Personal Wealth Management / Market Analysis

A Primer on Argentina and Turkey’s Currency Woes

A deep dive into these countries’ troubles shows why they don’t represent broader Emerging Markets.

Currency volatility in Emerging Markets is hogging headlines once again, as investors fear troubles in Turkey and Frontier Market Argentina will spill over, threatening the world with a 21st century version of 1998’s Asian currency crisis. However, a closer look at each country’s predicament shows their troubles are unique, stemming from long-running issues and questions over their central banks’ independence, among other issues. Most other Emerging Markets are in much better shape, limiting the risk of contagion.

Argentina: A Reformist Government Resurrects Old Ghosts

Understanding Argentina’s troubles requires a bit of history. For most of the 21st century thus far, the country was locked out of international capital markets after a sovereign default. Until 2016, Peronists led the government—Néstor Kirchner was president from 2003 – 2007, and his wife, Cristina Fernández de Kirchner, succeeded him. Under their watch, Argentina sank from a bustling, prosperous Emerging Market to an international basket case, beset by rampant inflation and heavy state intervention (e.g., nationalizing oil production and adopting price controls). MSCI downgraded it to Frontier status in 2009, and its economic problems escalated over the next seven years. Disillusioned with Peronism, voters elected Mauricio Macri, the center-right former mayor of Buenos Aires, to replace her in 2016. He spent his first year in office executing difficult but necessary economic reforms and solved the country’s long-running debt standoff, returning the country to international capital markets. Investors largely hailed his progress.

Yet inflation remained persistent, as is typical in the aftermath of price controls. In December, the central bank raised its inflation target from a range of 8% – 12% to 15%. Yet in January, despite accelerating inflation, it cut interest rates. Both measures brought the central bank’s independence into question, raising fears that Macri would turn on the monetary spigots to boost economic growth and his re-election prospects, just as Kirchner did.

As inflation expectations began to increase (estimates are for roughly 25% inflation this year, similar to last year, but well above official targets), its currency, the peso, began to suffer sharp declines. In response, the government intervened in the currency market, spending an estimated $6 billion of its forex reserves to support the peso by May 10. The central bank also raised interest rates from 27.25% to 40.0% in three moves since April 27 and lowered the cap on banks’ net open positions of foreign currency from 30% to 10%, forcing banks to sell an estimated $1.5 billion of foreign currency and move it back into the peso. Additionally, the government cut its targeted budget deficit this year from 3.2% to 2.7% of GDP. Finally, when all of that hadn’t fully stopped the problem, the government reached out to the IMF for a bailout loan of $30 billion. Talks to finalize the loan remain underway, spurring street protests from Argentinians who blame the organization for the fallout from 2001’s financial crisis.

With the currency run came the risk of bad loans. There has been a rapid increase in US dollar denominated-debt across the economy in recent years, with the percent of total Argentine credit in foreign currencies rising from 4.3% at the end of 2015 to 16.6% at the end of 2017.[i] When the peso plunges, foreign currency-denominated debt becomes much more difficult to service, raising the risk of defaults.

A successful government bond sale in mid-May helped shore up investor sentiment toward Argentina somewhat. The government successfully rolled over $27 billion worth of peso-denominated securities and auctioned $200 million in new debt, with interest rates ranging from 36% – 38%. The peso also appears to have stabilized, though it remains down about 25% versus the dollar. Meanwhile, the annual inflation rate hit 26% in April and inflation expectations continue rising, spurring the central bank to keep its key interest rate at 40% at this week’s meeting. From here, the outcome likely depends on the terms of any IMF deal and how much political capital Macri will have in its aftermath.

Hat tip to Austin Fraser for additional reporting and analysis.

Turkey: Escalating Authoritarianism Takes a Toll

While Turkey’s latest decline was rather sudden, years of economic mismanagement laid the groundwork for today’s problems. Turkish politics have long been dicey, and they have been increasingly problematic since 2016’s failed coup. In its aftermath, President Recep Tayyip Erdogan cracked down on dissent and consolidated power, prompting mass arrests, job dismissals and confiscation of roughly 800 businesses worth over $10 billion.

While Erdogan has apparently long desired autocracy, he has also had to operate within the bounds of Turkey’s constitution. After serving as prime minister from 2003 – 2014, he ran for and won the presidency—until then, a largely ceremonial position. To transfer power to the presidency and remain in power beyond previous term limits, he held a referendum in 2017. And in order to win, he had to be popular—so to offset the negative impact of his 2016 crackdown and boost his standing, he launched massive monetary and fiscal stimulus. Measures included interest rate cuts, lowering bank reserve requirements, removing a cap on consumer loans (instituted in 2015 to limit growth in the current account deficit) and increasing deficit spending. Additionally, he forced banks to reduce mortgage rates by threatening non-compliant banks with treason charges and setting up a tip line for customers to report them.

