Personal Wealth Management /

Breaking Down the ECB’s Wrongheaded ‘Stimulus,’ Q&A Style

The ECB’s latest move is unnecessary and counterproductive, but we think this bull market will persist regardless.

Well, there you have it. Early Thursday morning Pacific Time, ECB head Mario Draghi announced the bank’s Monetary Policy Committee had determined a -0.4% short-term policy rate and 10-year German bunds at -0.59% weren’t low enough to entice borrowers and goad banks to lend.[i] So with the eurozone economy slowing some, they announced new “stimulus.” That stimulus? Cutting short-term rates more and resuming quantitative easing (QE) bond purchases. In our view, these moves are unnecessary and counterproductive, but they are also unlikely to derail the bull market. Let us break this down for you, Q&A style.

Q: What in the world did the ECB do?

A: As noted, the bank cut the interest it “pays” banks to hold excess reserves by 10 basis points to -0.5%. Because this rate is negative, it amounts to the ECB charging banks a fee on excess reserves—an effort to prod them to lend (thus converting excess reserves to required reserves, which aren’t charged the negative interest rate). At a more granular level, they announced they would enact a two-tiered system that exempted a portion of banks’ excess reserves from negative rates and lowered interest rates on a program offering super cheap funding to banks, providing they lend the money. In addition, the ECB restarted its QE program of buying sovereign and corporate bonds at a €20 billion monthly rate, an effort to lower long-term interest rates and thereby stimulate loan demand.

Q: Why did they think this was necessary?

A: The ECB argues this program is a safeguard to ensure the recent economic slowdown doesn’t get worse. Policymakers also noted the bank has a 2% y/y inflation target they haven’t come close to hitting in recent years, absent a couple fleeting episodes when oil prices jumped. They think more lending would increase money supply, stoke inflation and stimulate growth.

Q: Are they wrong?

A: At a high level, the idea of stoking lending to boost money supply and growth is correct. But the tactics here are bizarre, confusing low rates with easy money.

Banks borrow at short-term rates to fund long-term loans. The spread between short and long rates, depicted via the yield curve, influences lending’s profitability. People—and banks consist of people—respond to incentives like profits. If lending is profitable, expect banks to extend credit. By lowering long rates, QE weighs on banks’ loan profits! There is little logic in this. We mean, while the ECB is busy arguing long rates need to be lower, pundits are in a tizzy over America’s inverted yield curve—a supposed sign of recession ahead. The US curve inverted because long rates plummeted below short. How does it make sense to simultaneously fear falling long rates and cheer a policy designed to reduce them further? Yet in the weird world we live in, many of the same pundits who fear flat-to-inverted yield curves are comfortable calling ECB policy “stimulus.”

Moreover, America, Britain, Japan and the eurozone all tried QE previously. Loan growth didn’t speed. Inflation floundered. Growth was sluggish. Europe and America would benefit from higher long rates that steepen yield curves. Not lower.

As for negative rates, they also hit bank profits—unless banks pass them on to depositors or dodge them. Hence, some European banks have been charging large institutional depositors a corresponding fee since rates went negative in 2014. In August, a couple banks in non-euro Switzerland and Denmark announced they would begin charging larger retail customers fees on deposits.

To dodge negative rates on excess reserves, many banks buy bonds. Hence, high-quality sovereign debt is broadly negative-yielding in the eurozone, Denmark, Switzerland and Japan—all nations sporting negative short-term rates. While holding a negative-yielding bond from issuance to maturity would ensure a loss, prices are quite sensitive to interest rates in the interim, providing at least the opportunity to break even. Especially if rates fall further.

Finally, if the ECB’s objective in enacting negative rates is to goad banks to lend, why shield a portion of excess reserves through tiering?

Q: OK, none of that sounds great. But you all say it isn’t a big deal, either. What gives?

A: While the ECB’s moves aren’t good, they don’t represent the huge, landmark shift so many claim. For one, short rates were already negative. Ten basis points more doesn’t seem like a game-changer. Restarting QE is negative, but the size and scope isn’t big. At its peak rate, the ECB was buying €80 billion monthly in 2016. The new €20 billion rate is far below that, likely too small to move rates much. Further, many hype the fact the ECB didn’t set an expiration date on QE. But the bank’s rules state they can own only up to one-third of any member state’s sovereign debt. With the past round still on the books, that leaves little room. Hence, soon-to-be ECB head Christine Lagarde will have to change this guideline to continue pursuing asset purchases for long. That isn’t assured, given rising dissent among policymakers. The ECB is taking a step in the wrong direction, but it is a baby step.

