Personal Wealth Management / Market Analysis

Don’t Gush Over Oil Stocks

Considering diving into Energy stocks? Better check the water's depth.

With the big bull market now more than six years old, some investors seem to be on a quest to find the remaining "cheap" stocks they believe have more upside potential-leading some to home in on Energy stocks, given the sector's more than -20% decline from late last June through Q1's close. Now, as we've written, there is nothing about allegedly "cheap" stocks that suggests they'll perform better looking forward. To argue otherwise is to suggest value is a permanently superior style of investing to growth, a fallacy. But also, Energy stocks don't seem particularly cheap by most measures. We would caution against diving into Energy today-your better prospects, in our view, lie elsewhere.

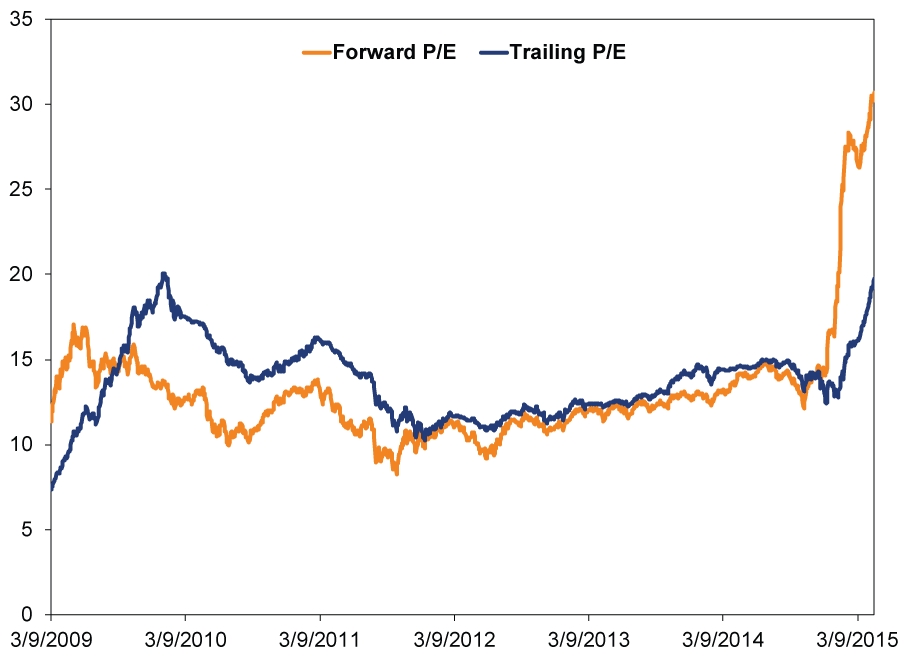

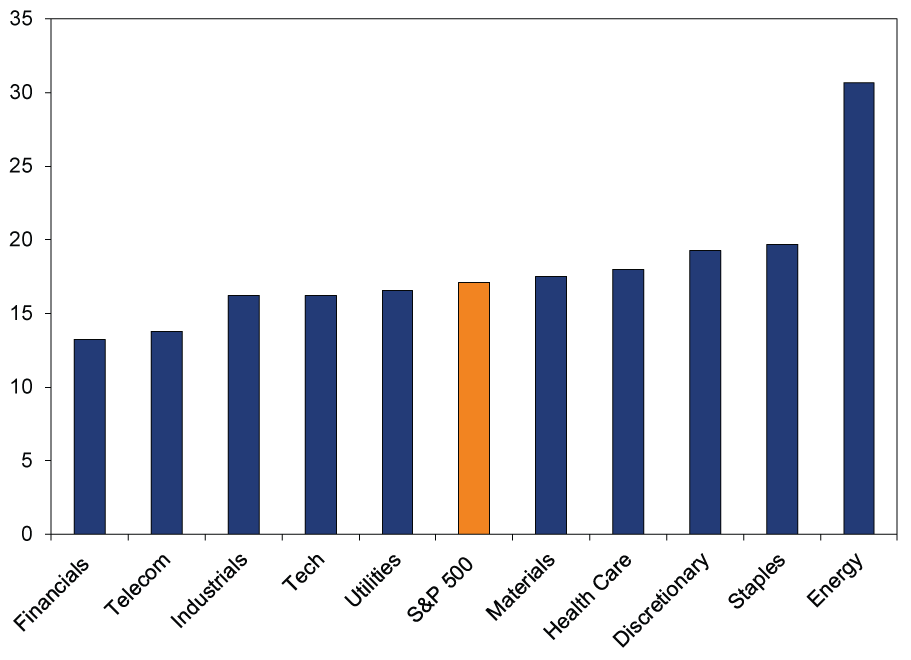

For one thing, if it's cheap stocks you seek, Energy doesn't meet the traditional definition in any meaningful sense. Yes, the sector, as measured by the S&P 500 Energy Sector Index, is down significantly, tied to oil prices' steep collapse since last year. But earnings have collapsed more. That means traditional valuation measures of the Energy sector have gone up. Exhibit 1 shows the spiking 12-month forward and trailing Energy sector price-to-earnings ratios (P/Es) in the last year. Exhibit 2 shows that