Personal Wealth Management / Market Analysis

All Aboard the Through Train?

China's long-awaited "through train" finally leaves the station Monday, giving foreign investors broader access to mainland stocks. Here are some things you should keep in mind if you're deciding whether to climb aboard.

Starting Monday, foreign investors will have unprecedented access to mainland Chinese stocks courtesy of the delightfully named "through train" program, which lets foreigners buy "selected" Chinese A-shares traded on the Shanghai exchange through Hong Kong brokerages. Many are cheery about the prospect of new demand worth tens of billions of dollars pushing Chinese stocks higher. But before you choo-choo your way over, we'd encourage you to keep a rational perspective. China has plenty going for it, but anyone expecting the through train to be the ticket to sky-high returns might end up a tad disappointed.

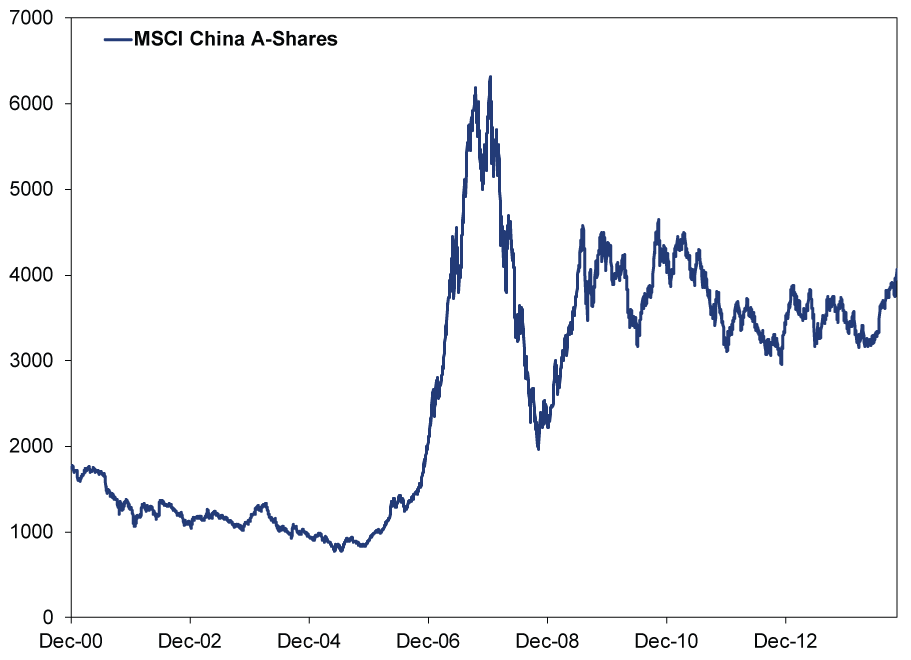

In recent years, Chinese A-shares haven't quite reflected the economy's rapid growth rate. They boomed at times during the 2000s bull market, but as Exhibit 1 shows, this was short-lived and out of step with the global bull that began in 2003. As of Thursday's close, A-shares were still 36% under their 1/14/2008 peak. Meanwhile, China's economy kept on chugging, taking Japan's place as the world's second biggest. Not that stocks and GDP should move one-to-one-that isn't how it works ever. But it underscores how China's political climate, capital market controls and sentiment have offset many an economic tailwind.

Exhibit 1: Chinese A-Shares

Source: FactSet, as of 11/14/2014. MSCI China A-Shares return with net dividends, 12/29/2000 - 11/13/2014.

Many believe heavy restrictions on foreign equity investment are a big reason why. Most mainland Chinese don't buy stocks (and not just because they're toiling in the fields). Moneyed cityfolk aren't terribly keen, either. Why? Most A-shares are state-run companies. The party lets some shares float, but ownership remains heavily concentrated among the party elite and the state itself. Individual investors see China's markets the way folks saw America in the Gilded Age-a market controlled and often manipulated by the privileged few. For those who aren't history nerds like us, some of America's worst panics were caused by a few individuals. In 1869, it was Jay Gould and his cronies' ill-fated attempt to corner gold. In 1901, it was Ed Harriman and James J. Hill trying to corner Northern Pacific railroad shares, bidding the price from $110 per share to over $1,000 in less than a day, lifting most of the market with them and setting up the New York Stock Exchange's first crash (and then the biggest decline on record). In 1907, it was Otto and Augustus Heinze's attempt to corner United Copper through the Knickerbocker Trust Company.

Rightly or wrongly, this is how the locals perceive their own market-with a hefty side of financial fraud, book-cooking and corruption. Disclosure requirements, corporate governance and investor protections are weak. Many folks just don't trust their stock market, so they buy real estate-tangible, watchable, and blessed with something sort of resembling the right of private property ownership.

Observers believe the through train will change the landscape some, and maybe they're right. Their logic? More shares will be owned by presumably rational, informed foreigners who follow sound strategies, buy and sell on actual fundamentals and aren't corrupt crony communists. The more foreigners own and trade A-shares, the more mainland China will resemble a normal, modern stock market.

Fair enough! But, there are some caveats. One, foreigners have been able to own A-shares through the Qualified Foreign Institutional Investor (QFII) and Renminbi QFII (RQFII) programs since 2002. Both have strict quotas, totaling only roughly $112 billion. China's performance, shown above, speaks for itself. Two, the through train has a quota, too-$2.1 billion (RMB 13 billion) per day, with a total cap of just over $48 billion (RMB 300 billion). Officials indicate they'll raise it over time (this is officially a six-month trial), just as they've broadened QFII and RQFII, but they have a history of moving glacially. In short, it is questionable whether foreigners will have anywhere near big enough a trading presence to offset the whims of the Party.

There are other, less technical issues to consider. This program has been in the pipeline a while. Chinese officials first announced it in 2007, but it never left the station after the financial crisis derailed their plans. Rumors have swirled in recent years, as officials have incrementally opened the capital account, and the present plan was finally announced in April-fully seven months ago. Markets are pretty darned good at pricing in all widely known information, and investors have known about this one for a good long while. It seems fair to say the news is largely discounted by now-particularly considering how excited folks are today.

While we'd thus caution against viewing the through train as the gravy train, that doesn't mean investors should shun China. If Emerging Markets is your thing, China has plenty of opportunities, like an economy in far better shape than most believe. The Party is also slowly opening the country, loosening capital and trade restrictions. Sentiment surrounding the through train may be elevated, but investors are plenty dour on other aspects of Chinese markets. For Emerging Markets investors, there is plenty to like.

The key is simply to assess China the way you would any other country: Don't get caught up in headline hype, rationally weigh the opportunities and risks, and see how sentiment stacks up with reality.

Stock Market Outlook

Like what you read? Interested in market analysis for your portfolio? Why not download our in-depth analysis of current investing conditions and our forecast for the period ahead. Our latest report looks at key stock market drivers including market, political, and economic factors.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23 -

Economics A Summertime Check-in on US Consumers2026-07-23

-

Market Analysis Why the SOX “Bear Market” Isn’t Foreboding2026-07-21

-

Politics Blunting Burnham?2026-07-21

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today