Personal Wealth Management / Market Analysis

Eurozone Update: Investors Still Seem Too Dour Relative to Data

While headlines dwelled on weaker business surveys, good news from loan officers flew under the radar.

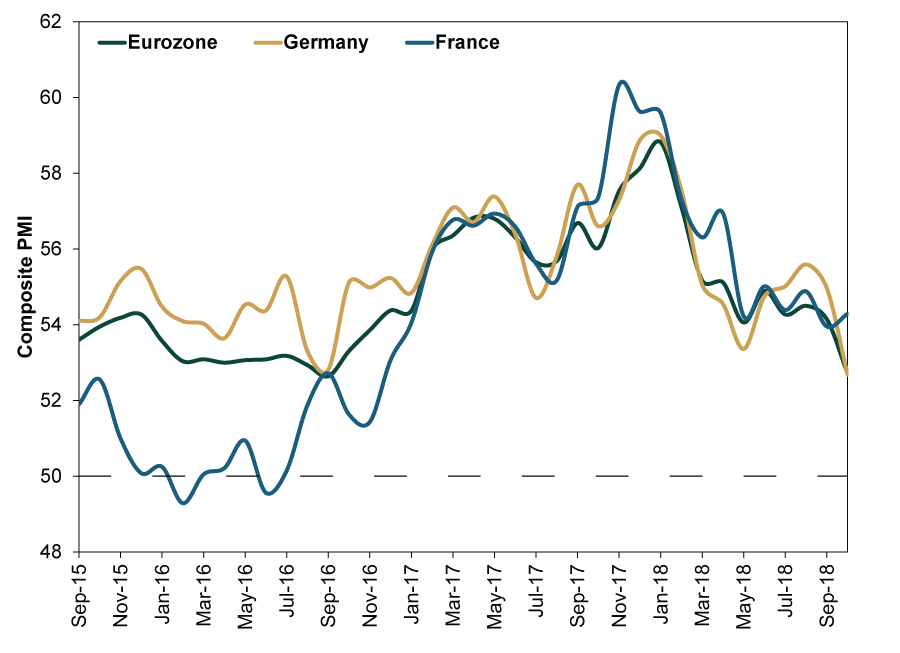

In a busy week for eurozone data, October flash purchasing managers’ indexes (PMI) stole most headlines—and those headlines weren’t terribly happy. Composite PMIs for Germany, France and the overall eurozone showed growth continued this month, but the eurozone’s slowdown continued, with composite PMI hitting its lowest level in 25 months. Services growth and new business held up nicely, but trade jitters weighed on manufacturing. Falling export orders drove total new orders to decline a bit, and sentiment also weighed. So even though PMIs remained well over 50—the line between growth and contraction—people broadly concluded the eurozone was weakening.

Exhibit 1: Eurozone PMIs Still Expansionary

Source: FactSet, as of 10/25/2018. Composite PMIs for the eurozone, Germany and France, January 2016 – October 2018.

But that conclusion seems too hasty. For one, PMIs measure growth’s breadth, not magnitude. All these surveys tell us is slightly fewer German and eurozone firms reported growth. They don’t tell us how much those companies grew. Moreover, survey provider IHS Markit cited manufacturing as the weak link, yet manufacturing is a small share of major eurozone economies. The services sector represents the vast majority of eurozone economic activity, and it is far more insulated from tariffs than manufacturing. In our view, the continued rise in new services business is probably more meaningful for the broader economy than the downtick in manufacturing new orders.

