Personal Wealth Management / Market Analysis

Be Averse to Mean Reversion Arguments

Markets are never “due” to behave in a certain manner based on averages, in our view.

Just over two months from the stock market’s lowest point (at least thus far) this year in late-March, a number of pundits are wondering whether its growth-led rally has legs to continue into the year’s second half. Many answer this question with variations of “no.” Some see more downside ahead, pointing to the bear market’s short duration. Others claim that whichever way broad markets head, growth’s huge outperformance this year means a reversal looms. Both theories seemingly hinge on mean reversion—a common investing flaw, in our view, since markets are never “due” to reverse course tied to the gravitational pull of an average or norm.

Mean reversion is another way to refer to the “law of averages.” The thinking goes, if an extreme event occurs, the opposite will inevitably transpire to preserve the historical average. Variations of this argument arise often in markets. As the last bull market went on to become history’s longest, folks frequently fretted that its longer-than-average length meant imminent trouble. Similarly, many spent much of the last bull market worrying far-lower-than-average interest rates would revert, dooming a “bond bubble.”

But now, such theories are mushrooming tied to various aspects of stocks’ recent swings. For example, some argue stocks can’t be in a new bull market yet because bear markets have averaged 14 months in length since 1950.[i] A few compare the COVID bear market to some of history’s biggest—most of which lasted 18 months and required more than five-and-a-half years to regain all-time highs.[ii] Their conclusion: Stocks won’t return to pre-lockdown highs until 2025. Beyond the duration debate, other observers have pondered whether a style leadership shift is afoot. Growth has led value for years, leading many to speculate a reversal is “due.” Yet it didn’t happen. Now, with growth stocks leading value by 26.5 percentage points in the trailing 12 months—the widest gap in decades—proponents argue that long-awaited rotation must be at hand.[iii]

In our view, though, mean reversion doesn’t impact markets and shouldn’t form the basis of an investment decision. For one, long-term averages consist of individually extreme components that display no particular pattern. Just as bull markets aren’t uniform, bear market returns and durations fluctuate, too.

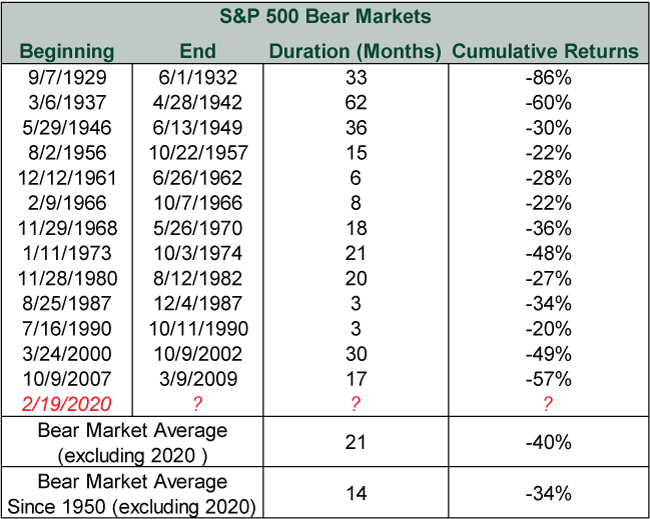

Exhibit 1: S&P 500 Bear Markets Since 1929

Source: Global Financial Data, Inc. and FactSet, as of 3/19/2020. S&P 500 Price Index, 1/3/1928 – 3/9/2009.

Note: We aren’t arguing the bear market is over. Hindsight is the only way to know that—and it can take many months. But should March 23 end up holding as the low, this bear market’s cumulative returns would be -34.0%, equaling the post-1950 average.[iv] Yet duration-wise, the bear market would have lasted a little more than a month—the shortest in modern history. Those presuming it still had many months to go based solely on long-term averages would have missed significant early bull market returns.

We believe similar logic applies to the growth versus value debate. Value’s relative lag stems from recent economic trends. Since value stocks are usually in economically sensitive sectors, they tend to move with the business cycle. During recession, value stocks typically get hit harder, sending prices to irrationally low levels. That, coupled with rampant pessimism common at bear market bottoms, tees up value stocks for a big rebound at the onset of the next bull market. As the bull market matures, growth eventually takes the lead as investors start preferring companies with faster earnings growth and higher margins. This leadership shift happened in the 2009 – 2020 bull market. Value led from 2009 – 2012 before giving way to growth, which then led for years. Many thought that positioned growth stocks for a massive decline in the next bear market—reverting returns toward the mean.

But that hasn’t happened. Growth has overall led during the downturn and the upturn thus far. In that way, the coronavirus-related bear market looks more like a correction. When the bear market began, the global economy was still growing and investor sentiment was far from euphoric. In a typical business cycle, recession forces businesses to cut excesses—setting the stage for smaller value firms to do well during the recovery. But if the global economy returns to some semblance of normalcy soon, the economic trends from the past bull market may persist—thereby potentially continuing to favor growth. For that trend to reverse, value proponents would likely have to capitulate—a sign of plunging sentiment—possible, but not assured. In that scenario, the gap between reality and rock-bottom expectations would be bullish for value stocks. That is possible—and it is something we are closely monitoring. But making a choice merely based on mean reversion doesn’t seem sound to us.

The key to any market outlook isn’t what happened and how it relates to historical averages. It is the future—and how that reality relates to expectations.

[i] “Could This Be More Than a Bear Market Rally?” Justin Waring, UBS, April 9, 2020.

[ii] Source: “A Reality Check for Market Bulls: It’s Going to Be a Long Slog for Stocks,” Howard Gold, MarketWatch, April 8, 2020.

[iii] “Growth Stocks Outperforming Value by Widest Margin in Decades,” Akane Otani, The Wall Street Journal, May 19, 2020. Outperformance figure source: FactSet, as of 5/29/2020. Russell 1000 Value Total Return Index and Russell 1000 Growth Total Return Index, 5/28/2019 – 5/28/2020.

[iv] Source: FactSet, as of 5/27/2020. S&P 500 Price Index, 2/19/2020 – 3/23/2020.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Economics Quick Hit: Durably Broad-Based Growth2026-07-29

-

Market Analysis On the Chop in the Oil Market2026-07-29

-

Politics Takaichi Raises Japan’s Wall of Worry2026-07-27

-

In The News Why Kevin Warsh should think twice about hiking interest rates — even as anxiety over the Iran war grows2026-07-27

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today