Personal Wealth Management / Market Analysis

An Update on Global Oil Markets

Despite a couple recent high-profile production dips, supply and demand still appear fairly balanced.

While recent declines in Iranian and Venezuelan oil production have spurred worries of a supply crunch driving up oil prices, energy market fundamentals don’t appear much changed since last year. Underappreciated supply growth from other OPEC countries plus still-strong US output suggest global oil markets remain roughly balanced, rendering sharp price moves in either direction unlikely at present. Thus, fears of big oil price hikes choking off economic growth likely remain misplaced. As for Energy stocks, if prices stay stable near current levels as we expect, some larger oil producers could benefit by picking up some slack from lost output in Venezuela and Iran.

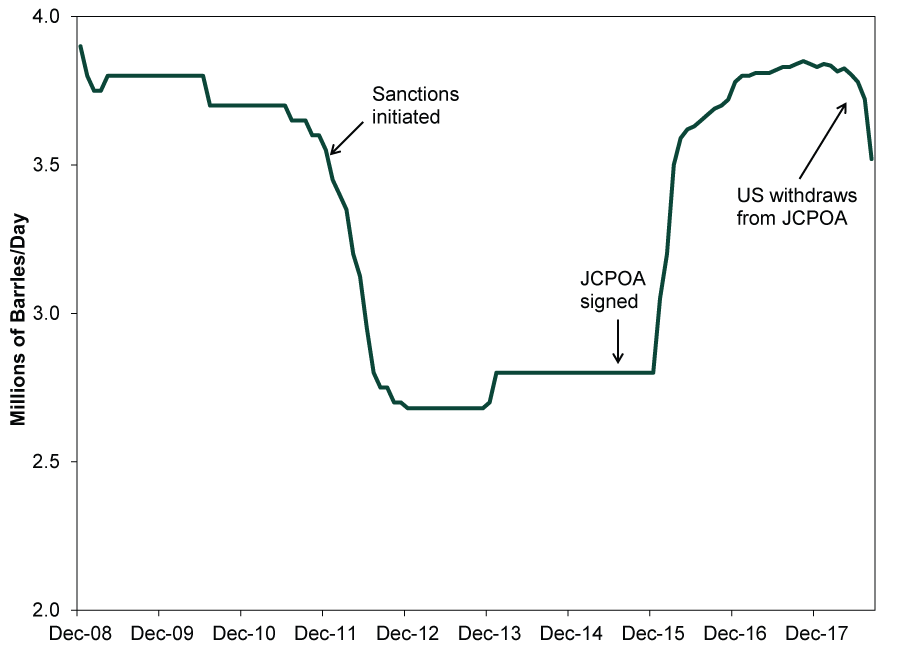

Before the US and Europe imposed sanctions in 2012, Iran was producing 3.7 million barrels of oil per day (bpd).[i] After sanctions cut Iran off from US banking services and most European countries ceased buying Iranian crude, production sank to 2.8 million bpd by November 2013.[ii] In 2015, the Iran nuclear deal—also known by its more cumbersome and vague title, the Joint Comprehensive Plan of Action (JCPOA)—alleviated this pressure. Iran’s exports rebounded fast, reaching 3.8 million bpd in early 2016.[iii]

Since the US withdrew from the JCPOA in May, US sanctions will return—but with big question marks surrounding other countries’ participation. In the lead-up to withdrawal, estimates of Iran’s likely oil output decline varied widely—from as low as a 200,000 bpd to as high as a million.[iv] Reaching the latter figure would probably require US allies to meaningfully curtail their buying and could conceivably lift global oil prices. The US State Department has sent mixed signals about how hard it will push allies to reduce their purchases, initially saying it wanted zero exports from Iran but later promising to grant some waivers.

Although sanctions on Iran’s oil sector don’t officially take effect until November, the country’s crude production has already started to slide, tied to the summertime implementation of sanctions on its Financials sector. (Exhibit 1) In August, it dropped 150,000 bpd from July to 3.63 million bpd.[v]

Exhibit 1: Iranian Crude Oil Production

Source: Energy Information Administration, as of 9/14/2018.

