Personal Wealth Management /

An Uneven Clip is No Double Dip

Folks fear the eurozone’s lackluster Q3 GDP growth suggests a double-dip recession, but LEI tells us otherwise.

Thursday, Q3 eurozone GDP showed the region logged its second straight quarter of growth—putting its long recession further in the rearview. However, GDP grew a mere 0.1%—triggering, predictably, fear of a double-dip recession. Critics wag an uneasy finger at Europe’s supposedly “uneven” recovery—we presume that means not all 17 members are advancing or advancing at the same clip. We’ll not argue 0.1% growth is super solid, but these fears are the norm fresh after a recession. However, like the US in 2009 and 2010, the Leading Economic Index (LEI) tells us to remain calm. If a double-dip recession were actually on the horizon, then the eurozone’s LEI gauges wouldn’t be rising! The eurozone economy may not shoot up from here, but LEI tells us growth should continue—likely surprising many.

It’s easy to see the logic behind double-dip dread. The eurozone just emerged from recession in Q2 with 0.3% growth, and Q3’s 0.1% is slower. A handful of countries are contracting—including France, which went from 0.5% growth in Q2 to -0.1% in Q3. And Germany grew, but slower. Anyone looking solely at the recent past would be sorely tempted to deem Q2 an inflection point and Q3 the start of another downward leg.

But economies don’t move on what’s happened in the past—they move on forward-looking conditions. As with stocks, the past doesn’t determine the future. That was then—we’re at now now. The future determines the future! LEI, while not perfect, is a fairly accurate snapshot of what to expect in the future, and right now, LEI tells you growth is likely to continue. Look at the individual components—a handful of the most forward-looking economic variables (just like the US, UK and other national LEI composites). Wider yield spreads are the biggest driver of recent LEI gains, and over a century of evidence tells us wider spreads mean money moves faster—good for growth. The Business Expectations Index—another key contributor—indicates service firms predominantly expect higher activity and demand based on new orders received and similar factors. This wouldn’t be the case if the region were weakening.

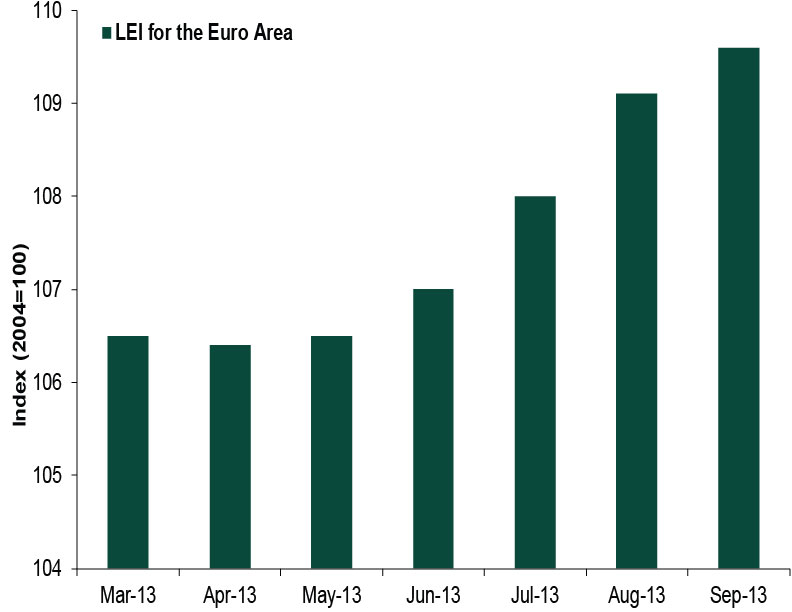

LEI has long helped in predicting economic health—yet few notice it. And few noticed how LEI began falling well before the eurozone recession began, dipped and dived for a while, then started rising in earnest well before GDP turned positive. LEI wobbled a bit earlier this year—presaging the small Q3 GDP wobble—but has gained steam since June. (Exhibit 1) This increase likely speaks to further recovery—as the US has shown for 50 years, a recession has never closely followed a rising LEI trend. Recessions generally begin after LEI has fallen for some time.

