Personal Wealth Management / Market Volatility

Bull Market Bounciness Isn’t a Call to Action

Volatility calls for discipline, not action.

The past several weeks have seen some volatility return, with global stocks falling -5.5% from September 6 to October 4’s low, then rebounding to close less than 1% from where they started today.[i] Still, we see pundits suggesting now is the time to raise cash, arguing the likelihood of more negativity is high. Holding more cash in anticipation of rocky stretches may sound sensible, but doing so could cost you dearly. Let us review.

There are myriad reasons for holding cash, some more beneficial than others. For example, cash is a near-necessity in a right-sized emergency fund or for a known or planned expenditure—two scenarios where any volatility is likely a huge problem. Cash also can make sense as part of a defensive strategy during a bear market, perhaps alongside bonds and other securities, depending on market conditions. However, we think it makes sense to go this route only if you see a bear market forming and have based your assessment on careful fundamental analysis, not merely recent returns. In our view, pundits’ reason for raising cash now is less beneficial. Some see recent volatility as a call to pare back stock holdings to “protect” capital while also building up some “dry powder” to put to work after a decline.

That sounds nice in theory, but in our view, it falls apart in practice. Volatility doesn’t announce its arrival or departure, and a short negative spell doesn’t beget more market bounciness. As we wrote throughout the year, markets had been relatively calm in 2021—until September. But last month’s dip doesn’t say anything about future market movement. Yes, more negative volatility is always possible, and if stocks fall anew, recent calls to hold cash for future buying opportunities will look prescient. But volatility goes both ways. If markets go through a stretch of positive volatility, that better buying opportunity you are waiting for may be in the rearview already.

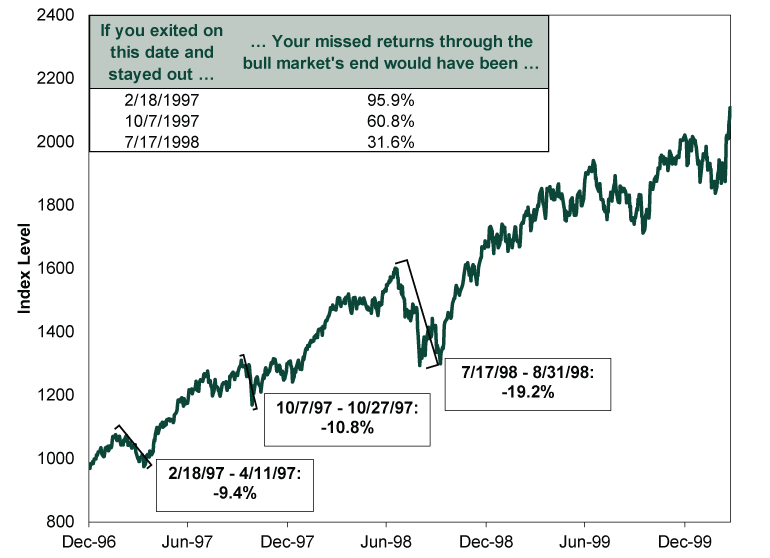

Take the 1990s bull market. Though the S&P 500 endured some sharp pullbacks in 1997 and a big correction in 1998, those bouts of negativity didn’t end the bull market, which charged on until its peak in March 2000. To illustrate the potential opportunity cost, Exhibit 1 shows the returns investors would have missed if they went to cash at the start of a pullback or correction but didn’t buy back in during the rest of the bull market.

Exhibit 1: Reacting to Negative Volatility Can Be Costly, 1997 – 2000

Source: FactSet, as of 10/20/2021. S&P 500 Total Return Index, 12/31/1996 – 3/24/2000.

