Personal Wealth Management / Market Analysis

Don’t Let Summertime Blues Influence Your Investing Decisions

Sentiment surveys don’t tell you much about stocks’ future direction.

From the tragic circumstances in Afghanistan and Haiti to COVID’s persistence, headlines have no shortage of bad news these days. The Delta variant in particular has dominated coverage, and it is weighing on the collective mood if the latest sentiment surveys are any indication. US consumers are feeling their bluest in nearly a decade, and the atmosphere seems similarly dour on the Continent. But for investors, sentiment surveys are at best a snapshot of feelings in the present—a coincident indicator. They won’t tell you where the economy or markets are headed next.

Several widely watched surveys highlighted the world’s case of the summertime blues. The University of Michigan’s US Consumer Sentiment Index (CSI) fell -13.5% m/m to 70.2 in August, well below expectations of 81.0.[i] That was the third-largest monthly decline on record—behind only April 2020 and October 2008. The ZEW – Leibniz Centre for European Economic Research’s Indicator of Economic Sentiment for Germany fell 22.9 points to 40.4—a third-straight monthly contraction after May’s 20-year high.[ii] A Wall Street Journal/Vistage small-business confidence survey reported only 39% of small-business owners expect US economic conditions to improve in the next 12 months—nearly 30 percentage points below March’s 67%.[iii] The overwhelming (and unsurprising) factor weighing on sentiment: the Delta variant. As an economist summarized in U-Michigan’s press release, “Consumers have correctly reasoned that the economy’s performance will be diminished over the next several months, but the extraordinary surge in negative economic assessments also reflects an emotional response, mainly from dashed hopes that the pandemic would soon end.”[iv]

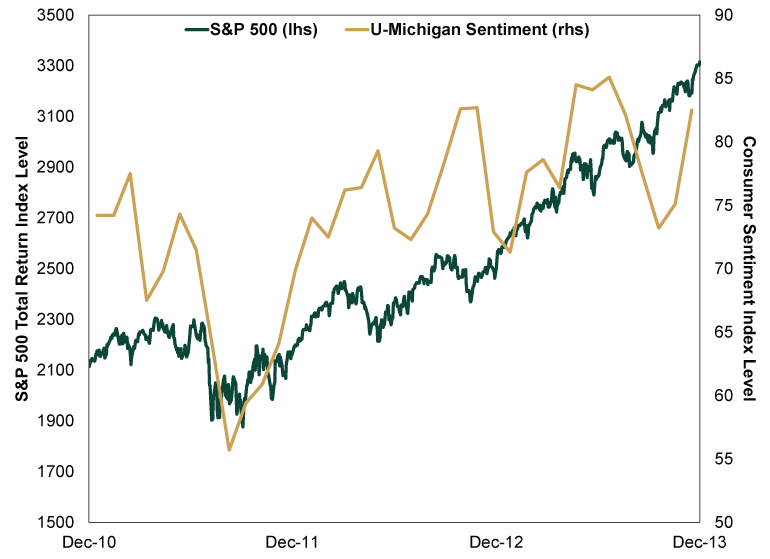

We can certainly empathize. Yet it is also important to keep perspective, as sentiment surveys don’t predict future market returns. Take the U-Michigan survey, which last plumbed similar lows in December 2011 and spent much of that year below today’s level. That year coincidentally[v] illustrates how sentiment surveys are, at best, coincident indicators—and can be influenced heavily by recent stock market movements and fearful headlines. Several big stories weighed on sentiment in 2011. In the US, a debt ceiling fight—and potential credit rating downgrade (which eventually happened)—led coverage. Across the Atlantic, the eurozone’s debt crisis stirred concerns about a potential euro collapse. Global stocks suffered twin corrections (sharp, sentiment-fueled drops of -10% to -20%) that year, further shattering investors’ nerves. However, as Exhibit 1 shows, Americans’ mood didn’t predict lasting market malaise. Nor did it do a good job predicting volatility—mostly, it just mirrored market wobbles.

Exhibit 1: Sentiment Doesn’t Lead Stocks

Source: FactSet, as of 8/18/2021. S&P 500 daily Total Return Index, 12/31/2010 – 12/31/2013, and University of Michigan Consumer Sentiment Index, monthly, January 2011 – December 2013.

The CSI’s 2011 high was in February—not exactly a precursor of the bumpy stock market ride to come. Its 2011 low came in August, when stocks were in the midst of the year’s first correction and hyperbolic headlines were escalating. The US debt ceiling fight culminated with Standard & Poor’s downgrade of America’s credit rating on August 5, while protests and bailout talks for Greece dominated discussions throughout the summer.

Yet poor moods don’t equal a poor reality. Dour headlines can weigh on people’s emotions, especially when coverage speculates the worst is yet to come. In 2011, headlines claimed America’s credit downgrade was a step toward default and Greece’s problems made eurozone collapse imminent. These were all false fears, not serious threats to the US or global economy. Moreover, stocks move most on the gap between expectations and reality. When those dismal projections didn’t pan out, the relief boosted stocks up the proverbial wall of worry. A rocky 2011 gave way to a nice 2012 and gangbusters 2013—and the bull market kept marching until lockdowns truncated it last year.

We think those past lessons can serve investors well today. Sentiment surveys have roughly tracked COVID progress this year. Moods perked up this spring as vaccines rolled out and a summer of fun seemed on the horizon, but they have since cooled alongside rising case counts. However, surprises move markets most—and little with COVID is surprising at this point, and the primary economic risk has always been the associated lockdowns rather than the virus itself. Granted, restrictions and lockdowns are human decisions, which defy prediction. But outside so-called “Zero Covid” areas like Australia and New Zealand, draconian rules largely aren’t reappearing. Instead, continuing to adapt while staying open appears to be the choice for most governments in the US and Europe. To roil markets anew, we think reality would likely have to turn out much worse than feared.

The latest sentiment surveys suggest many expect a pretty bleak foreseeable future. With expectations so dour, reality has a low bar to clear—reason to remain bullish, based on what we see now. That perhaps sounds counterintuitive, but we think it is critical to remember stocks are forward looking and rather callous. In our view, they have likely already moved on from today’s Delta-related setbacks and are looking further ahead, to a world that has continued to adapt to living with COVID.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis The New Tariffs in Town Are Still Old News2026-07-24

-

Expert Commentary This Week in Review | Market Volatility, Tariffs, SpaceX

2026-07-24

2026-07-24 -

Economics A Summertime Check-in on US Consumers2026-07-23

-

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today