Exhibit 1: Eurozone LEI

Source: The Conference Board, Eurostat as of 10/28/2013.

So growth likely continues, but that doesn’t mean every country grows—and as some areas stay weak while others grow, headline regional growth could stay muted for some time. But unevenness isn’t weakness. Germany isn’t Greece isn’t Cyprus—just as was the case during the recession. Greece has shed over 25% of its GDP since 2009, while Germany barely shed any during the region’s recession. Cyprus shrank 0.8% in Q3 and Greece fell, too, but Germany grew 0.3%. Peripheral weakness may drag down the average, but core strength matters more.

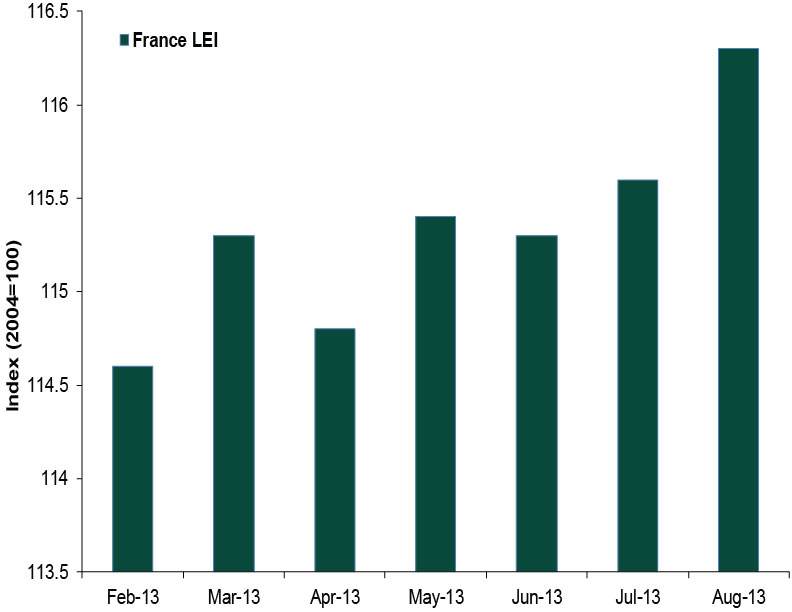

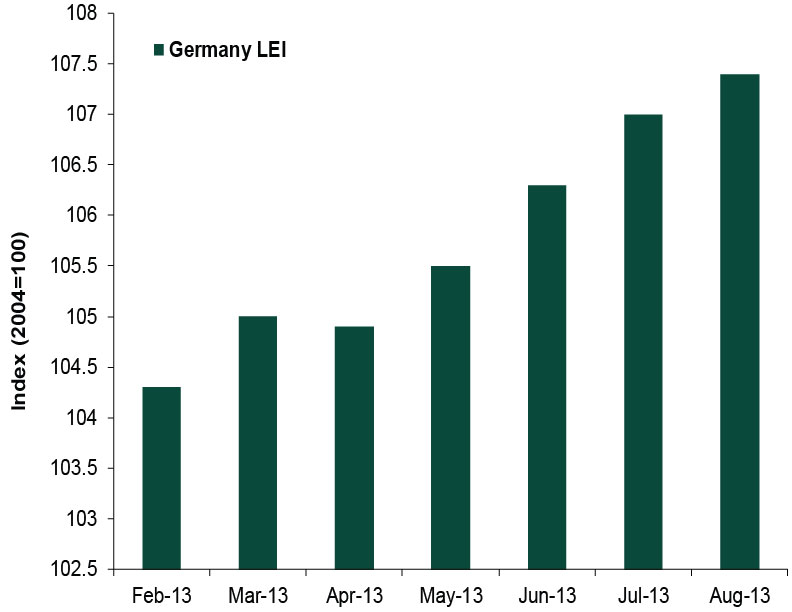

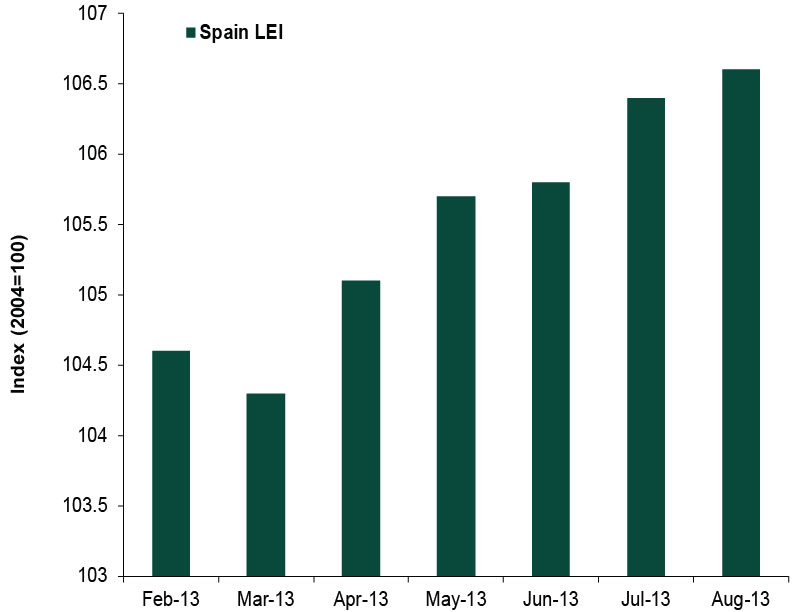

Granted, the bigger economies also diverged a bit, but here, too, LEI indicates the longer-term trend should prove better than many expect. France, for example, fell from 0.5% growth in Q2 to a -0.1% drop in Q3, and many fret eroding competitiveness and high unemployment. But while recent policy moves haven’t been great for the economic landscape, France has managed to grow for decades despite a rather large amount of red tape—a precedent few see. Similarly, few realize unemployment data are backward looking—growth begets jobs, not the other way around. Were it otherwise—if economies couldn’t grow and people couldn’t spend if unemployment were high—growth in spending wouldn’t lead growth in jobs. France’s LEI, by contrast, looks forward—and says growth looks likely to return. Just as Germany’s and Spain’s LEIs mesh well with Q3’s growth. (Exhibits 2-4)