India’s participation may prove key to US sanctions’ effectiveness. The country buys the second-highest amount of Iranian crude (behind China), accounting for 18% of Iranian oil exports.[vi] US Secretary of State Mike Pompeo has told Indian officials that waivers permitting the purchase of Iranian oil will be short-lived.[vii] India’s oil ministry also announced in June that refiners should prepare for “a drastic reduction or zero” oil imports from Iran starting in November.[viii] Likely as a consequence, India’s Reliance Industries—which operates the largest refinery in the world—bought no Iranian crude in August.[ix] They and two other Indian energy firms have also noted they have no purchases planned for September and October.[x] South Korea, the third-largest buyer of Iranian crude, reportedly hasn’t shipped any Iranian oil in 75 days.[xi] If these two stick to their guns, Iranian oil output likely falls significantly, potentially dampening global supply growth. For now, though, this is mostly just something to watch. Same goes for Iran’s production situation overall. It is likely still too soon to say how much impact US sanctions will have on Iranian output or exports—much less on global oil prices.

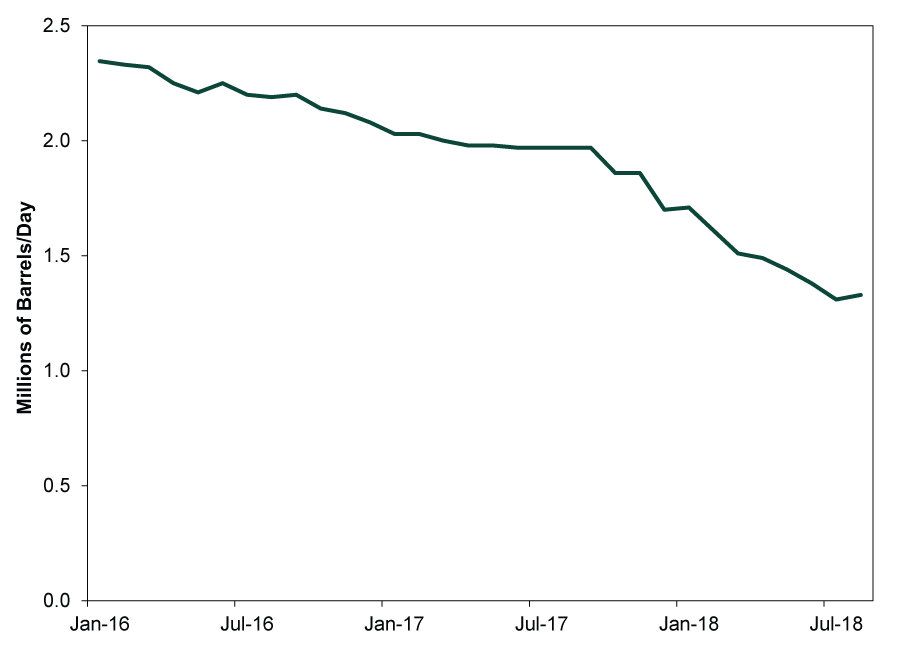

Supply constraint worries aren’t limited to Iran. Amid Venezuela’s worsening economic and humanitarian crisis, many anticipate the chaos will knock the country’s oil production even further. As recently as 2016, Venezuela was churning out 2.2 million bpd. That number has since dropped to 1.3 million bpd.

Exhibit 2: Venezuelan Crude Oil Production

Source: Energy Information Administration, as of 9/14/2018.

In an extreme scenario involving disruptions from a coup or a long-shot UN or US intervention, Venezuelan oil output could sink. But such geopolitical concerns are seemingly ever-present in many less developed (and less stable) oil-producing countries. However awful, troubles like these aren’t novel for markets. Moreover, media has consistently covered Venezuela’s plight—including its actual (and potential) effects on oil markets. This likely limits surprise power.