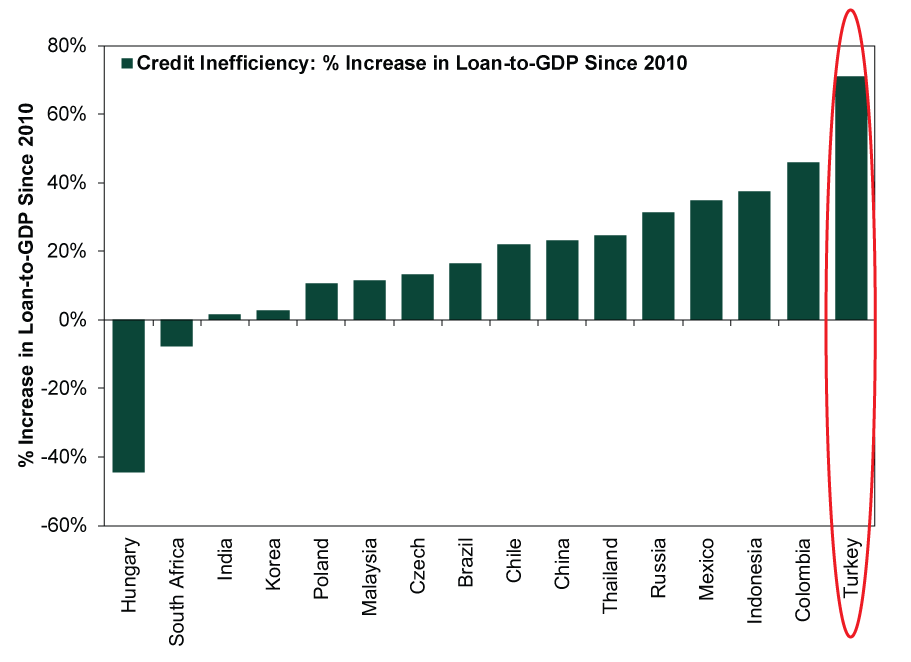

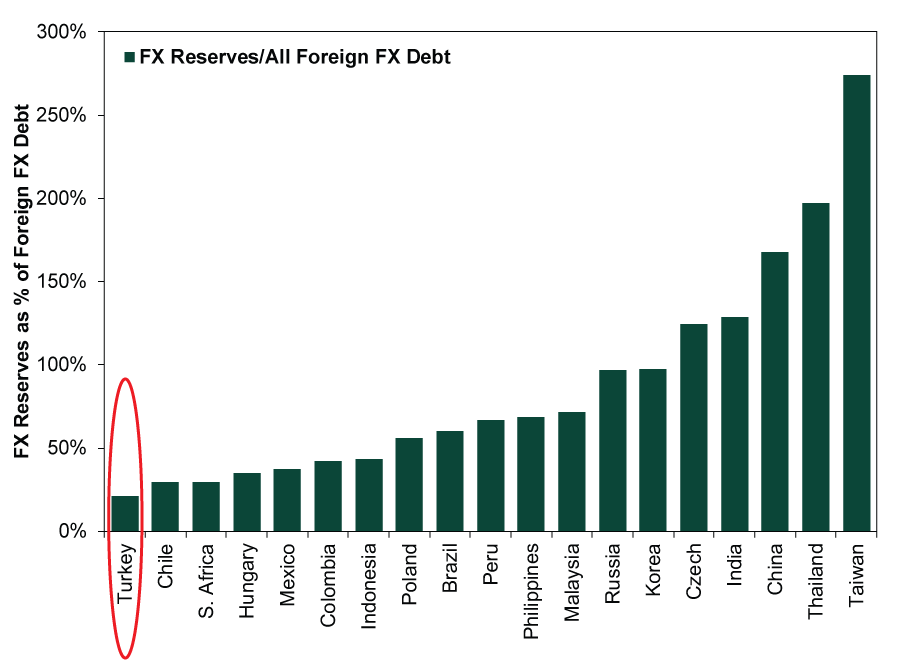

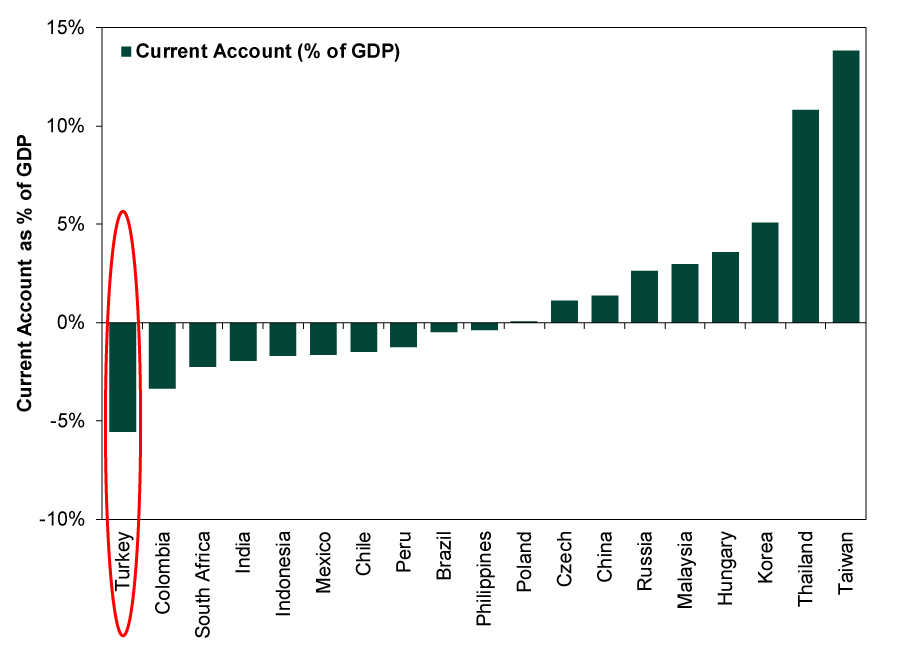

While these actions stimulated the economy and sealed Erdogan’s referendum victory, they also resulted in rising inflation, an expanding current account deficit and increasing levels of total debt and foreign currency denominated debt. Turkey now easily has the highest increase in loans relative to GDP since the start of 2010 (representing less-efficient loan growth), the lowest FX reserves as a percent of foreign currency denominated debt and the largest current account deficit as a percentage of GDP of any major country in the MSCI Emerging Markets Index.

Exhibit 1: Turkey’s Credit Growth Has Been the Least Efficient Among Major EMs

Source: Bank for International Settlements, as of 5/25/2018. Data excludes Peru, Philippines, and Taiwan, which are broadly considered major Emerging Markets, due to lack of reporting by Bank for International Settlements.

Exhibit 2: Turkey’s Forex Reserves Are the Lowest Relative to Foreign Currency Debt Among Major EMs

Source: Bank for International Settlements, as of 5/23/2018.

Exhibit 3: Turkey’s Current Account Deficit as % of GDP is the Worst Among Major EMs

Source: IMF, as of 5/25/2018. Current Accounts as Percentages of GDP on 12/31/2017.

The stimulus was unsustainable. But in an attempt to continue to capitalize on it and increase his majority in parliament, Erdogan called for a snap election in June, well ahead of the scheduled vote in November 2019. Following June’s vote, thanks to last year’s referendum, Turkey will have an executive presidency. With the country still under a state of emergency, the government has bypassed parliament in passing new laws. If Erdogan wins in June, he will be able to consolidate power even further.

