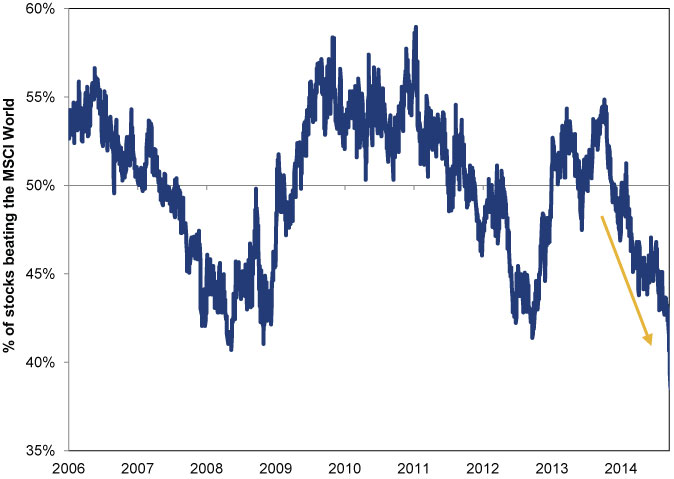

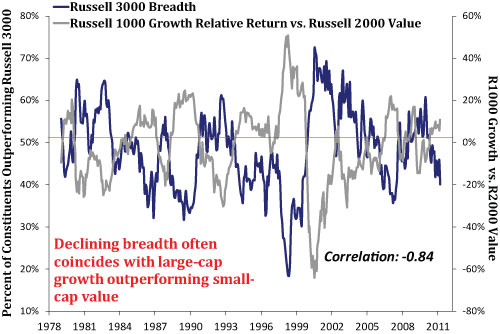

Exhibit 1 shows in bull market early stages, about 60% of Russell 3000 constituent stocks outperformed the index on average. However, as bull markets mature, this share fairly consistently falls. And as breadth narrows, big cap growth stocks tend to outperform small value—as shown in Exhibit 2.

Exhibit 1: Market Breadth Narrows as Bull Market Matures

Source: Thomson Reuters. Russell 3000 Index trailing twelve month price returns.

Exhibit 2: Big Growth Outperforms as Breadth Narrows

Source: Thomson Reuters. Russell 3000, Russell 2000 Value and Russell 1000 Growth Index trailing twelve month price returns.

In Fisher Investments’ view, the compositions of the small value and big growth categories fundamentally underpins this shift. Small value companies tend to be concentrated in mature, commoditized industries leveraged to the most cyclical segments of the economy. These firms may also be highly capital intensive, leading to heavy dependence on debt financing. As such, a steepening yield curve (strong incentive for banks to extend financing) and pent-up capex tend to form an ideal backdrop for small value outperformance. And those two features tend to be classic characteristics of early expansions.

In contrast, big growth sectors are generally less cyclical and less capital intensive—growth is often driven by innovation, new product development and rising market penetration (as the markets aren’t as mature). And they are typically less reliant on debt financing. Hence, as the yield curve flattens, that tends to favor small cap value less and big cap growth more.

The full rotation from small value to big growth leadership generally doesn’t happen overnight, and the effect historically has lasted a long time. What’s more, as bull markets end, breadth typically falls to less than a third of Russell 3000 stocks, and big cap outperformance is usually fairly material (see Exhibit 3). That these conditions haven’t materialized yet also suggests to us the current bull market has plenty of life left.

Exhibit 3: Big Growth Usually Outperforms Small Value Widely Before the Bull Ends

Source: Thomson Reuters. Russell 2000 Value and Russell 1000 Growth Index trailing twelve month price returns.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Corporate Information How You Benefit from Fisher Investments' Transparent Fee Structure

2026-08-04

2026-08-04 -

Corporate Information How Fisher Investments' High-Touch Service Helps You2026-08-04

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets — July 27 - July 312026-08-03

-

Expert Commentary 3 Things You Need to Know This Week | US Jobs, Trade Balance, Earnings Reports

2026-08-03

2026-08-03

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today