Personal Wealth Management / Market Analysis

About China …

Domestic Chinese stocks' wild ride should hold little risk for global investors..

China's Shanghai and Shenzhen stock exchanges have taken a wild ride over the last year-first with a spectacular rise, then, since June, with a crash that has some raising comparisons with the US in 1929. Chinese officials have tried several times to stop the bleeding to no avail, and now there are rumors and worries of global contagion. We could indeed see volatility as fear spikes, but China's domestic markets have a few quirks that render true contagion unlikely.

China has two major stock classifications: A-shares (mainland stocks traded on the local exchanges) and H-shares (mainland stocks traded on Hong Kong exchanges). Because China has strict capital controls, H-shares comprise most of the universe accessible to non-Chinese investors. A-shares are available mostly to Chinese investors, with international participation limited to three trial programs with strict limits. The programs for institutional investors are capped at a combined $138 billion, or 5.8% of the investible A-share market capitalization.[i] The program for individual investors has a $2.1 billion daily limit-equal to roughly 0.07% of the A-share market capitalization-and covers only about 200 of the Shanghai exchange's roughly 1,700 stocks.[ii] This very limited foreign access is why MSCI declined to add A-shares to its mainstream Emerging Markets benchmark last month.

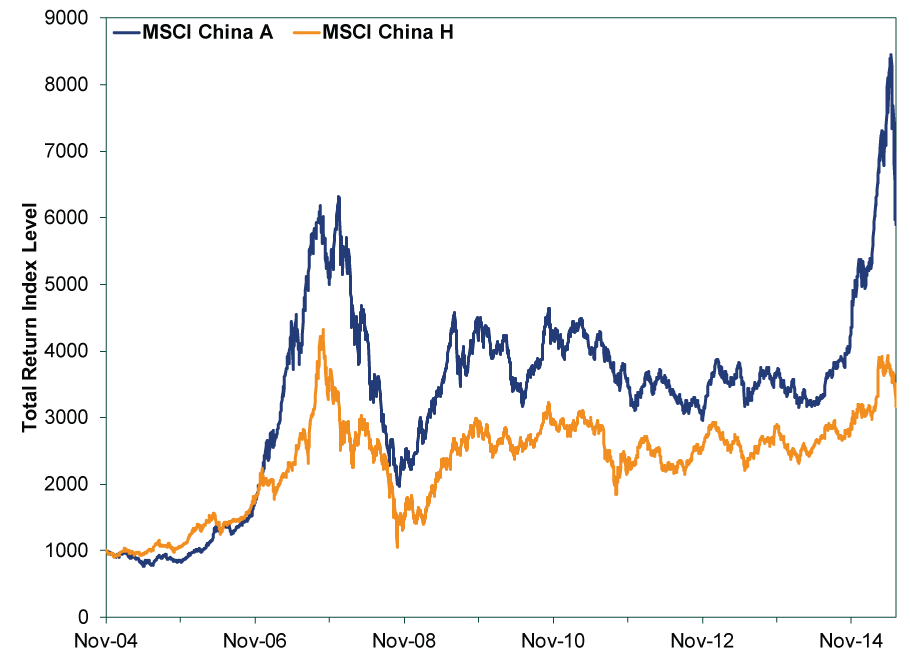

The wild ride is largely concentrated in A-shares. H-shares have moved, but not to nearly the same degree-up or down. This continues a long-running trend. Since MSCI launched its A-share and H-share indexes in late 2004, A-shares have been far more volatile.

Exhibit 1: A-Shares Vs. H-Shares

Source: FactSet, as of 7/8/2015. MSCI China A and MSCI China H index returns with net dividends, 11/30/2004 - 7/7/2015.

