Personal Wealth Management / Market Analysis

Fed Rate Hike: Emerging Markets Edition

Rumors of the Fed's impact on Emerging Markets are greatly exaggerated.

Nearly a week has passed since the Fed hiked rates for the first time during this bull market, and US stocks haven't imploded. The world has not ended. Christmas was not cancelled. Americans felt fine enough to spend nearly $250 million on Star Wars tickets opening weekend. Here's something else, little-noticed, that defied most folks' expectations: Emerging Markets (EM) stocks didn't crash. Yes, for all the fear that a rate hike would send capital fleeing from the developing world, tanking EM stocks, sending EM currencies reeling and causing an epic debt crisis, markets are pretty darned calm. That seems about right. This was always a false fear. Some EMs aren't in great shape, but the global risks are exceedingly low.

Fear of Fed tightening harming EM has swirled since May 2013, when former Fed head Ben Bernanke warned the Fed would soon begin "tapering" quantitative easing (QE) bond-buying. Back then, the (wrong) story went that all the QE money had flooded into EM, fueling an unsustainable debt binge as companies borrowed vast sums of cheap dollars. Once QE ended, the party would stop and the dollar would soar, making it impossible for firms to service that mountain of dollar-denominated debt as their own currencies plunged. Those fears sparked volatility in a few EMs that summer, most notably in India and Indonesia.

But then markets calmed, as they regularly do after sentiment-driven swings. As the Fed tapered throughout 2014, there was no EM debt crisis. Several EM currencies weakened as the dollar strengthened from midyear on, but still, no EM debt crisis. Companies didn't default left and right, and yields didn't soar. But investors didn't realize the fear was false, and broadly, they didn't get over it. Instead, the fear morphed: Folks decided rate hikes were the real risk, and the worst was yet to come.

Fears of the Fed whacking EM appear as false now as they were in 2013. As we wrote back then, foreign investment flows into EM during the Fed's allegedly easy money era weren't abnormally large. They rose swiftly at first, reversing the big declines during the Global Financial Crisis, but then they slowed even as QE gained steam. Most countries received investment in line with economic growth. Debt grew, but with solid economic growth, it was easy enough for firms and governments to service. Most EM nations also had big piles of foreign exchange reserves-having learned their lesson after the late-1990s Asian Currency Crisis-allowing them to prevent destructive currency slides if necessary. Several EM central bankers have spent months telling the Fed to get on with it. And, crucially, EM stocks have underperformed the developed world for most of this global bull market, which you wouldn't see if there were an actual bubble inflated by "hot money" from the West.

One thing that we didn't do back then was scale the amount of dollar-denominated debt in EM nations to the size of their economies or global GDP. The data just weren't available. Total foreign debt was easy enough to round up, but not the currency breakdown. But now, thanks to the whizzes at the Bank for International Settlements-the central bank for central banks, basically-we have the numbers. They were published earlier this month, in a special section of the BIS's Quarterly Review, which is devoted to the EM/rate hike issue. You can find it here, and it's worth a read, as it describes the difficulty in rounding up a reliable data set.