on a forward P/E basis, the Energy sector is the most expensive sector of the market. Now, far be it from us to argue valuations predict returns! They don't! But they are a signpost of sentiment. Take this in concert with recent media claims that Energy is a screaming buy, and positive net inflows into Commodity-oriented ETFs (suggesting folks are acting on this impulse), and there doesn't seem to be much suggesting oil stocks are super cheap.

Exhibit 1: Energy Sector Forward and Trailing P/Es

Source: Factset, S&P 500 Energy Sector Forward and Trailing 12-month P/Es, 3/9/2009 - 4/23/2015.

Exhibit 2: S&P 500 Sector Forward 12-Month P/Es

Source: Factset, S&P 500 Forward 12-Month P/Es, as of 4/23/2015.

Now, again, that Energy isn't cheap doesn't mean much about future returns. Fundamentals, however, suggest Energy's day in the sun isn't close. The sectors' revenues and earnings are closely connected to oil prices, and these don't seem very likely to bounce back far and fast soon. While US shale drillers are scaling back activity, cutting the number of active onshore rigs by -54% since peaking October 10, production has persistently increased. How? Drillers have scaled back on less productive wells first, focusing on more economical production. Now, the US Energy Information Administration projects the first monthly production drop will come in May (-57,000 barrels per day), but this doesn't mean headwinds are gone.