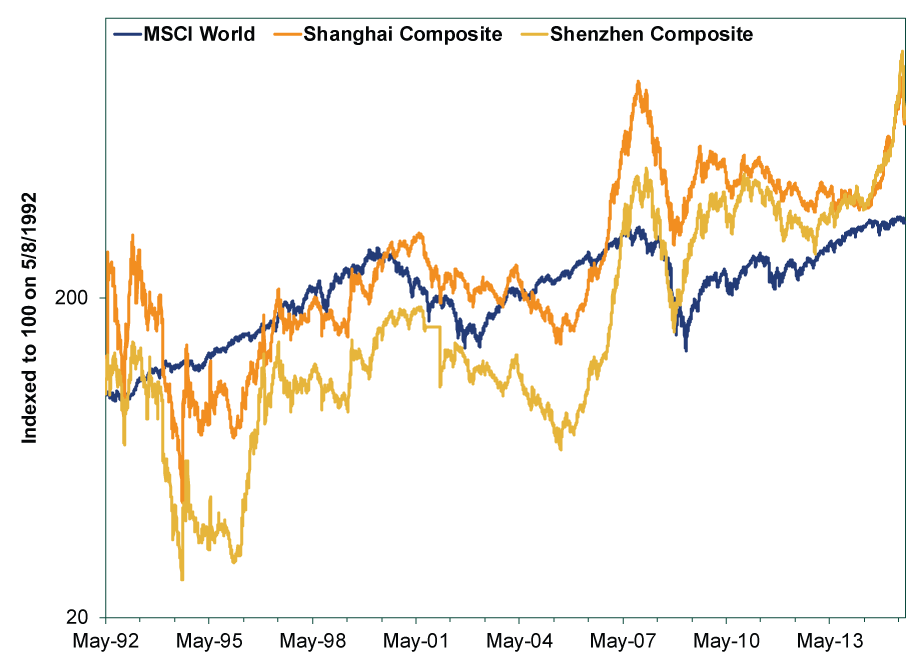

A-shares have next to no relationship with global stocks. Exhibit 2 shows the Shanghai and Shenzhen Composite indexes, which have a longer history than MSCI's benchmark, along with the MSCI World Index since 1992. We used a logarithmic scale, which shows percentage-based movements and reflects mainland shares' wildness better than a linear scale would. While China's economy certainly has a major global impact, its equity markets are isolated. From a stock market perspective, what happens in China stays in China.

Exhibit 2: Mainland and World Stocks

Source: FactSet, as of 7/8/2015. Shanghai Composite, Shenzhen Composite and MSCI World Index price returns, 5/8/1992 - 7/7/2015.

The numbers since A-shares' mania began are striking. From 4/30/2014 through their 6/12/2015 peak, A-shares rose 163.2%.[iii] Since then, they've fallen -30.2%.[iv] By contrast, H-shares rose 52%, then fell -14.9%.[v] Big moves when considered in a vacuum, but far tamer than A-shares.

A-shares' wild ride over the past 14 months seems like a classic mania, but the firewall around mainland stocks should prevent spillover-much as it prevented the steep rise from spilling over. Historically, Chinese investors have preferred to park their savings in real estate, not stocks. Real estate has relatively decent property rights-a big attraction. A-shares were less attractive because most are state-run companies, with ownership heavily concentrated among Communist Party elites and the state itself. Most saw Chinese stocks as a market controlled by a privileged few, subject to manipulation, much like US stocks in the Gilded Age. Throw in weak corporate governance, corruption and a tendency to cook the books, and local investors mostly thumbed their noses.

But then Chinese property markets took a beating, leaving folks wanting an alternative. Simultaneously, China's government was desperate to diversify away from banks as the primary source of corporate funding, and encouraging equity participation seemed like a good way to do it-if newly moneyed locals would buy new listings, then companies could get funding via capital markets, not funds channeled through state-run banks, freeing them up more to help address the local government debt problem. Seemed like a winner! So Chinese state-run media started publishing articles touting stocks' benefits, talking them up left and right and encouraging the locals to pile in. They did, often on margin, and mainland stocks soared.

It had all the trappings of a mania. New investors with no market knowledge snapping up penny stocks, believing low prices meant automatic gains. Newly IPO-ed stocks rising by the daily limit for weeks on end. Folks margined to the hilt trading on momentum, ignoring surging valuations that sometimes hit triple digits. Increasingly irrational editorials in state-run media trying to explain away the market's surge and encouraging folks to buy in. In January and May, the central bank tightened margin curbs, triggering big one-day drops, but the frenzy near-immediately resumed. Sentiment was clearly out of line with fundamentals, and realignment was a matter of when, not if. It looks like that realignment is happening now, though no one can know how long it will last.

