Personal Wealth Management / Market Analysis

An Interesting Forecast for Interest Rates

Contrary to the crowd, we believe interest rates will end the year lower.

With the Fed expected to hike rates several times this year and inflation picking up recently, most assume higher long-term interest rates are certain to come this year-bringing potential problems along with them. One prominent forecaster made waves recently for saying the 10-Year Treasury yield piercing 2.6% would be a bearish signal for bonds. Others say 3.0% is the magic mark. However, markets often do what the consensus can't fathom, and we believe US 10-year yields will actually finish the year below where they started.

It's true rates have started the year higher. Since 2017 began, the 10-year Treasury yield is up 9 basis points (0.09 percentage point), from 2.45% to 2.54%.[i] Most observers think this is just the start of yields' steady climb, which may not only break but stay above the 2.6% "ceiling" within the next month. This forecast relies on several rationales. One, many expect the Fed to hike its fed-funds target range several times this year, and they presume rising short-term rates beget rising long-term rates. Another factor: expectations for higher inflation. CPI has accelerated since last July and just hit 2.7% y/y in February-the fastest year-on-year rate since February 2012. Along with President Trump's promises of a yuuuuge infrastructure stimulus plan, some worry this increased spending will translate into higher inflation later on.

While inflation expectations do influence long rates, as lenders demand a higher return to compensate for the loss of purchasing power, we don't think the logic supporting the outlook for rising rates holds. From a high level, markets often go against the consensus and do what few anticipate. Since there are virtually universal expectations for long-term rates to rise this year, this argues for flat or falling rates-especially once you consider the logical errors at hand. For instance, a higher 10-year yield today doesn't dictate a steady climb through 2017 since recent past movement says nothing about the future. At 2016's start, the 10-year was at 2.27%. It fell to a low of 1.37% in July and climbed as high as 2.60% in December.[ii] After all those zigs and zags, Treasury yields rose only 18 basis points from year start to year end, finishing at 2.45%.

