Personal Wealth Management / Market Analysis

Don’t Sweat Sideways Stocks

Sideways markets are often frustrating, but stocks can move quickly-make sure you're ready.

Don't let the markets' recent ripples throw you. Photo by Streeter Lecka/Getty Images Sport.

Volatility continued Tuesday, as Asian and European markets tumbled for the second straight day. US stocks started off rocky but clawed back as the day progressed, finishing up a tad. Headlines focused on the usual suspects-China! Greece! Fed!-but folks also put the move in context with the last several months, chalking it up as the latest wobble in a long, frustrating sideways bounce. At times like this, it can be tempting for folks to wonder why the heck they should stay in stocks-after all, enduring volatility is theoretically the price we pay for returns, and if you look at a chart, there doesn't seem to be much payoff for the wobbles. But we'd suggest turning that argument on its head and keeping a longer view. Instead of asking "what reasons are there to own stocks," ask, "are there any reasons not to own stocks?" We think the answer to that second question is a resounding "no," and over time, we think markets should reward long-term growth investors for their patience.

A picture is worth a thousand words, so here are some pictures of stocks this year:

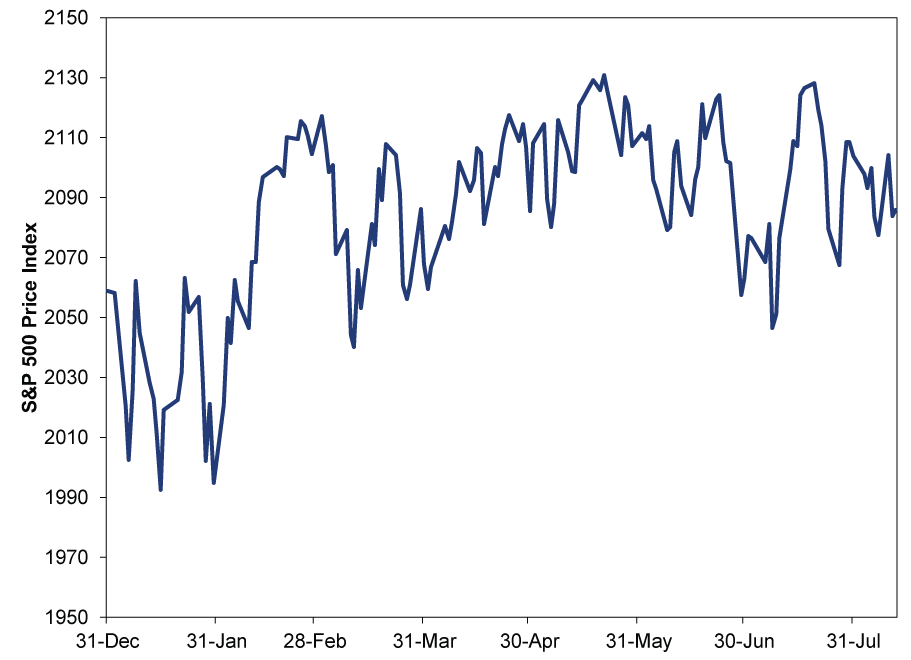

Exhibit 1: S&P 500 Year to Date

Source: FactSet, as of 8/12/2015. S&P 500 Price Index, 12/31/2014 - 8/12/2015

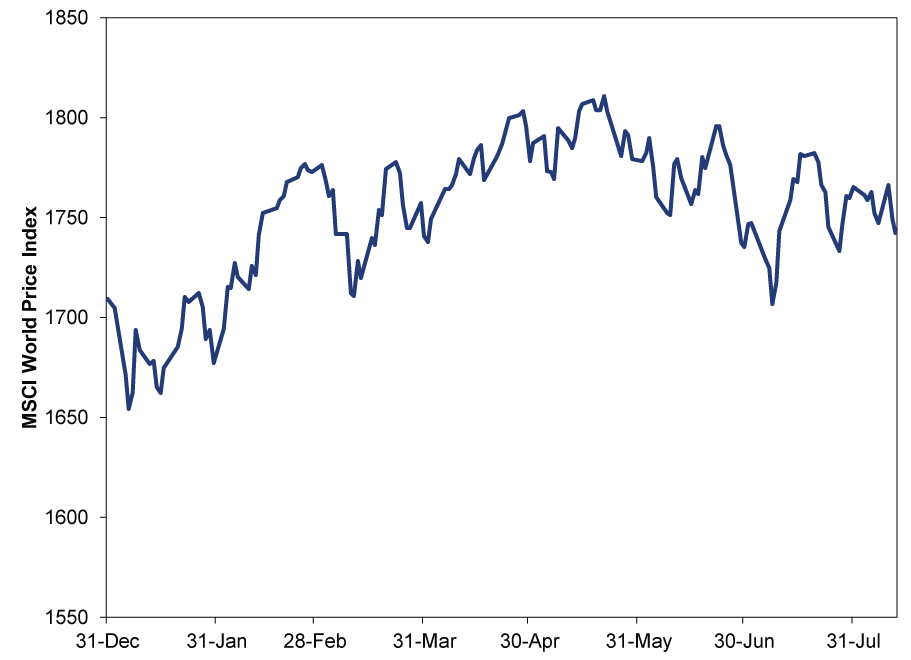

Exhibit 2: MSCI World Index Year to Date

