Personal Wealth Management / Economics

As January Ends, Global Economy Still Looks Healthy

January flash PMIs show major developed economies are chugging along.

As we approach January’s close, pundits remain transfixed on the state of the global economy. Recession chatter has quieted, but many see the expansion as sluggish and worry developments like the Wuhan coronavirus will knock growth. As fears command headlines, some key and timely indicators seem overlooked: The latest PMI data, which show major developed economies continued growing as 2020 kicked off.

Here are IHS Markit’s January flash purchasing managers’ indexes (PMIs).

Exhibit 1: January’s Flash PMIs

Source: FactSet, as of 1/27/2020.

PMIs are monthly surveys measuring whether business activity rose or fell across different industries. Readings over 50 indicate expansion; below 50, contraction. PMIs have their limits, as they show only the breadth of growth—not the magnitude. Moreover, flash estimates are subject to revision since they are based on approximately 85% – 90% of total survey responses. Still, PMIs are useful snapshots of how businesses are faring.

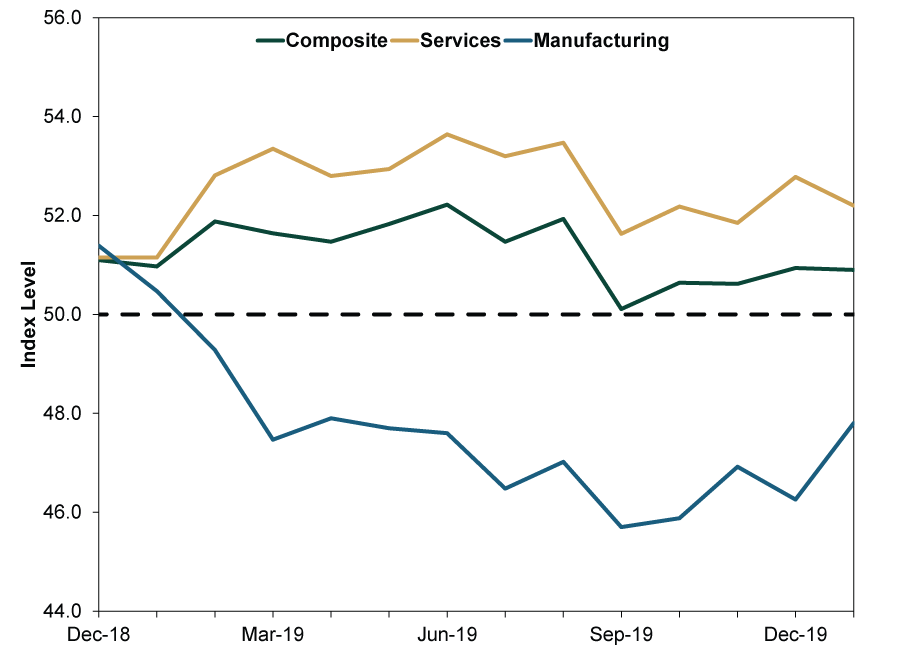

The PMI that most caught our eye was the UK’s, as it showed the composite PMI returning to growth after a months-long slump, suggesting Brexit uncertainty is less of a headwind. For much of last year companies held off on business investment while they awaited clarity. First, Brexit looked set to happen by March 29, and with no deal in sight, business pulled economic activity ahead in anticipation of a “no-deal” scenario. When politicians pushed the deadline to October 31 at the last minute, many companies were left with a supply overhang, which weighed on production in subsequent months. That repeated, perhaps to a lesser extent, in October, when Brexit was then pushed back another three months to today.

Exhibit 2: UK PMIs, December 2019 – January 2020

Source: FactSet, as of 1/28/2020. IHS Markit UK composite, services and manufacturing PMIs, December 2018 – January 2020 (flash).

Much of that uncertainty dissipated following December’s general election, which delivered Prime Minister Boris Johnson a resounding Parliamentary majority—enabling him to push his Brexit deal through. Of course, not all is clear, as the UK and EU are now wrangling over a new trade deal. However, UK businesses now have a much better idea of what they are dealing with, and January’s PMI likely reflects some of that newfound clarity. As January’s flash report noted, “Survey respondents often commented on hopes that an end to domestic political indecision will have a favourable impact on business investment and help to sustain a more favourable economic landscape.” Future data will confirm whether January’s rebound is a blip or not, but in our view, just knowing Brexit will happen is a positive for both businesses and investors, allowing them to move on.

