Personal Wealth Management / Market Analysis

Context Is Everything

About those wobbles in bond and stock markets …

Volatility returned mid-week, with a one-two punch hitting US Treasurys and stocks on Wednesday and Thursday. First, 10-year yields jumped 10 basis points from 3.05% to 3.15% on Wednesday, arbitrarily described in some coverage as the largest move since President Trump took office.[i] That allegedly bled over into stocks Thursday, with most European and Asian benchmarks down around -1% – -2% and the S&P 500 price index losing -0.8%.[ii] The culprit, supposedly, was the dastardly combination of strong US economic data and Fed head Jerome Powell, who said some things that made people fear aggressive interest rate hikes through next year. We think this is all rather overwrought, and not just because rate hike jitters are one of this bull market’s many false fears. Rather, it seems people misinterpreted Powell and didn’t fully read his comments.

Best we can tell, Powell seems to have delivered his not-so-magic words in two venues: a Tuesday speech at the National Association for Business Economics in Boston and a Wednesday sit-down with PBS’s Judy Woodruff. The soundbite repeated all over the Internet is this: “Interest rates are still accommodative, but we’re gradually moving to a place where they will be neutral. We may go past neutral, but we’re a long way from neutral at this point, probably.” That echoes a half-sentence from the closing of his Boston speech: “Our ongoing policy of interest rate normalization reflects our efforts to balance the inevitable risks that come with extraordinary times …” Ergo, everyone thinks interest rates are off to the races.

Trouble is, Powell’s entire speech, which you can read here, was all about why inflation is low and why the Fed doesn’t expect much inflation in the foreseeable future. Relevant clips include:

“For example, the medians of the most recent projections from FOMC participants and the Survey of Professional Forecasters, as well as the most recent Congressional Budget Office (CBO) forecast, all have the unemployment rate remaining below 4 percent through the end of 2020, with inflation staying very near 2 percent over the same period. From the standpoint of our dual mandate, this is a remarkably positive outlook.”

“The baseline forecasts of most FOMC participants and a broad range of others show unemployment remaining below 4 percent for an extended period, with inflation steady near 2 percent. I have made the case that this forecast is not too good to be true and does not signal the death of the Phillips curve. Instead, the outlook is consistent with evidence of a very flat Phillips curve and inflation expectations anchored near 2 percent.”[iii]

“As you probably know from our public communications, we carefully monitor survey- and market-based proxies for expectations, and we do not see evidence of a material shift in longer-term expectations. The survey measures have been particularly steady for some time. The financial market-based measures include both an expectations component and a volatile inflation premium component, so they tend to move around much more than the surveys, but we see no evidence of a material change in these measures, either.”

“Wages and compensation data are one important source of information. These measures have picked up some recently, but in a way that is quite welcome. Specifically, the rise in wages is broadly consistent with observed rates of price inflation and labor productivity growth and therefore does not point to an overheating labor market. Further, higher wage growth alone need not be inflationary. The late 1990s episode of low unemployment saw wages rise faster than inflation plus productivity growth without an appreciable rise in inflation.”

So, to sum up, Powell doesn’t see much risk of high inflation. This is important. Not just because less inflation probably means less Fed tightening, but because inflation is a primary driver of long-term interest rates. People who buy Treasury bonds are generally looking for the interest payments to outpace inflation enough that they make a little bit of money on a long-term loan to the government. As inflation and inflation expectations rise, people will demand a higher interest rate. Without rising inflation, a sustained rise in long-term interest rates doesn’t make a ton of sense. Hence, this is our first clue that investors overreacted.

Our second clue: the yield curve. Even if you do think Powell’s comments presage several more interest rate hikes, this isn’t reason for long rates to soar. Overnight rates, which the Fed controls, don’t have a preset relationship with long rates. The market prices long rates, and those rates move on supply and demand—with inflation expectations the chief demand driver. Contrary to all the above chatter about wages, which are an after-effect of inflation rather than a cause, inflation’s primary driver is money supply growth. Prices rise when too much money chases too few goods and services. So you generally don’t get fast-rising inflation without money supply growing faster than the broader economy for a sustained period. In a fractional reserve banking system, where banks create most new money through lending, you don’t get fast-rising money supply without fast loan growth. Banks base most lending decisions on the risk-reward tradeoff, with the estimated reward based on their net interest margin—basically, the interest rate they’ll get from the loan minus the interest rate they pay to get short-term funding. In other words, long-term interest rates minus short-term interest rates. You can eyeball this gap by looking at the yield curve.