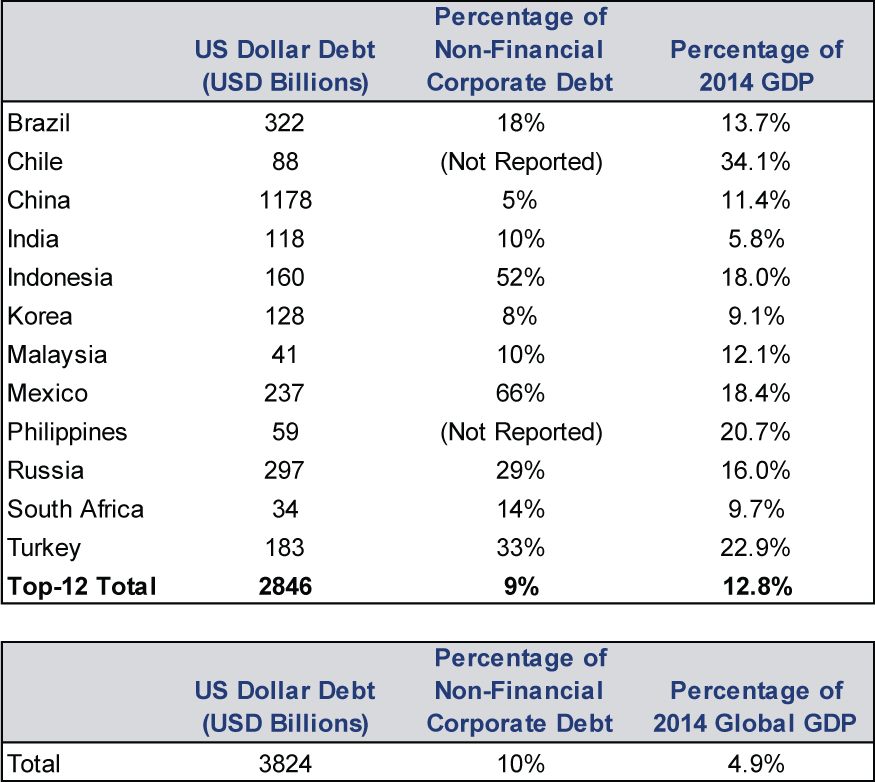

I've long suspected the lack of concrete data on this topic is what allowed the fears to take on a life of their own. It allowed pundits to make sweeping claims about a huge debt mountain and be largely unchallenged. Perhaps that will change now that the BIS has shared their findings with the world. Because, folks, the numbers here just aren't that big. I mean, the headline number looks big: $3.8 trillion in estimated total dollar-denominated debt. But that is scattered across more than 100 countries. The BIS itemizes it only for the top 12, and here is what that looks like:

Exhibit 1: Dollar-Denominated Debt

Source: Bank for International Settlements and IMF as of 12/22/2015. Includes cross-border and locally extended loans plus total outstanding bonds issued by non-banks (of all nationalities) located in the country plus bonds issued offshore by the foreign affiliates of non-banks with a parent headquartered in the country.

Even these numbers are probably a bit overstated, as they include debt issued by foreign firms in each country-some of which was probably issued by developed-world firms. But better to over-estimate than under-estimate, so we'll go with them.

Now, if you're familiar with our definition of a "wallop"-a huge unseen negative that could truncate an otherwise healthy bull market-that 4.9% of GDP for total EM dollar-denominated debt probably jumps out at you. A loss that big would be enough to cause a global recession. But the likelihood the entire $3.8 trillion goes bust is next to nil. Over one-fourth of this total is Chinese, and Chinese authorities are notorious for not letting market forces take over when companies are in trouble. For good or ill, officials have talked a big game about permitting defaults, but they've consistently bailed out troubled corporate borrowers or made borrowers whole on the back-end by funding bond insurers. Even after drawing down foreign exchange reserves somewhat to support the yuan this year, they still have over $3 trillion, ample firepower. Oh, and as you probably gleaned from the preceding sentence, the yuan doesn't float freely. Currency pegs are inherently unsustainable in the long run, but for now, with reserves flush, China is perhaps the least at risk of a sudden, huge currency plunge that would imperil dollar debt.

Exclude China, and we're down to 3.4% of global GDP-with much of it in healthy, growing economies. South Korea is basically a developed country at this point and has developed-world bond yields. India is one of the world's fastest-growing countries. Indonesia and the Philippines are no slouches, either. Mexico faces headwinds from its sizable Energy industry, but growth continues defying expectations. So does Turkish growth. Brazil and Russia are in bad shape and probably most at risk of debt woes. But their combined total, $619 billion, is too small to ripple much globally-0.8% of GDP and both nations have currency reserves sufficient to greatly mitigate any impact. Finally, both countries are also in deep recessions already, however, and their troubles are well-known. Wallops, by definition, are unseen. There is no surprise factor in either country.

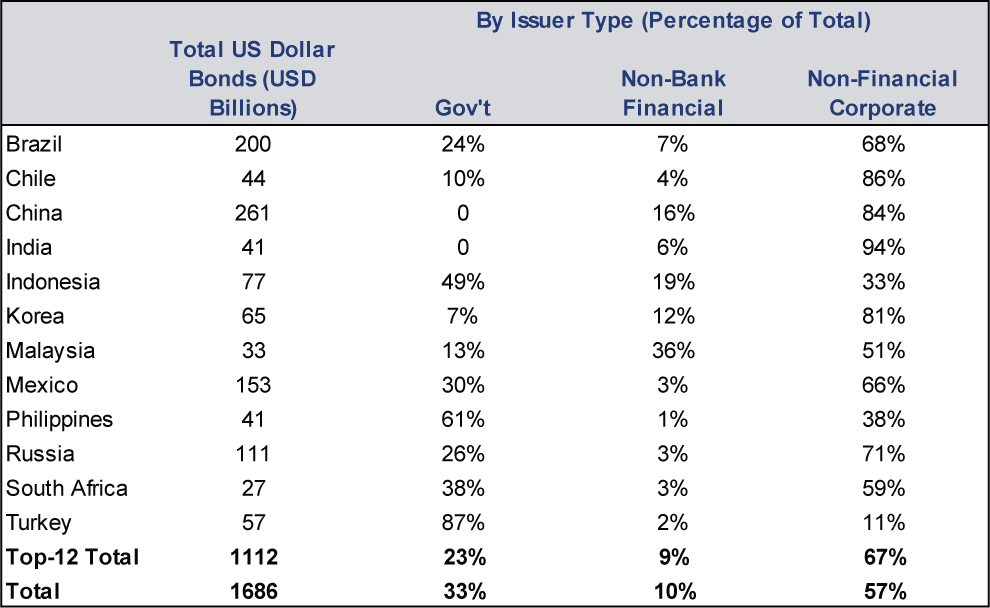

Plus, these totals include bonds and bank loans[i]. Narrow it to bond markets, and everything gets much smaller.