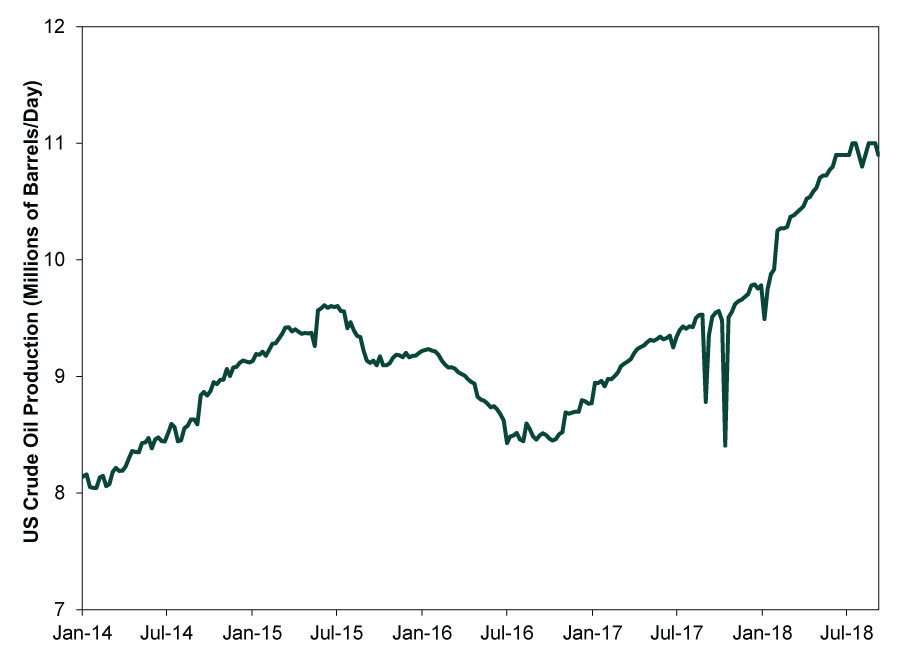

Beyond Iran and Venezuela, global oil supply looks to be in much better shape. Take the US, where—despite production holding mostly steady since hitting 10.9 million bpd in June—output has grown markedly year-to-date.[xii] (Exhibit 3) US shale still appears to be supporting global supply in a big way.

Exhibit 3: US Crude Oil Production

Source: FactSet, as of 9/14/2018.

Flattish US oil output growth of late alongside supply uncertainty elsewhere has probably contributed to crude prices’ recent uptick. But the former may be partly the result of Permian operators’ slowing activity modestly due to recent pipeline bottlenecks.[xiii] These holdups appear temporary, though, likely fading next year and removing one production impediment.[xiv]

Lastly, an International Energy Agency (IEA) report showed OPEC production surged in August, rising 420,000 bpd and more than offsetting Iran’s 150,000 bpd decline.[xv] Here, too, the much-discussed output crunch doesn’t seem to be materializing.

