Personal Wealth Management / Market Analysis

Don’t Bank on Financials Leading

Some may wonder whether it is Financials time to shine; we don’t expect it to.

When value stocks led briefly last fall as good vaccine news shot sentiment higher, many presumed it was the start of a longer-lasting leadership rotation that would benefit banks—value stalwarts. While that rally has since faded, some suspect it previews what is to come once reopening really kicks in. Presumably, that would jumpstart loan demand, supercharging bank earnings. We think that thesis overlooks a lot of contrary evidence, though, and jumping headlong into banks probably isn’t a winning move.

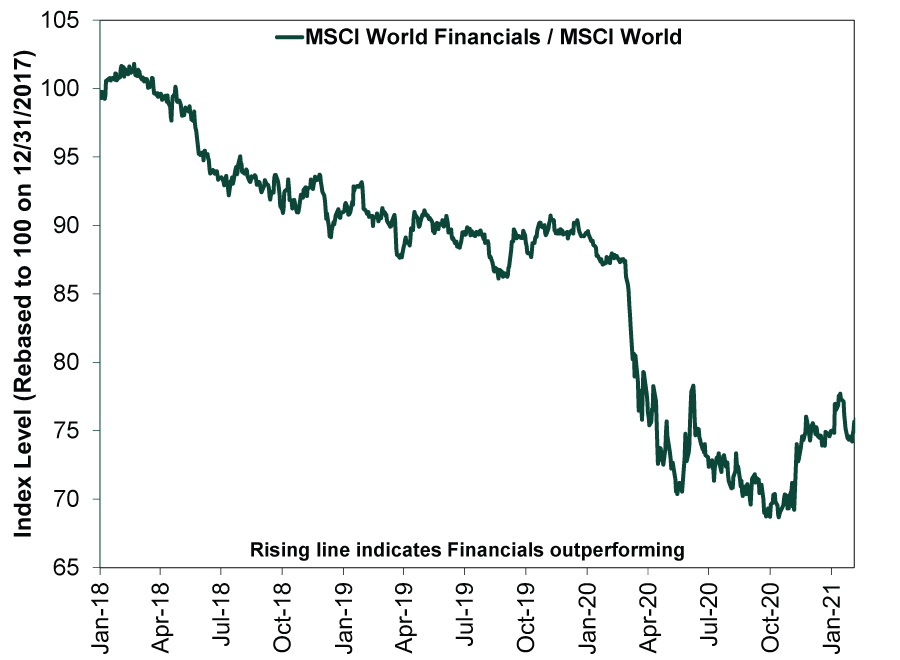

Exhibit 1: Despite Several Countertrends, Financials Have Underperformed for Years

Source: FactSet, as of 2/9/2021. MSCI World Financials and MSCI World, both with net dividends, 12/31/2017 – 2/8/2021. Financials index divided by World index rebased to 100 on 12/31/2017.

As Exhibit 1 shows, Financials have underperformed for years, tied to value’s lag. Many pundits suggest that makes it “due,” particularly since, on paper, we are in a young bull market that began last March. Because economically sensitive value stocks tend to lead early and Financials constitute value stocks’ biggest sector—with banks its chief industry—some think November’s rally is a prelude to their leadership.[i] If vaccine news can be so bullish, imagine what an actual widespread rollout could do!

It isn’t just their share of the index that makes banks key to value. Value companies typically depend on bank lending to fund their operations, especially smaller firms unable to tap the corporate bond market. In turn, the yield curve drives banks’ willingness to lend, as they borrow at short rates, lend at long rates and pocket the difference. When the yield curve steepens, banks’ loan profitability tends to swell, giving them more incentive to extend credit and fuel economically sensitive firms’ expansion.

Some see the yield curve as added fuel for value. The 10-year Treasury yield exceeded the 3-month by 0.4 percentage points last August. It is now up to 1.1 percentage points.[ii] Meanwhile, with 59 out of 65 S&P 500 Financials companies reporting as of February 9, Q4 earnings have jumped 17.2% y/y versus expectations for a -9.4% decline at 2020’s end.[iii] Outside America, developed world Financials tell a similar tale, with Q4 earnings up 17.1% y/y against initial expectations for a -27.2% drop, albeit with only about a quarter of reports in. Pundits also tout US banks’ potential to buy back shares with the Fed’s blessing after they passed December’s stress tests. Some believe the extra demand—and reduced share count—will further boost prices.

But without greater fundamental improvement in banks’ primary driver—the lending environment—we don’t expect sustained outperformance. First, banks’ positive earnings surprise stemmed largely from trading activity and the release of loan loss reserves.[v] It generally wasn’t from higher loan growth or bigger net interest margins.[vi] Big banks capitalized on last quarter’s record equity trading, which many attribute to individual investors’ buying frenzy. While that has extended into this year, banks don’t expect a repeat. Meanwhile, loan delinquencies and defaults haven’t been as dire as forecast. Banks typically set aside reserves for expected bad loans, hitting profits before recording any actual loss. If fewer loans sour than expected, they release these reserves, adding to profits. But the move is effectively backward-looking.