Exhibit 2: Dollar-Denominated Bonds

Source: Bank for International Settlements, as of 12/22/2015. Includes issuers (all nationalities) resident in the country (including issuers with a parent company headquarter in the country) and issuers resident outside the country but with a parent inside that country.

The total bond burden here, $1.7 trillion, is about 2.2% of GDP-most of it in quite healthy and growing nations. You generally don't get a wave of defaults when economies are growing. Bonds in troubled Russia and Brazil are 0.4% of GDP-a bit bigger than Greece.

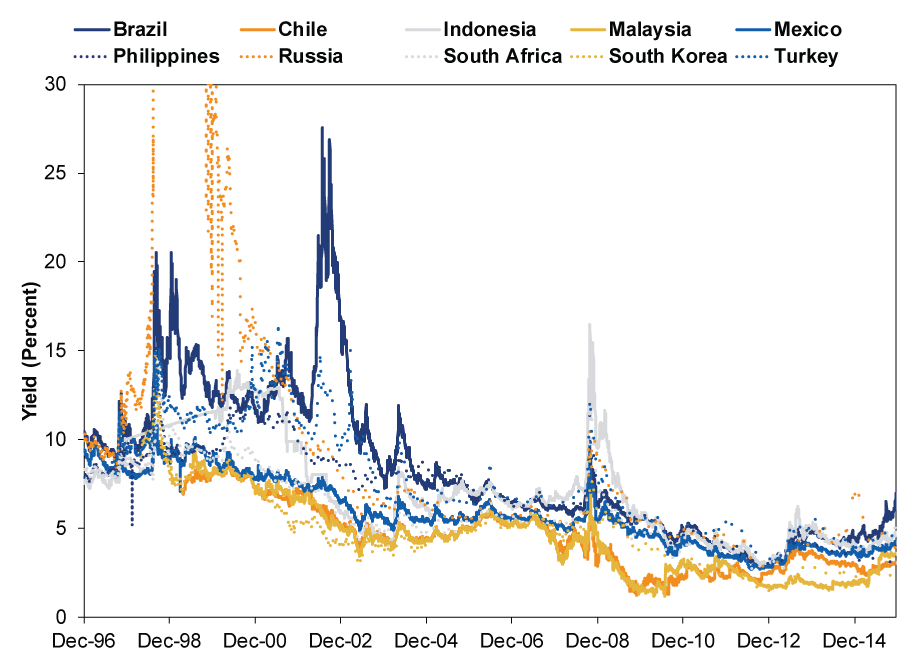

Moreover, markets are pretty darned efficient, and they have been dealing with these fears for about two and a half years. EM bond markets know full well many of these nations' currencies have slid, theoretically making dollar-denominated debt more expensive to service. Yet yields on dollar-denominated debt haven't skyrocketed. Across the board, they are far lower than they were during the Asian Currency Crisis. That isn't what you'd expect to see if default risk on dollar debt were soaring. Yields have drifted up lately in some countries, but not all. Markets are rationally discerning risk on a country-by-country basis.

Exhibit 3: Yields on Dollar-Denominated Sovereign Debt

Source: FactSet, as of 12/22/2015. BofA Merrill Lynch US Dollar Sovereign Bond Index for each of the countries referenced, 12/31/1996 - 12/18/2015. Turkey begins on 9/1/1997. Chile begins on 4/30/1998. Malaysia begins on 6/30/1999.

This chart is messy, but here is what it shows: Yields have stayed fairly tame in Turkey, Mexico and throughout Emerging Asia-except Malaysia, which maintains an embattled currency peg. Rates are also rising in Brazil, Chile and South Africa, all of which are dealing with the economic impact of commodity prices' steep downturn. It wouldn't be shocking to see more troubles in commodity-heavy nations. But these account for a very small share of global output, too small to wallop broader markets.

Happily, sentiment seems to have improved over the last week, as investors have seen EM stocks' resilience to the Fed's move. Many now interpret EM stocks' disappointing returns during the months before the Fed's announcement as markets pricing in the eventual move. That's encouraging-sentiment warming as folks get over false fears is what helps propel stocks up the proverbial "wall of worry." However, it wouldn't shock if fear returned as folks speculate over the Fed's next rate hike. So steel yourself now.

[i] Anecdotally, most of these bank loans were issued by non-US banks.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis The New Tariffs in Town Are Still Old News2026-07-24

-

Expert Commentary This Week in Review | Market Volatility, Tariffs, SpaceX

2026-07-24

2026-07-24 -

Economics A Summertime Check-in on US Consumers2026-07-23

-

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today