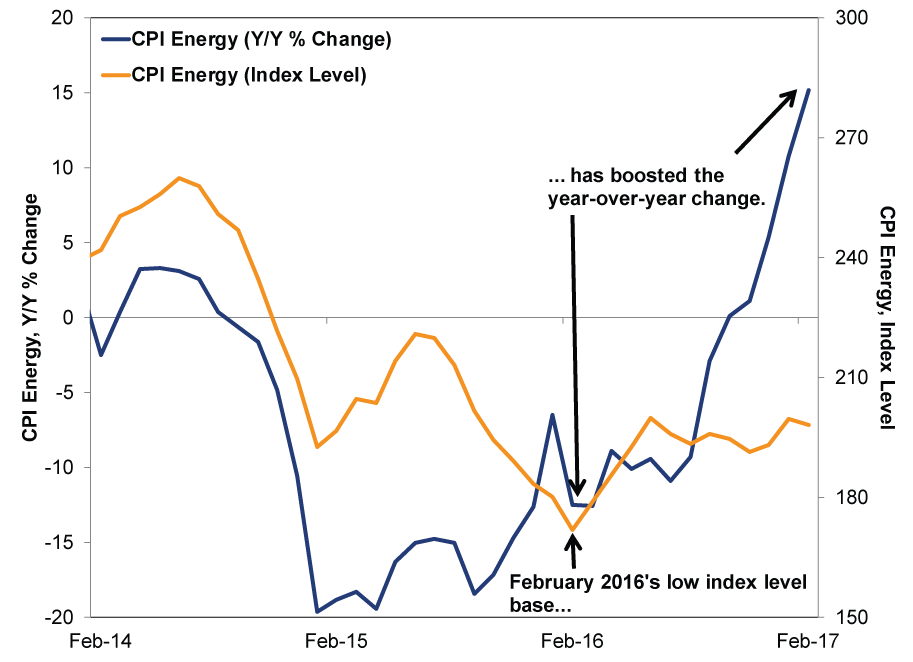

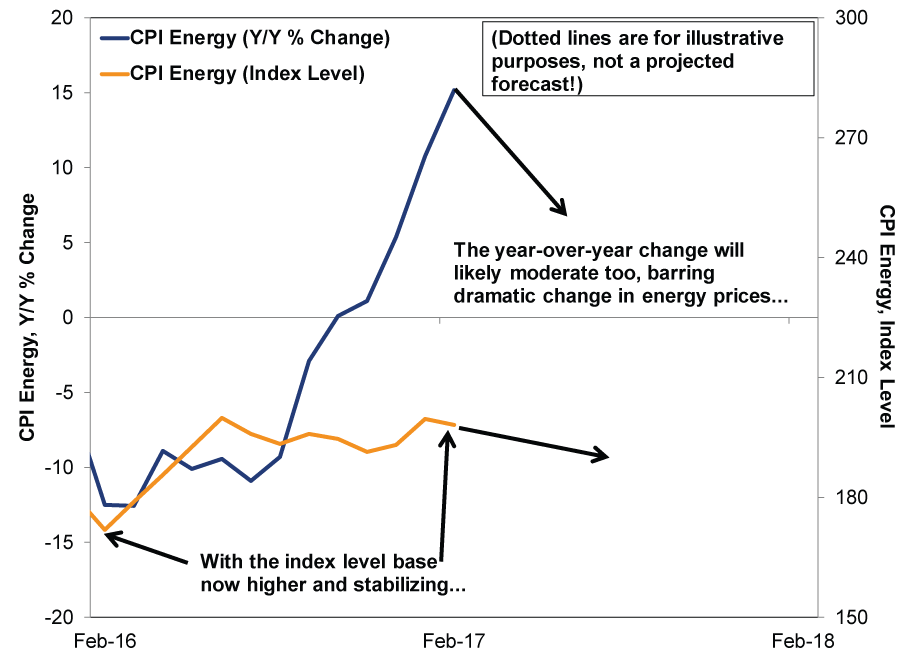

Moreover, rising short rates don't automatically push long rates higher. If they cause inflation expectations to fall, that argues for lower long rates. We see a strong case for this. While CPI has been on the rise, as we explained in greater detail elsewhere, this is a function of math. Plunging energy (namely, oil) prices from 2014 and 2015 skewed CPI over the past couple years. Now that oil prices have stabilized, those year-over-year growth rates won't look as dramatic (presuming oil stays more or less in its current range). February CPI's 2.7% y/y rate is the highest in five years, but this is due to February 2016's low base. Stripping away volatile energy prices, core CPI was 2.2%-right in the 2.0% - 2.3% range it has been in since November 2015. If energy CPI holds steady, energy's y/y growth rate would be much more moderate by October. (Exhibits 1-2)

Exhibit 1: Energy CPI's Skewed Year-Over-Year Comparison

Source: FactSet, as of 3/17/2017. US CPI Energy year-over-year percent change, non-seasonally adjusted (lhs) and US CPI Energy Index Levels (rhs). From February 2014 - February 2017.

Exhibit 2: Stabilizing Energy Prices Portend Moderating CPI

Source: FactSet, as of 3/17/2017. US CPI Energy year-over-year percent change, non-seasonally adjusted (lhs), and US CPI Energy Index Levels (rhs). From February 2016 - February 2018.

People have continually ignored the fact that CPI's gyrations the last few years were just math, and this blind spot likely doesn't go away. Hence, as math moderates CPI, many folks will likely credit the Fed with containing inflation, figuring rate hikes are getting the job done. This tempers future inflation expectations, so with lower inflation risk, investors won't demand higher yield, giving rates room to fall.

Finally, bond markets are global, and what happens overseas affects long-term rates here. With the BoJ and ECB continuing their long-term debt buying spree-pushing down yields in Europe and Japan-investors seek higher-yielding US Treasurys, which lowers yields here. In our view, these various pressures will contribute to long-term rates ending up lower by year's end.

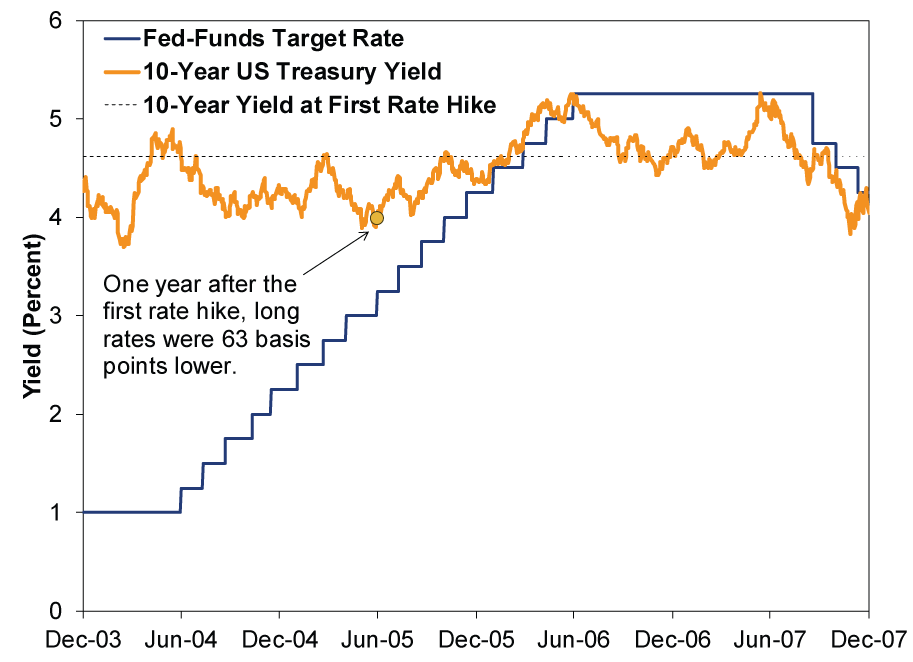

Moreover, for the "conventional wisdom" argument that tighter monetary policy automatically leads to higher long-term rates, history shows this isn't automatically the case. Sometimes it does! But not always, as it depends on the environment. Consider the 2004-2006 stretch during the last bull market. The Fed hiked at 17 straight meetings, yet long-term rates had zero net change from June 30, 2004 - March 6, 2006. (Exhibit 3)

Exhibit 3: Rising Short Rates Don't Always Mean Rising Long Rates

Source: FactSet, as of 1/9/2017. Fed-funds target rate and 10-year US Treasury yield, from 12/31/2003 - 12/31/2007.

We suggest investors refrain from making significant changes to fixed income allocations based solely on forecasts of higher interest rates-they are by no means predestined. Other consensus expectations, like wider credit spreads, are likely off the mark too, so corporate bonds should still do well in this current environment. There doesn't appear to be a need to significantly shorten duration to reduce interest rate sensitivity, either. Since we believe interest rates will end the year lower, bond prices would thus be higher (since they move in opposite directions).

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Pumping Up the Yen?2026-07-17

-

Market Analysis Business Friendly Bureaucracy or No, Britain is Growing2026-07-16

-

Economics Don’t Doubt the Old World2026-07-16

-

Market Analysis On the June Inflation Cooldown2026-07-14

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today