Personal Wealth Management / Economics

A UK Perspective on QE

Since the UK stopped asset purchases late last year, it has shown signs of a strengthening economy. In our view, tapering QE in the US likely brings similar results.

Fed head Ben Bernanke made another attempt to soothe quantitative easing (QE) tapering jitters Wednesday, this time testifying about tapering plans in a House Financial Services Committee hearing. Headlines seemed relieved to hear tapering will depend on economic and financial developments and is not on a “preset course.” Never mind that Bernanke said nothing new—the Fed has sent this same message for some time. Moreover, while many still fret economic malaise once the Fed pulls the supposed punchbowl of endless liquidity, recent evidence from the UK suggests QE tapering shouldn’t be disastrous. In fact, the economy could very well accelerate.

This is what is happening across the pond. While some say QE ended earlier this month when new Bank of England (BoE) chief Mark Carney and all of his deputies voted against it (driving ye olde British QE jitters on Wednesday), it actually ended in 2012 when the Bank of England BoE finished its last round of asset purchases.

So the UK has gone all of 2013 without fresh QE—not just a taper, but a full stop. But similar to the Fed’s stated plans, it hasn’t started selling assets—and likely won’t for a while, according to some BoE committee members. The balance sheet has shrunk a little as some assets have matured—again, similar to what the Fed has telegraphed. (Exhibit 1)

Exhibit 1: Total BoE Assets

Source: Bank of England, as of 7/17/2013.

But likely to many folks’ surprise, a modest, gradual balance sheet decrease has not caused the economy to crater. In fact, the UK has shown several signs of fundamental economic improvement since QE ended.

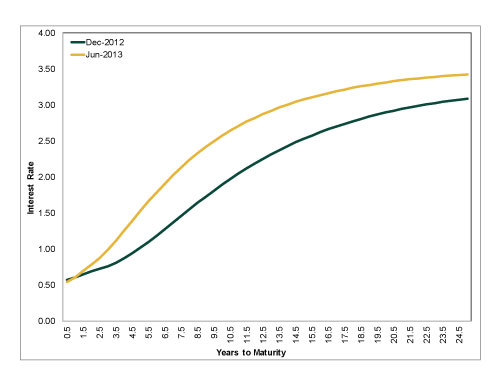

Most notably, the yield curve is beginning to steepen—an economic tailwind—now that the BoE’s no longer pulling down long rates through asset purchases. (Exhibit 2)

Exhibit 2: Government Liability Spot Curve

Source: Bank of England, as of 7/17/2013.

Several economic readings have shown notable acceleration, too—data that moved in fits and starts while QE was in full swing. PMI surveys were choppy at best while the BoE was purchasing assets. Manufacturing and Construction contracted regularly and Services struggled to gain momentum. But all have increased steadily since February and are now in positive territory. Retail sales increased from +3.3% y/y in May 2012 to +9.7% y/y by May 2013—and accelerated from 0.6% q/q in Q1 to 0.9% q/q in Q2. Trade has also picked up some, with exports and imports both trending higher this year. Business investment had its first positive quarter in a year in Q1, increasing by £21.1 billion q/q. These positive trends may not be because of QE’s end, but they are strong evidence the economy can accelerate without a steadily increasing central bank balance sheet.

Sure, the US isn’t the UK. But we’d argue the US, with seemingly stronger economic fundamentals, may be positioned even better for post-QE growth. Corporate earnings are at all-time highs, firm balance sheets are flush with cash, manufacturing output is improving from recent volatility, retail sales are up and housing is making a strong comeback—even with the QE-induced flatter yield curve. Should these conditions remain, we’d suggest the prospects for growth—possibly even improved growth—are good once the taper takes place.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets — July 27 - July 312026-08-03

-

Market Analysis Digging Into Last Week’s Fed ‘Credibility’ Concerns2026-08-03

-

Expert Commentary 3 Things You Need to Know This Week | US Jobs, Trade Balance, Earnings Reports

2026-08-03

2026-08-03 -

Expert Commentary This Week in Review | Fed Meeting, US GDP, Eurozone GDP

2026-07-31

2026-07-31

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today