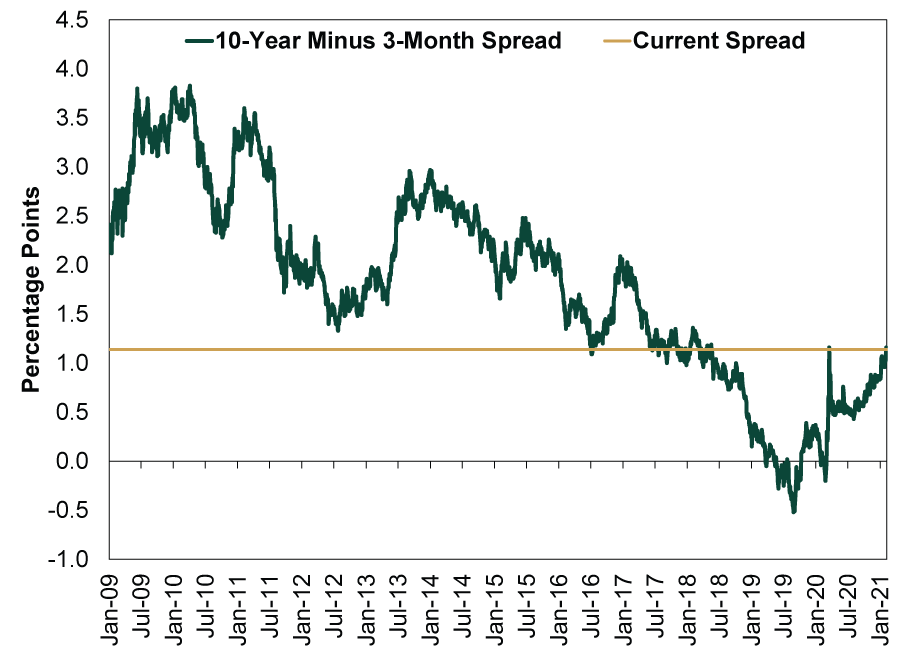

Although the yield curve is steeper, as Exhibit 2 shows, it is still flatter than the vast majority of the last bull market. It probably isn’t enough to generate much loan growth, which has steadily decelerated from its CARES Act boost last May to January’s lowest rate in seven years.[vii] According to the Fed’s latest Q1 survey, banks’ senior loan officers continue to see challenging conditions ahead and are restricting credit access for a significant slice of borrowers, further suggesting a lending rebound isn’t likely any time soon.[viii] They expect delinquency and default rates to worsen throughout 2021. This implies banks still need to provision, limiting the reserves they can release and their willingness to lend.

Exhibit 2: Yield Curve Still Pretty Flat

Source: FactSet, as of 2/9/2021. 10-year minus 3-month Treasury yield spread, 1/1/2009 – 2/8/2021.

No doubt some loan improvement is likely with vaccinations and further reopening, but this knowledge is widespread—and largely priced. Less appreciated: Markets aren’t acting like this is a new bull market. Despite countertrends, growth has led. Sentiment is broadly optimistic, a late bull market feature. The yield curve also isn’t likely to steepen much. Supply and demand continue to weigh on long-term interest rates. Treasury issuance is mainly at the short end—five years or less—leaving a dearth of long-term Treasurys for private buyers. With developed market sovereign yields below US rates across the board, global Treasury demand probably won’t abate—money generally chases the highest-yielding asset. Meanwhile, the Fed’s quantitative easing long-term bond purchases persist.

Owning some Financials and maintaining exposure to value stocks is sensible as part of a counterstrategy. This is the heart of diversification, in our view—knowing the future isn’t predetermined and you can always be wrong. But the environment we expect doesn’t favor them leading.

[i] Source: FactSet, as of 2/9/2021. Statement based on MSCI World Value Index sector weights, 2/8/2021.

[ii] Source: Federal Reserve Bank of St. Louis, as of 2/9/2021. 10-year minus 3-month Treasury yield spread, 8/4/2020 – 2/9/2021.

[iii] Source: FactSet, as of 2/9/2021.

[iv] Ibid. MSCI World Index ex. USA Financials Q4 earnings, 2/9/2021.

[v] “Wall Street Traders Propelled Bumper Quarter for Biggest Banks,” Shahien Nasiripour, Bloomberg, 1/20/2021.

[vi] “How Wall Street Reflects the Economy Biden Inherits,” Andrew Ross Sorkin, Jason Karaian, Michael J. de la Merced, Lauren Hirsch and Ephrat Livni, The New York Times, 1/21/2021.

[vii] Source: Federal Reserve Bank of St. Louis, as of 2/9/2021. Loans and leases in bank credit, 5/6/2020 – 1/27/2021.

[viii] “Senior Loan Officer Opinion Survey on Bank Lending Practices,” Staff, Federal Reserve, 2/1/2021.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Politics The Tenth Question Facing Alberta2026-08-06

-

Market Analysis Western Oil and Gas Producers Are Ramping Up2026-08-06

-

Corporate Information How You Benefit from Fisher Investments' Transparent Fee Structure

2026-08-04

2026-08-04 -

Corporate Information How Fisher Investments' High-Touch Service Helps You2026-08-04

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today