However, before the election could occur, sentiment began to sour on Turkish stocks as its currency, the lira, slid. Rather than raise interest rates or attempt to stabilize the currency, Erdogan vocally opposed higher rates. Despite having no official direct power over the central bank, he publicly declared he would assume responsibility for the central bank’s decisions, claiming he would be credited or blamed for the outcome regardless. This caused sentiment to deteriorate further, escalating the lira’s decline. As the situation spiraled downward, the central bank recently raised its key interest rate by 3.0% to try to stabilize the situation, but the currency continued declining.

Meanwhile, in a case of bizarre timing, Erdogan officially kicked off his election campaign on Thursday, reciting poetry and delivering a speech pledging splashy public investments, a Turkish space agency, free and open markets and single-digit inflation as deputies told reporters the country’s currency woes were the result of a “financial attack” by agents determined to expel Erdogan from Turkish politics. Only time will tell if local voters have the same opinion of an authoritative Erdogan as markets appear to.

Hat tip to Christo Barker for additional reporting and analysis.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis The New Tariffs in Town Are Still Old News2026-07-24

-

Expert Commentary This Week in Review | Market Volatility, Tariffs, SpaceX

2026-07-24

2026-07-24 -

Economics A Summertime Check-in on US Consumers2026-07-23

-

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today