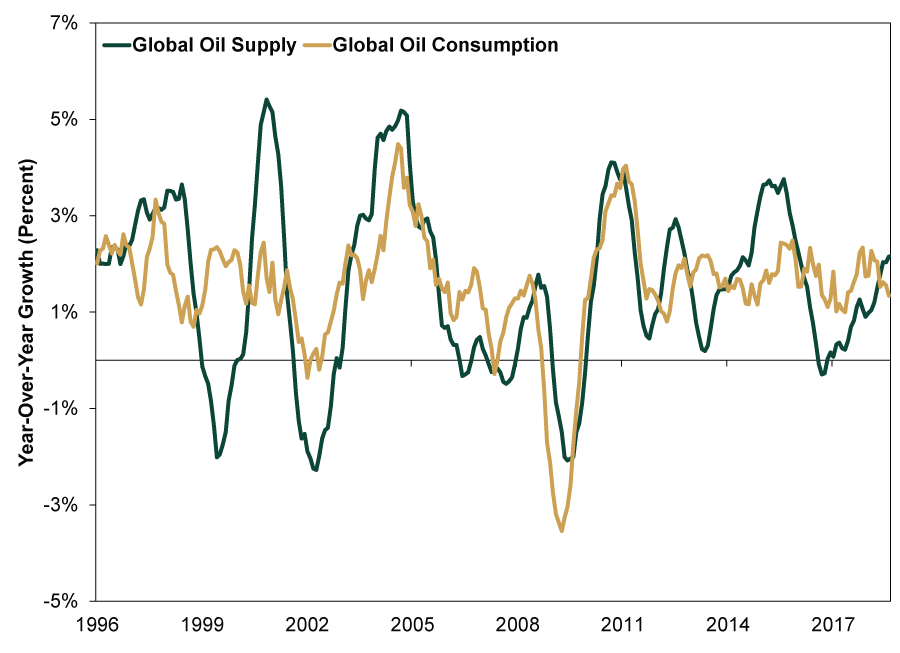

More broadly, global oil market metrics still show strong supply growth relative to demand. Averaging the prior 6 months shows oil supply growth of 2.2% y/y, while consumption has grown a tamer 1.3%. (Exhibit 4) This seemingly belies concerns of Iranian oil production cuts (and other supply disruptions) meaningfully tightening global oil markets.

Exhibit 4: Global Oil Supply and Demand

Source: FactSet, as of 9/17/2018.

The major sources of alleged supply tightness today appear temporary (see: the US), well-known (Venezuela) or unknowable at present (Iran). Meanwhile, demand appears robust. Conditions in the oil patch could change, but for now, there don’t appear to be strong reasons for oil demand to outpace supply hugely and send prices soaring.

[i] “Iran’s oil exports not expected to increase significantly despite recent negotiations,” Mark J. Eshbaugh, Energy Information Administration, 12/10/2013.

[ii] Ibid.

[iii] “OPEC to keep oil gushing,” Staff, Deutsche Welle, 2/6/2016.

[iv] “Oil price shoots higher as Trump quits Iran nuclear deal,” Gregory Meyer and David Shepherd, Financial Times, 5/9/2018.

[v] “Global Oil Supply Hit a Record High in August as OPEC Ramps Up Production,” Christopher Alessi, The Wall Street Journal, 9/13/2018.

[vi] Source: Energy Information Administration, as of 9/14/2018.

[vii] “India's Iran oil purchases to fade ahead of U.S. sanctions,” Nidhi Verma, Reuters, 9/13/2018.

[viii] Ibid.

[ix] “India's August imports of Iran oil down a third month-on-month: sources,” Nidhi Verma, Reuters, 9/5/2018.

[x] “India's Iran oil purchases to fade ahead of U.S. sanctions,” Nidhi Verma, Reuters, 9/13/2018.

[xi] “In Big Win for Trump, U.S. Sanctions Cripple Iranian Oil Exports,” Javier Blas, Bloomberg, 9/17/2018.

[xii] “U.S. shale oil production to rise to 7.6 million barrels per day in October,” Jessica Resnick-Ault, Reuters, 9/17/2018.

[xiii] “Bigger Oil Pipelines Are Coming to West Texas to Ease Bottleneck,” Rebecca Elliott, The Wall Street Journal, 7/30/2018.

[xiv] Ibid.

[xv] “Global Oil Supply Hit a Record High in August as OPEC Ramps Up Production,” Christopher Alessi, The Wall Street Journal, 9/13/2018.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Insights Ken Fisher on Crypto, Inflation, Annuities and More - June 20262026-06-30

-

Market Analysis Investors Are (Still) Fighting the Last War on Inflation2026-06-30

-

Market Analysis Reader Mailbag: June 20262026-06-30

-

Expert Commentary 3 Things You Need to Know This Week | Midterm Miracle, US Jobs, Tax Planning

2026-06-29

2026-06-29

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today