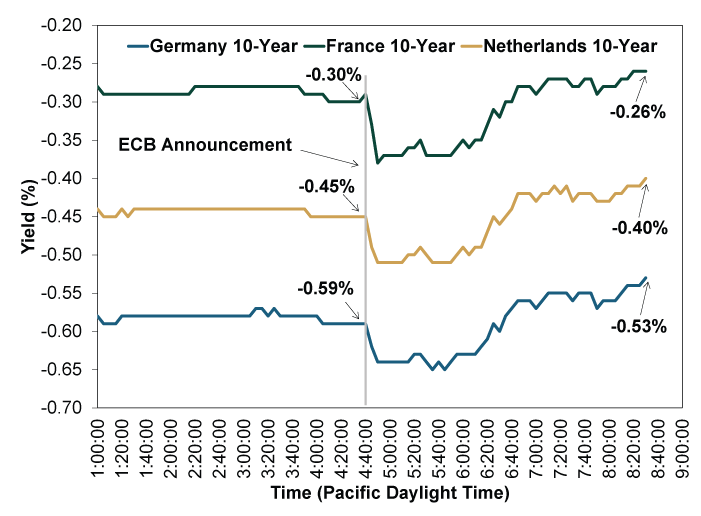

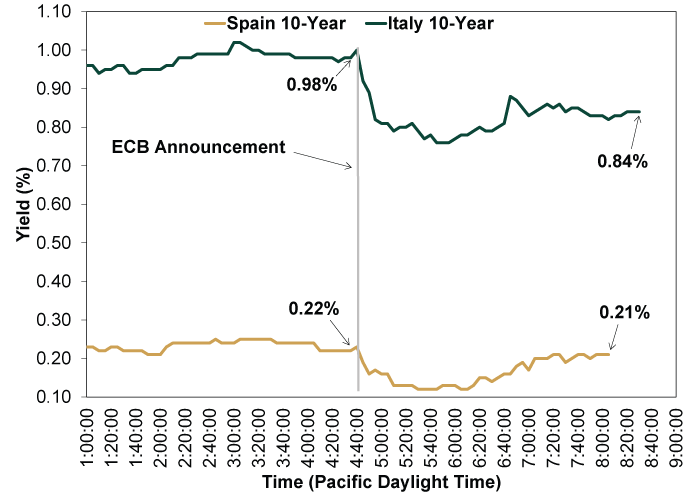

Further, markets pre-price widely expected announcements like this. They have spent months hearing chatter about QE, deeper negative rates and more. Essentially, markets already moved on this “news.” Extremely myopic Exhibits 1 and 2 show this by plotting the intraday movement in 10-year bond yields for five major eurozone nations. As Exhibit 1 shows, German, French and Dutch rates rose after the announcement. While Italian and Spanish rates fell a touch, they were off the lows by market close.

Exhibit 1: German, French and Dutch Yields Rose Post-ECB Announcement

Source: FactSet, as of 9/12/2019. Intraday movement on 9/12/2019.

Exhibit 2: Spanish and Italian Yields Fell a Bit Post-ECB Announcement, but Not Much

Source: FactSet, as of 9/12/2019. Intraday movement on 9/12/2019.

Finally, while these policies aren’t great, they have existed for long stretches of this bull market. Would we be happier without them? You betcha. But stocks have risen in spite of low-interest-rate tight money for years. We see little reason to think this episode is massively different.

Q: What about the euro? Isn’t this move really about weakening it to boost exports?

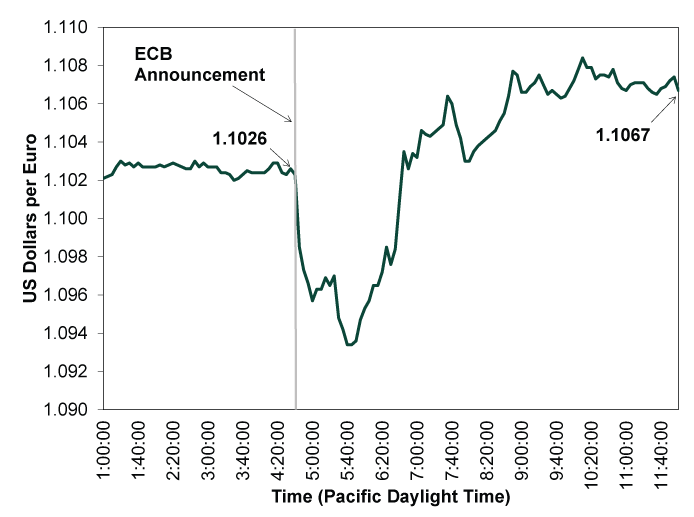

A: That is what many claimed following the announcement, but we doubt it. The ECB has long stated it doesn’t target exchange rates—which policymakers repeated when asked this morning. But even if that is a smoke screen, it doesn’t much matter. The idea a weak currency is a huge economic boost is a fallacy. In today’s world, very few products are produced 100% in one country or region. Companies source components, raw materials and more from abroad. A weak currency jacks up those costs. Weak currencies also don’t automatically translate into more economic activity. Japan saw this in the 2012 – 2013 timeframe, when the yen tumbled. Rather than cut prices for consumers abroad to boost volumes, exporters simply pocketed extra yen as a profit boost. Oh and here too: Markets pre-price widely expected moves. Hence, the euro strengthened against the dollar after the ECB’s announcement. (Exhibit 3)

Exhibit 3: After a Wiggle, the Euro Strengthened Against the Dollar

Source: FactSet, as of 9/12/2019. Intraday movement on 9/12/2019.

[i] Source: FactSet, as of 9/12/2019. German 10-year bund rate as of 9/12/2019 at 4:35 AM Pacific Daylight Time.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary 3 Things You Need to Know This Week | Q2 Earnings, ECB Meeting, Trump Accounts

2026-07-20

2026-07-20 -

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—July 13 - July 172026-07-20

-

Expert Commentary This Week in Review | US-Iran Conflict, US Inflation, New UK Prime Minister

2026-07-17

2026-07-17 -

Market Analysis Pumping Up the Yen?2026-07-17

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today