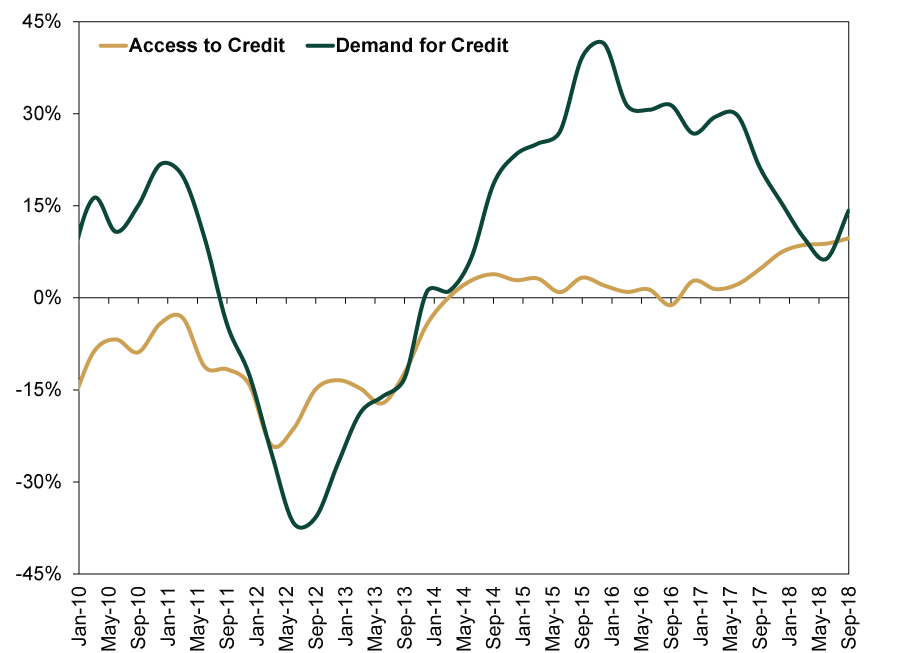

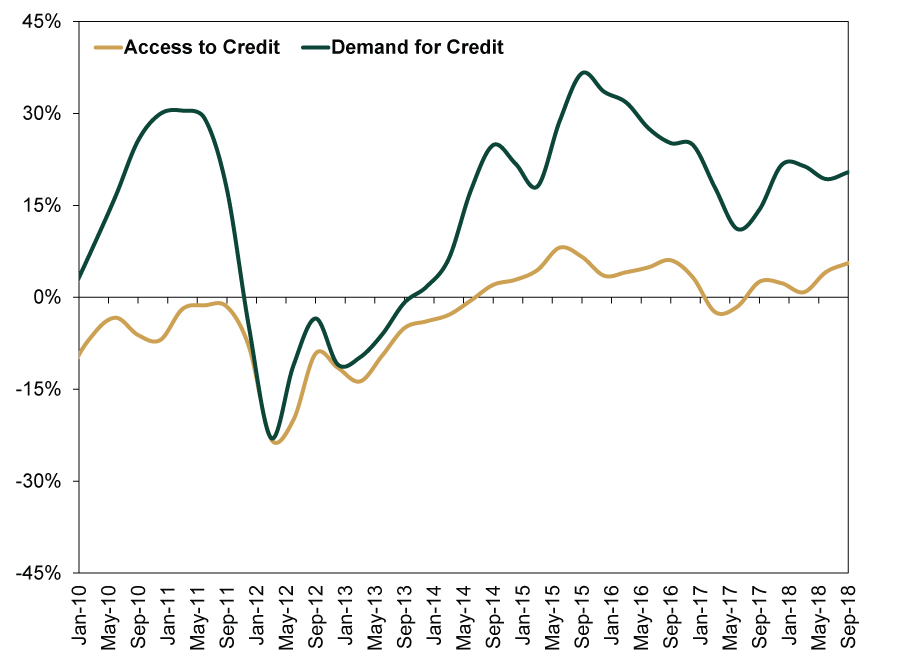

Moreover, eurozone financial conditions remain quite strong. While investors obsessed over PMIs, the ECB’s latest loan survey largely flew under the radar. This survey, which estimates credit supply and demand, is one of the most important indicators of the eurozone economy’s future health—and the latest results, which cover Q3, were good. Banks remain willing to lend to every part of the economy, and they expect demand to remain strong. Exhibits 2 and 3 show banks’ expectations for loan supply and demand in the mortgage and business markets over the next six months. When the lines are above zero, banks are more willing to lend and expect demand to improve—exactly what we have now. The likelihood of a eurozone recession when credit is this available and demand this strong is exceptionally low.

Exhibit 2: ECB Bank Loan Survey Next Six Months—Mortgage Loans

Source: FactSet, as of 10/25/2018. Net percentage of banks reporting greater access to credit and demand for credit, mortgage loans, Q1 2010 – Q3 2018.

Exhibit 3: ECB Bank Loan Survey Next Six Months—Commercial & Industrial Loans

Source: FactSet, as of 10/25/2018. Net percentage of banks reporting greater access to credit and demand for credit, commercial & industrial loans, Q1 2010 – Q3 2018.

The upcoming end of the ECB’s quantitative easing (QE) program makes these charts especially significant. The bank reduced monthly asset purchases to just €15 billion this month, and ECB chief Mario Draghi has said the program will likely end after December unless the economic outlook radically deteriorates. People broadly fear QE’s end will tighten credit and add another economic headwind. But banks clearly don’t see it this way, which supports our long-held view that people wrongly view QE as stimulus and its end as a negative. Loan surveys suggest sentiment is far detached from reality, creating big positive surprise potential as QE ends and loan growth stays healthy.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis The New Tariffs in Town Are Still Old News2026-07-24

-

Expert Commentary This Week in Review | Market Volatility, Tariffs, SpaceX

2026-07-24

2026-07-24 -

Economics A Summertime Check-in on US Consumers2026-07-23

-

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today