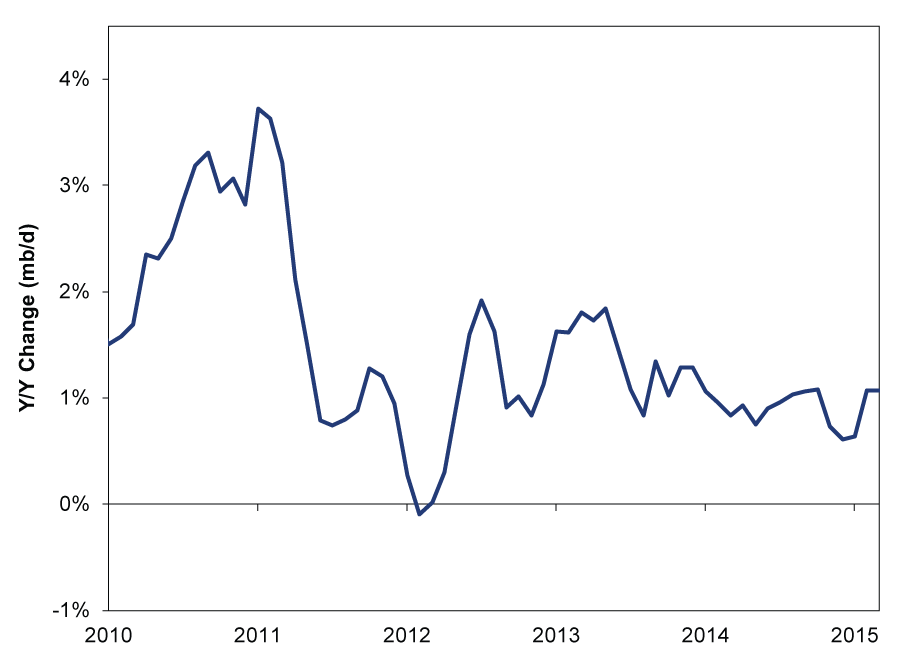

In a phenomenon cutely called "fracklog," shale drillers have begun thousands of wells and stopped within weeks of completion. All they must do is inject high-pressure water and chemicals into the well to crack the rock restraining oil (frack the well), meaning a huge backlog (hence that cute name) of production is sitting and waiting for oil prices to perk. Some estimates suggest more than a Libya is waiting to come online. Others suggest more than 500,000 barrels per day of production would hit if oil rebounded to $65 per barrel. Additionally, the Saudis just got done pumping a near-record high 10.1 million barrels per day in March, suggesting their focus on market share hasn't changed. While we won't suggest either of these factors are a hard ceiling, it would take a significant uptick in oil demand to offset this factor-an uptick that doesn't seem likely to arrive. (Exhibit 3) Perhaps one might expect consumers in fast-growing Emerging Asia to ramp up consumption given lower oil prices, but many governments have cut energy subsidies to the extent prices at the pump aren't down much there.

Exhibit 3: Demand Is Growing, But Slowly

Source: Factset, US Energy Information Administration, 3-month moving average of monthly global oil consumption, 12/31/2009 - 3/31/2015.

What's more, smaller Energy firms are facing an additional pinch. While it may be hyperbolic to claim, as some have, that half of fracking companies and a significant number of drillers will disappear (through failure or M&A) as a result of the oil price collapse, it isn't a stretch to suggest some form of shake out is likely. Already, banks in America's oil patches are reducing exposure to oil firms and jacking up rates. Energy high-yield bond rates have skyrocketed, and smaller oil firms are now turning to issuing shares and asset-backed debt. While it is always darkest before the dawn, most analysts believe Energy sector bankruptcies will rise from here-that would be normal and natural in this type of scenario, as the late-1980s Energy sector collapse shows.

This isn't a death blow for the US oil industry, it is the business's normal ebb and flow. The way forward is added efficiency, which does seem to be coming ... gradually. At a recent conference in Texas, one industry exec noted his firm cut the time to drill an 18,000 foot deep well in half. Another noted the focus on efficient wells to drive output growth more cheaply is likely to slash costs significantly looking forward-industry survivors will be stronger for it, once the herd is thinned. In the foreseeable future, though, this factor doesn't offset the huge increases in supply and slow-growing demand. At the same conference, the head of Kuwait's national oil firm, Prince Nawaf Al-Sabah, said, "Prices are not going to snap back. People are in denial." Oil industry historian and author Daniel Yergin recently said he expects oil prices to be locked in a volatile W-shaped pattern in the immediate future. Now, those are forecasts about a volatile commodity price, but it is worth considering that, if true, Energy sector profit growth will require big cost cuts that will take time.

All in all, we continue to believe the bull market has significant room left to run. We'd just suggest your exposure to the Energy sector should be limited and focus on the biggest, highest-quality integrated firms-those best positioned to weather the storm and come out stronger for it.

Stock Market Outlook

Like what you read? Interested in market analysis for your portfolio? Why not download our in-depth analysis of current investing conditions and our forecast for the period ahead. Our latest report looks at key stock market drivers including market, political, and economic factors. Click Here for More!

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis The New Tariffs in Town Are Still Old News2026-07-24

-

Expert Commentary This Week in Review | Market Volatility, Tariffs, SpaceX

2026-07-24

2026-07-24 -

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23 -

Economics A Summertime Check-in on US Consumers2026-07-23

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today