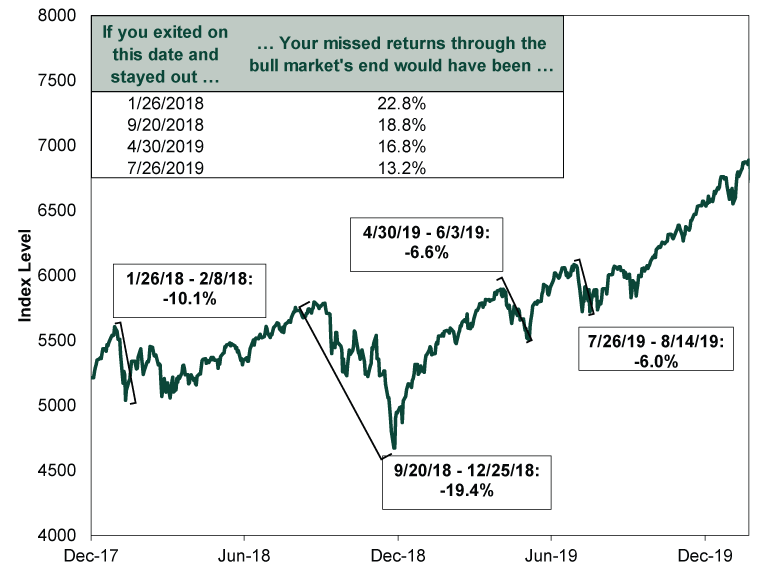

More recently, 2018 featured two periods of sharp negative volatility, including a late-year correction that left US stocks down for the year. However, unless they perfectly timed the beginning and ending of those downturns, investors who built up cash to deploy at a “better” time risked missing out on a stellar 2019. (Exhibit 2)

Exhibit 2: Reacting to Negative Volatility Can Be Costly, 2018 – 2020

Source: FactSet, as of 10/20/2021. S&P 500 Total Return Index, 12/31/2017 – 2/19/2020.

Now, to address the elephant in the room: Yes, a bear market struck within two months of 2019’s end. For those who had loads of cash, this was your ultimate buying opportunity. But we strongly doubt too many people with “dry powder” were rushing to deploy it in late March 2020, when pessimism and fear of a new depression reigned. Mostly, we saw lots of pundits and investors arguing for months and months thereafter that the new bull market was disconnected from a dire reality—and sure to reverse before long.

That brings us to a critical point: If you up your cash holdings with the intent of deploying them at a “better” time, you also have to determine when to buy back in. With hindsight and a chart, the ideal reentry points—a market trough—look obvious. But in the moment, many investors attempting to time the market fail to do so, in our experience. Stocks are the rare thing people tend not to want to buy when they are on sale. Sentiment is usually dour following a market decline, and it gets more so the further stocks fall. Hence, many investors seek confirmation the worst has passed before acting. But stocks don’t sound an “all-clear” signal, and those waiting for one may end up missing the very buying opportunity they were waiting for. In our view, enduring those volatile days, weeks or months helps ensure you don’t miss a bull market’s returns over the longer run.

Again, if you see an actual bear market forming, it can make sense to reduce your stock exposure significantly. Those declines are typically long, deeper than -20% and grinding. Since they begin and end for fundamental reasons, if you are careful and disciplined, you can mitigate the risk of getting whipsawed. That isn’t the case with corrections or pullbacks, which are sentiment-driven. That is why they defy predictability—sheer irrationality at work. They are also normal during bull markets. During bull markets, the S&P 500’s average annualized return is 21%—a figure that includes all of the unpredictable pullbacks and corrections over the past 90 years.[ii] To us, that is the reward for dealing with volatility.

Rather than get hung up on the prospect of near-term dips, we recommend taking a higher-level view and focusing on market cycles. As Fisher Investments founder and Executive Chairman Ken Fisher has said, “If you aren’t in a bear market, you are in a bull market.” Investors who need long-term growth must participate fully in bull markets to reap their gains, which includes enduring a lot of uncomfortable volatility. To instill discipline, we suggest investors reframe how they treat market pullbacks. Rather than as a call to action, view them as the price to pay for bull markets’ long-term returns.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis The New Tariffs in Town Are Still Old News2026-07-24

-

Expert Commentary This Week in Review | Market Volatility, Tariffs, SpaceX

2026-07-24

2026-07-24 -

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23 -

Economics A Summertime Check-in on US Consumers2026-07-23

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today