Capital controls and China's strictly controlled media explain why A-shares rollercoaster is a pure domestic phenomenon. H-shares are largely off-limits to mainland investors, so their irrational exuberance couldn't spill over there. Because the government blocks many foreign news sites, most mainland investors also couldn't read the many, many articles warning of a bubble and impending crash in A-shares, so there was nothing to counterbalance the state-run media's unwarranted cheer. Non-Chinese investors, by contrast, saw all the warnings, and it wasn't hard to figure out Chinese state-run media had ulterior motives to promote stocks. Sentiment in H-share markets was therefore far more tame. They had more information and a more diverse perspective to discount. Not to mention all that lingering skepticism over a hard landing in China's economy. As a result, the balance between sentiment and fundamentals in H-share markets is far more favorable.

Thanks to China's capital controls, the only way this could ripple globally is if it triggered an economic hard landing-China is big enough that severe economic troubles there could hurt the world. However, this seems unlikely. While stocks in developed-world markets are a good leading economic indicator, A-shares really aren't. The current drop is the third exceeding -20% since 2009. China's economy never stopped growing-actually accelerating during the first-and the modest slowdown since 2012 is a largely government-engineered phenomenon. Some have speculated about a "wealth effect," where falling stock prices could dent consumption because folks "feel" less rich, but the wealth effect is as mythical in China as it is in the rest of the world.[vi] Disposable income is the primary driver of consumption, and officials continue doing what's needed to ensure enough growth to keep boosting incomes. Plus, consumer spending is roughly one-third of China's economy-quite small. For all the comparisons between China today and the US in 1929, the crash of '29 didn't cause the huge economic contraction that ran through 1933.[vii]

There are legitimate questions over what the rout means for Chinese policy, but we don't see much reason to fret a sea change at the moment. Since he took over in 2012, President Xi Jinping has taken several steps to move China to a more market-oriented economy, and many fear the government's stock market interventions represent a big U-turn-measures include removing mandatory margin requirements (leaving margin call thresholds to brokerages' discretion), increasing margin financing support (with the central bank agreeing to inject liquidity directly), establishing a "market stabilization fund" to buy stocks, and getting 21 securities firms to agree not to sell stocks from their books while the Shanghai Composite trades below 4,500. Wednesday, securities regulators banned "major shareholders, corporate executives and directors" from selling stakes exceeding 5% of outstanding shares for six months.

China's seemingly haphazard approach announcing new measures daily adds to uncertainty and fear. That, coupled with the fact the bleeding hasn't stopped, has undermined confidence in officials to manage the markets and economy-hence those contagion fears. But Chinese officials have always been figuring things out as they go along, and prior attempts to allow market forces to play a greater role haven't always gone as planned either. On a few different occasions last year, they tried to allow state-owned and private firms to default on corporate bonds so investors could stop assuming an implicit government guarantee, allowing markets to better price risk. But each time, they eventually caved, arranging for investors to be made whole. There has always been a tradeoff between reform and ensuring stability-it is just more high-profile today.

If Chinese officials do slow down reform plans, it shouldn't be a global negative-it is more the absence of a long-term positive. World stocks have done fine with China playing less of a role in global markets, and they can keep doing fine if China isn't much of a global market force. The status quo, politically and economically, is just fine for global investors. Even at its slower growth rate, China contributes heavily to global trade, demand and growth. A-shares' wild ride shouldn't change that today-just as domestic bear markets didn't kill growth in 2009 - 2010 and 2011 - 2012.

[i] FactSet, as of 7/8/2015. MSCI China A Investible Market Index market capitalization in USD on 7/8/2015.

[ii] Ibid.

[iii] FactSet, as of 7/8/2015. MSCI China A Index returns with net dividends, 4/30/2015 - 6/12/2015.

[iv] Ibid. MSCI China A Index returns with net dividends, 6/12/2015 - 7/7/2015.

[v] Ibid. MSCI China H Index returns with net dividends, 4/30/2015 - 6/12/2015 and 6/12/2015 - 7/7/2015.

[vi] We'd also note that even with the crash, Chinese investors remain better off than they were a year ago.

[vii] We don't have the space to go into it all here, of course, but the Fed's failure to act as lender of last resort and its decision to allow money supply to contract bear much of the blame, along with the Smoot-Hawley tariff and the wave of protectionism that followed globally. We encourage you to read Milton Friedman and Anna Jacobson Shwartz's The Great Contraction and Amity Shlaes' The Forgotten Man for the full story.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis The New Tariffs in Town Are Still Old News2026-07-24

-

Expert Commentary This Week in Review | Market Volatility, Tariffs, SpaceX

2026-07-24

2026-07-24 -

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23 -

Economics A Summertime Check-in on US Consumers2026-07-23

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today