Source: FactSet, as of 8/12/2015. MSCI World Index price level, 12/31/2014 - 8/12/2015.

Exhibit 3: MSCI European Economic and Monetary Union Index Year to Date

Source: FactSet, as of 8/12/2015. MSCI European Economic and Monetary Union Index price level, 12/31/2014 - 8/12/2015.

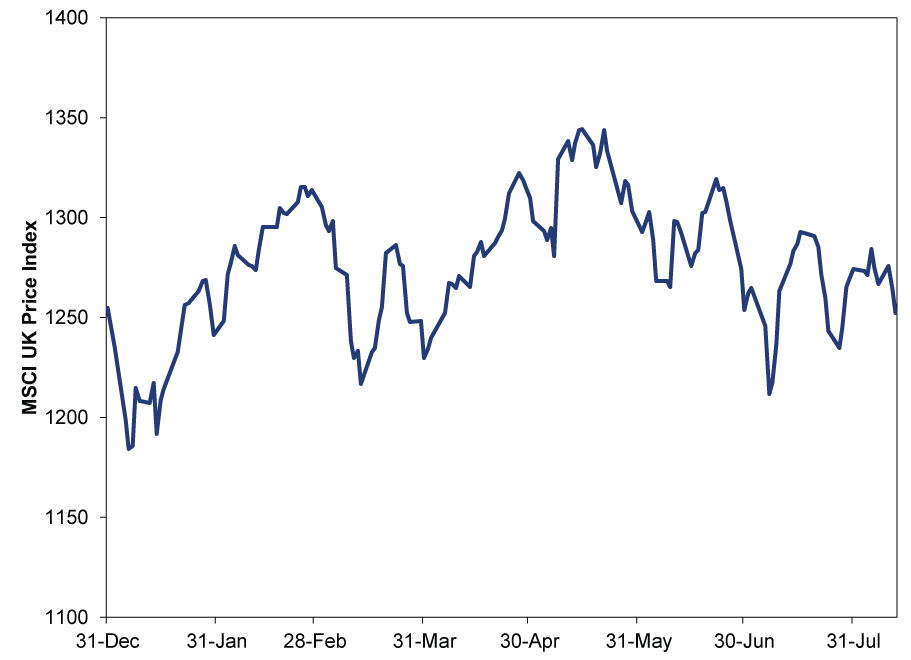

Exhibit 4: MSCI UK Index Year to Date

Source: FactSet, as of 8/12/2015. MSCI UK Index price level, 12/31/2014 - 8/12/2015.

On the one hand, there is lots of wobbling, which feels like volatility. On the other, it all evens out to about flat over the past several months, with quarterly moves well below-average. You might call it Schrodinger's stock market[i]-whether it's volatile or not depends on your perspective and definition.

Either way, Western stocks can't seem to break through. Pundits call this "range-bound" trading-an index bouncing in a narrow bandwidth-and offer all sorts of reasons for it, both technical and fundamental. Perhaps you've read traders are buying at the low levels and selling or short-selling at the tops, content with reaping small gains over and over. Or, maybe you've heard stocks lack a catalyst for a breakout and will be stuck until something good (or, we guess, awful) happens. Then again, perhaps you've seen the technical analysts warning major indexes are at or near their "death cross," where the 50-day moving average crosses below their 200-day average, supposedly signaling worse times ahead. (A wrongheaded interpretation-technical indicators like this aren't predictive, and market history is chock full of false signals from this and other supposed indicators.)

