Personal Wealth Management /

All-Time-High Boredom

Stocks hit an all-time high on Friday—and the news met a rather curious reaction.

For weeks, the Internet has been inundated with stories claiming this year’s ultra-low volatility is lulling investors into a false sense of security. They say folks are getting complacent, assuming bouncing along sideways is the worst thing markets can do (totally Pollyanna, but never mind).

Judging by the reaction to the S&P 500’s latest all-time high, though, this clearly isn’t the case. Investors haven’t been lulled into complacency. They’ve been lulled to sleep.

Time was, a round-numbered all-time high—like the S&P’s push past 1900 to a record-high 1900.53 on Friday—was big news. 1,600—this bull’s first round-number milestone—got a party last May. 1,700 received plenty of fanfare in August. 1,800 caught fire in November with Hunger Games puns galore. 1,900 got some notice, but most reactions are ho-hum. It happened. Few are looking for meaning or making grand proclamations. No one’s calling for an impending crash. No one’s hyping it. No one’s calling for 2000 and beyond, the way they did at 1,700. 1,900 apparently doesn’t “reinforce confidence” the way 1,600 did. Some gripe that it took too long to get there. Bored.

35 years ago, Daniel Kahneman theorized humans magnify the pain of losses. Clearly we do the same with the boredom of flatness. Volatility gets us excited—fearful and greedy. Muted sideways bouncing is a snoozer. Wake us when something interesting happens. Record-high or no, interesting isn’t a 2.8% year-to-date price gain through May 23.

On the bright side, boring is bullish. The lack of “what goes up...” warnings tells us we’re plenty past the pessimistic days of yore. The dearth of “next up, 3,000!” tells us widespread euphoria isn’t here. If all-time highs don’t get our dander up, we’re in a good place—folks aren’t seeing the normal as abnormal. True complacency comes when folks see all-time highs as self-perpetuating. We aren’t there yet. Record-highs occasionally get a brief hat-tip, and the world moves on.

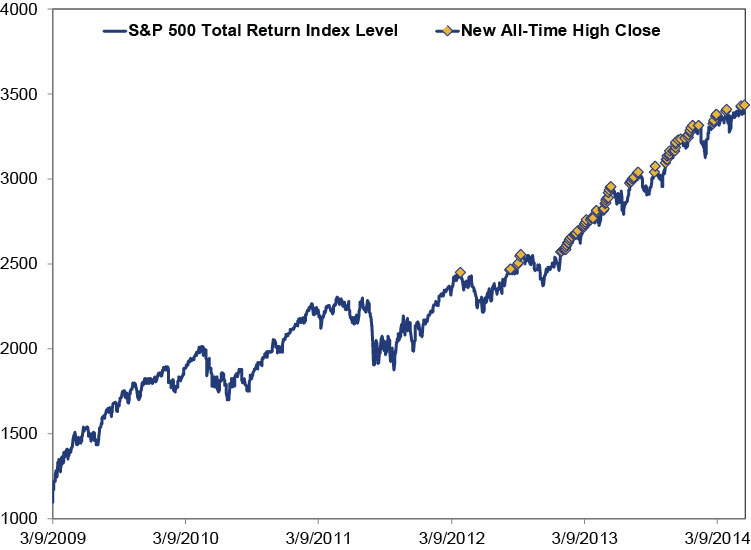

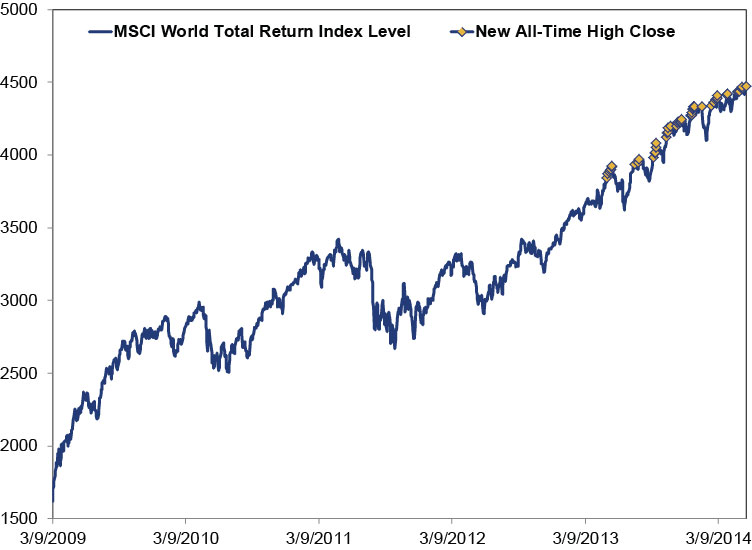

This is how it should be. All-time highs are normal in bull markets. Dozens of them, if not hundreds. The S&P 500 Total Return Index—which includes dividends and better reflects actual returns—hit 153 in the 1980s bull and 347 in the 1990s rager. So far, this one has 95 (Exhibit 1). The MSCI World Total Return Index hit its 52nd Monday (Exhibit 2).

We’ll probably get more. How many more, we can’t say. But as long as folks find them so doggone boring, it’s a fair assumption they won’t stop any time soon. Emotions aren’t too hot or too cold—sentiment, like the economy, is in a Goldilocks sweet spot.

Exhibit 1: S&P 500 Total Return Index

FactSet, as of 5/27/2014. S&P 500 Total Return Index, 3/9/2009-5/26/2014.

Exhibit 2: MSCI World Total Return Index

FactSet, as of 5/27/2014. MSCI World Total Return Index, 3/9/2009-5/23/2014.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets — July 27 - July 312026-08-03

-

Expert Commentary This Week in Review | Fed Meeting, US GDP, Eurozone GDP

2026-07-31

2026-07-31 -

Market Analysis Don’t Fret the EU’s Low Summertime Gas Storage Levels2026-07-31

-

Economics Q2 US GDP’s Stealthy Strength2026-07-31

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today