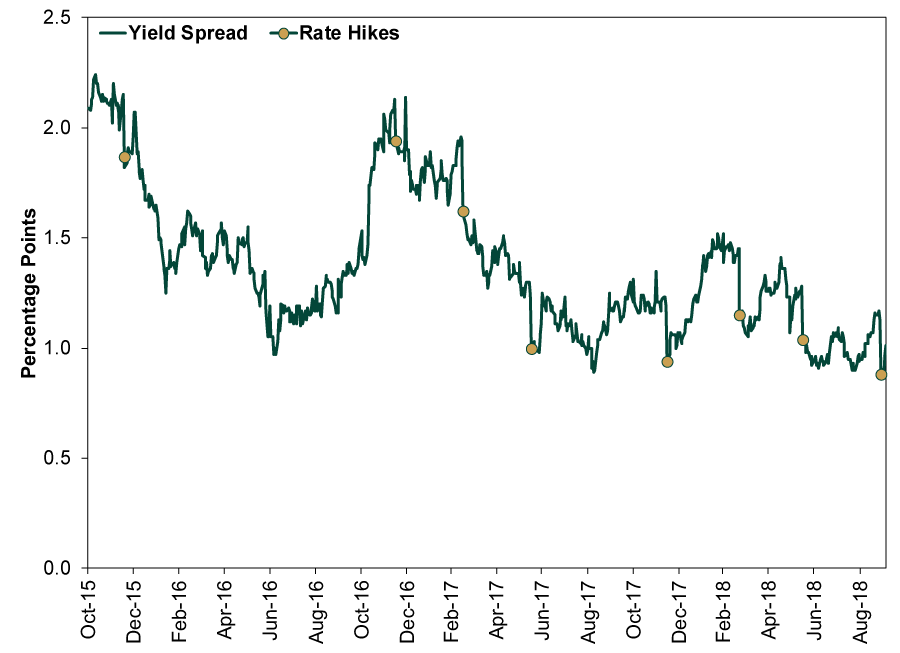

Do so (Exhibit 1), and you will see it has flattened lately. The gap between 10-year yields and the effective fed-funds rate was 1.52 percentage points (or if you prefer, 152 basis points) on February 21. After Thursday’s close, it is only 1.01 percentage point. That includes this week’s uptick in long rates. Overall, the spread is a little more than half what it was when the Fed started hiking rates way back in December 2015. We would expect this to bring low inflation, not hot. Seems to us the bigger risk lurking on the horizon is that the Fed overshoots during an arbitrary quest for “normal” interest rates, inverts the yield curve and ends the party. The global yield curve, meanwhile, has barely budged over the last year, with the spread between 3-month and 10-year yields at 0.9 percentage point in September (versus 1.0 percentage point a year prior).[iv]

Exhibit 1: The Yield Curve Spread

Source: FactSet and Federal Reserve, as of 10/4/2018. 10-year US Treasury yield minus effective fed-funds rate, daily, 10/31/2015 – 10/4/2018.

The main lesson of markets’ swings, in our view, is that bond markets aren’t immune to short-term volatility. They can overreact, just like stocks. Lesson two, we think, is that while any old thing can impact stocks on a daily basis, stocks and interest rates aren’t linked. If rising long rates are so bad for stocks, then why is the S&P 500 up double digits year to date while 10-year yields are up 79 basis points? Why are there numerous other instances in history where stocks and bond yields rose together?

[i] Source: FactSet, as of 10/4/2018.

[ii] Ibid.

[iii] The Phillips curve posits a link between unemployment and inflation. We don’t subscribe to this, as explained here, but we’ll let Powell run with it this time.

[iv] Source: FactSet, as of 9/11/2018.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Politics Blunting Burnham?2026-07-21

-

Market Analysis Why the SOX “Bear Market” Isn’t Foreboding2026-07-21

-

Expert Commentary 3 Things You Need to Know This Week | Q2 Earnings, ECB Meeting, Trump Accounts

2026-07-20

2026-07-20 -

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—July 13 - July 172026-07-20

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today