We chalk all of this up as a fruitless search for meaning. Sometimes, you can explain volatility. When a big, scary story accompanies a downturn, it is usually safe to say fear of that thing knocked stocks. We saw that in late June and early July with Greece. But other short-term movement is less easy to explain. We've said before corrections (short, sharp drops of roughly -10% to -20%) can strike for any or no reason. Same goes for sideways stretches. They happen. Tempting as it is to read into these moves, it often does more harm than good. It is very, very easy to overthink your way out of stocks. This might not seem so bad when they're just bouncing along sideways, but these stretches begin and end without warning, and stocks move fast. Being on the sidelines when stocks resume their climb can severely knock your long-term returns. Missed upside-opportunity cost-is money lost.

Contrary to widespread belief, stocks don't need a litany of reasons and catalysts to keep rising. Their natural tendency, over time, is to rise as the global economy grows and corporate earnings grow with it. Even if you don't see any wonderfully bullish developments on the horizon-no big WOWs, so to speak-as long as the global economy looks set to keep growing, politicians remain unlikely to mess things up and investors' expectations aren't outlandish, stocks can do fine. Don't let recent performance make you think otherwise. Past performance never dictates future returns. Stocks look forward, not backward.

The only time to be out of stocks, in our view, is when you see a big reason not to own them-preferably a reason few others see. Reasons might include a withering economic outlook that euphoric investors overlook. That would be a sign stocks have climbed to the top of the bull market's proverbial "wall of worry" and are entering a bear market, a nasty long downturn of -20% or more. Other reasons would fall under what we call a "wallop," a huge (and widely overlooked) negative that could knock a few trillion off world trade or output, triggering a global recession. Potential wallops could include rising trade protectionism, severe monetary policy errors, regulatory changes that impede lending or force widespread deleveraging, sweeping new laws that disrupt property rights or the distribution of resources and capital, and other similar negatives. Big, nasty things that pack a punch, but that most overlook or misperceive as positive-for example, politicians bragging about trade restrictions that allegedly create jobs on the home front.

We don't see any such wallops today. Greece might not survive the year as a member of the eurozone, but it is too small-0.3% of the world economy-and as we show here, the risk of contagion is minimal. China's domestic stock markets are isolated from the world, with little spillover, and they aren't a leading economic indicator. A hard landing in the world's second-largest economy remains as unlikely as ever. A Fed rate hike wouldn't invert the yield curve, and stocks usually do fine for a long while after the Fed begins a tightening cycle. Congress remains gridlocked through 2016 at least, limiting legislative risk in the US. Recent and upcoming elections in the UK, Canada and much of Western Europe heighten gridlock abroad, too. Regulators don't have much of significance on their agenda for now, limiting the risk they concoct something nasty behind closed doors and foist it on markets with little warning. US regulators are still finishing off 2010's Dodd-Frank Wall Street Reform law, and they've telegraphed these plans for years-little shock potential. And as for trade, it is getting freer, not tougher (but keep an eye on Washington, D.C., as some Presidential candidates have discovered protectionism's populist appeal).

Meanwhile, the world economy is growing, and investors remain skeptical about the future, making it easy for results to keep beating expectations whether or not growth accelerates. We don't need some massive GDP pop. After all, stocks did phenomenally in 2013, when the US grew 1.5%, the UK grew 1.7% and the eurozone shrank -0.4%. All three are stronger today. Rip-roaring growth is nice, but it isn't a bull market requirement.[ii] Trite as this may be, growth is growth, and the US, Europe and Asia are growing more than enough to offset well-documented weakness in Canada, Russia, Brazil and other commodity-dependent nations. Rising Leading Economic Indexes in the US and Europe suggest this should continue.

So tune out the noise, don't overthink recent returns, and own stocks. No one can say, with scientific evidence or precision, when stocks will resume setting new record highs. But at some point, they will, and you don't want to miss it.

[i] Yes, we are feeling nerdy today, sorry.

[ii] Heck, returns across many Emerging and Frontier Markets over the past 11 months prove stocks and GDP aren't joined at the hip.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Politics Blunting Burnham?2026-07-21

-

Market Analysis Why the SOX “Bear Market” Isn’t Foreboding2026-07-21

-

Expert Commentary 3 Things You Need to Know This Week | Q2 Earnings, ECB Meeting, Trump Accounts

2026-07-20

2026-07-20 -

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—July 13 - July 172026-07-20

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today