Exhibit 2: France LEI

Source: The Conference Board, Eurostat as of 10/18/2013.

Exhibit 3: Germany LEI

Source: The Conference Board, Eurostat as of 10/23/2013.

Exhibit 4: Spain LEI

Source: The Conference Board, Eurostat as of 10/16/2013.

This isn’t the first time LEI has defied a double dip—we’ve seen this movie before. Take 2009-2010 when people were scared of a double-dip recession in the US—yet LEI was rising, indicating we would be just fine. And we were! No double dip. Growth wasn’t gangbusters, but GDP eventually surpassed the previous high and still grows today (and US LEI says this likely continues).

Eurozone GDP could grow similarly slowly—or slower—looking ahead. Diverging competitiveness throughout the 17-nation bloc is a fact of life for now. But slow, uneven growth likely surprises the many investors who expect the region’s economy to sink. LEI isn’t perfect, but in our view, it’s a strong signal expectations are too dour, and reality is likely to pack the surprise global stocks will appreciate.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Corporate Information How You Benefit from Fisher Investments' Transparent Fee Structure

2026-08-04

2026-08-04 -

Corporate Information How Fisher Investments' High-Touch Service Helps You2026-08-04

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets — July 27 - July 312026-08-03

-

Expert Commentary 3 Things You Need to Know This Week | US Jobs, Trade Balance, Earnings Reports

2026-08-03

2026-08-03

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today