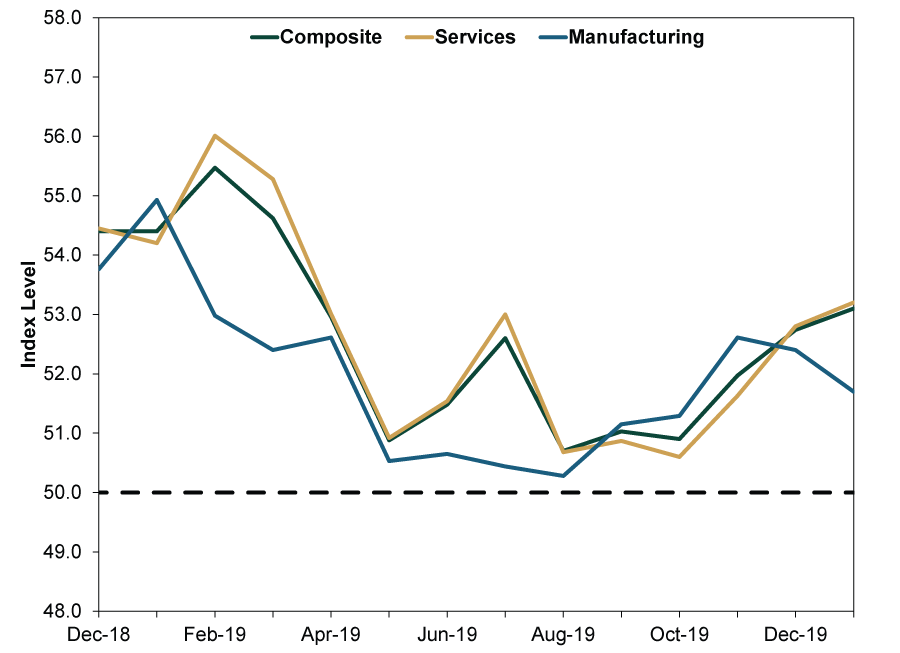

As for other major developed economies, January’s flash PMIs extended the global expansion’s recent story: Ongoing manufacturing weakness gets attention, but services industries continue driving growth. In Europe, manufacturing has been below 50 since February 2019, but January’s 47.8 was the highest since April as fewer firms reported contraction. It is still too early to say eurozone manufacturing is on the rebound, but the contraction has been easing since September—perhaps signaling the worst has passed. Less noticed, though more noteworthy, in our view: The eurozone services PMI continues expanding.

Exhibit 3: Eurozone PMIs, December 2019 – January 2020

Source: FactSet, as of 1/28/2020. IHS Markit eurozone services and manufacturing PMIs, December 2018 – January 2020 (flash).

Markit’s PMIs never showed US manufacturing contracting last year (the ISM PMIs, which survey fewer businesses but have a longer history, did). It just showed growth was noticeably less broad-based, while services held up better. After improving in recent months, manufacturing slowed again in January, which we suspect stems from cash-strapped shale oil producers tightening their belts. But services kept doing the heavy lifting, fueling America’s solid private sector-led expansion.

Exhibit 4: US PMIs, December 2019 – January 2020

Source: FactSet, as of 1/28/2020. IHS Markit US services and manufacturing PMIs, December 2018 – January 2020 (flash)

The primary reason the manufacturing-driven mid-cycle slowdown didn’t trip developed world economies as badly as many projected: Services and consumption dominate economic output. (Exhibit 4) Steady growth in those industries pulled the flagging parts of the economy along.

Exhibit 5: Economic Breakdown

Source: OECD, as of 1/29/2020. Value Added by Activity. Heavy Industry includes manufacturing, energy and construction. May not sum to 100% due to rounding. Table reflects latest available annual data: 2018 for UK and Euro Area and 2017 for USA.

In our view, these data reinforce an important point: Stocks don’t need gangbusters economic growth to rise. Last year’s manufacturing struggles didn’t prevent global stocks from having their best year in a decade. With global growth likely to continue this year, we think investors should evaluate how reality squares with expectations. As folks start warming up to a better-than-appreciated reality, the gap between reality and expectations narrows. However, false fears—like the coronavirus and geopolitical tension—still get attention, suggesting euphoric sentiment remains at bay. In our view, stocks can still do fine in this environment, justifying a bullish outlook in 2020.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis The New Tariffs in Town Are Still Old News2026-07-24

-

Expert Commentary This Week in Review | Market Volatility, Tariffs, SpaceX

2026-07-24

2026-07-24 -

Economics A Summertime Check-in on US Consumers2026-07-23

-

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today