Personal Wealth Management / Market Analysis

Chart of the Day: The Other Fund Flows

Bond markets are subject to sentiment swings, too.

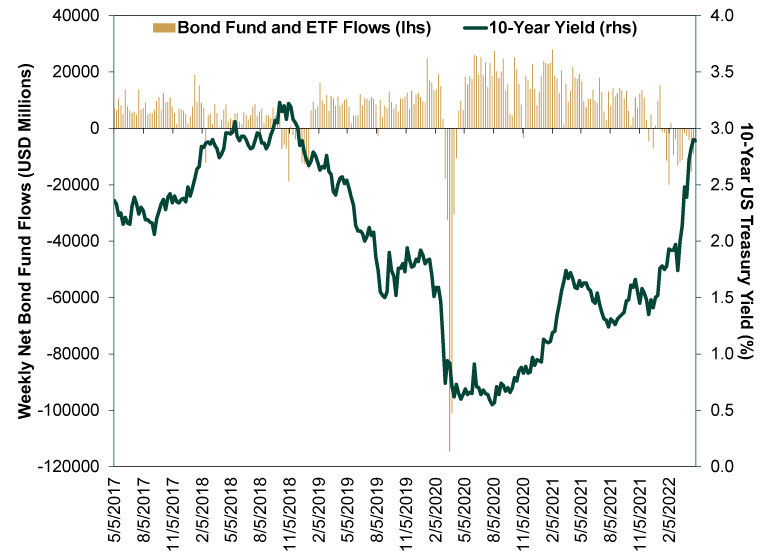

Over the years, we have occasionally checked in on the net movement of dollars into and out of stock funds (“fund flows”) as a loose, very imperfect sign of sentiment, on the theory that they give some insight into how people feel about stocks from week to week—particularly when they are at extremes. Yet they are generally pretty noisy and not all that conclusive. But bond flows have been a bit more interesting. While normally positive, they have had three distinct negative stretches in the past five years: in late 2018 – early 2019, as rising rate chatter spooked investors; during the worst of 2020’s lockdowns; and now.

Exhibit 1: Sentiment Clues in Bond Fund Flows?

Source: FactSet, as of 5/6/2022. Net bond mutual fund and ETF inflows and 10-year US Treasury yield (constant maturity), weekly, 5/5/2017 – 4/29/2022.

We hesitate to draw big conclusions from the recent outflows. They do seem to undercut the whole notion that investors fled bonds for stocks when rates were lower and are now poised to reverse that, given higher yields. But beyond this, they are a reminder that bond markets, like stocks, are prone to sentiment-fueled moves now and then.

Today, 10-year yields’ journey north of 3.0% is getting heaps of attention. Pundits say things like, bonds’ 40-year bull market is over. (A statement that glosses over cycles by starting from the late 1970s and early 1980s record-high interest rates, for what it is worth.) But they said that an awful lot in 2018, too, and what happened? The spike didn’t last. Yields fell just when most expected the spike to continue on higher. They took a different path than the masses expected, as markets often do. All liquid markets deal efficiently with widely known information, including forecasts and widely held expectations. In 2018, they priced talk of higher rates and then went about their daily business of pricing longer-term inflation expectations.

Is that a blueprint for today? Over the medium term or so, we think it probably is. There is a strong whiff of a sentiment freakout in bond markets right now, and it doesn’t quite square with market-based long-term inflation expectations, which remain quite tame despite CPI’s latest lurch higher. We think the sharp exodus from bond funds speaks to that as well—people are ditching well-reasoned long-term asset allocations because of recent performance, which is rarely a beneficial move. It all suggests bond markets are being Ben Graham’s proverbial short-term voting machine, demonstrating the instant irrationality that occasionally befalls all marketplaces. Which also suggests they should eventually return to weighing long-term expectations.

None of this predicts when the tide will turn. It is an interesting observation, not a timing tool. But we do think it argues against the long bond bear market thesis.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis The Politics and Practicalities of the Social Security Trust Fund2026-06-16

-

Market Analysis Gold Fails the Safe Haven Test Again2026-06-16

-

Market Analysis A Market Perspective on Iran Truce Whisperings2026-06-15

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—June 8 - June 122026-06-15

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today