Personal Wealth Management / Economics

Four Growthy GDP Reports

Recent GDP reports show fundamental support for stocks.

A flurry of GDP reports hit last week, and they were chock full of good news about the global economy. US Q2 GDP grew 2.3% (seasonally adjusted annual rate), rebounding from Q1's upwardly revised 0.6%. UK Q2 GDP climbed 0.7% q/q (2.8% annualized), accelerating from Q1's 0.4% q/q (1.5% annualized). Spain's Q2 GDP jumped 4.1% annualized, up from Q1's 3.8% and the eighth consecutive quarter of growth. Finally, Ireland finally reported Q1 GDP, announcing a 6.5% y/y jump. While this doesn't foretell future growth, it shows the global economy remains on firm footing, giving stocks plenty of fundamental support.

The US numbers were fairly strong across the board. Consumer spending jumped 2.9%. Total trade rose, with exports gaining 5.3% while imports rose 3.5%. While pent-up demand from Q1's West Coast ports work stoppage explains some of the rise, trade in services-insulated from port labor strife-grew nicely (exports and imports up 2.5% each). So far, it would seem the strong dollar is hardly the export-killer many presumed. Energy, however, remains a headwind. Spending on mining exploration, wells and shafts plunged a whopping -68%, contributing to the -0.6% drop in business investment. But categories less tied to Energy fared better. Investment in intellectual property products climbed 5.5%, driven by a 5.2% rise in R&D spending.

The other detractor was federal government spending and investment, which fell -1.1%. But this doesn't necessarily reflect the broad economy's health-demand is demand, but government spending isn't always a net positive. Government outlays have fallen for years now, yet the economy continued expanding and private businesses eventually filled the gaps. In other words, while falling spending is a minus, it isn't necessarily a structural headwind or sign of slower growth to come.

As usual, the BEA will likely revise this estimate in the coming months and even years-there is no such thing as a final tally. But anything beyond this point is mostly academic, a lesson in the time it takes to gather data and crunch the numbers. Stocks are forward-looking and have already moved on from Q2. They know the economy grew and are already looking toward the rest of this year and next. Just as they don't much care that Q1 growth was revised up from -0.2% to 0.6% as the BEA fixed its faulty seasonal adjustments, nor did they care that the BEA revised growth for 2012 - 2014 down from an average of 2.3% annually to 2.0%. That is mere trivia at this point.

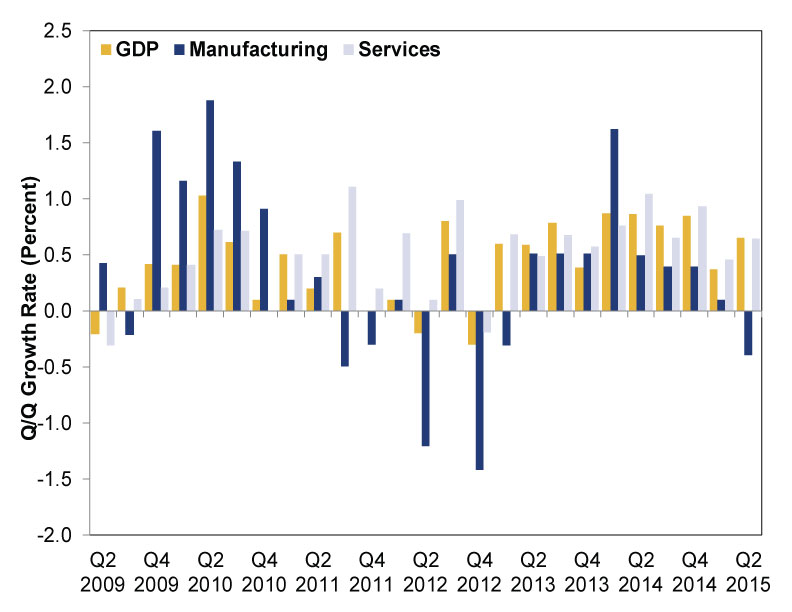

Across the pond, the UK remains near the top of the developed world. Per-capita GDP finally surpassed its pre-recession peak, notching another pleasant (though meaningless) milestone for this expansion. Most eyeballs centered on the sector breakdown, however, as service sector output rose 0.7% q/q, while construction was flat and manufacturing contracted -0.3% q/q, triggering more handwringing over the UK's "unbalanced recovery". But services account for about 78% of the UK economy, so it is logical and normal for the sector to drive growth. There is nothing inherently unhealthy about an economy with pockets of strength and weakness-growth is rarely uniform anywhere. UK manufacturing has been choppy throughout this expansion, but that didn't prevent growth from gaining steam over the last year or the recovery from broadening geographically. (See Exhibit 1)

Exhibit 1: UK GDP Growth 2009-2015

Source: Factset, as of 7/31/2015. UK quarter-over-quarter GDP growth.

Industrial production-which contracted in Q1-grew 1.0%, led by a rebound in Energy as mining and quarrying climbed 7.8%. Some discount this as a potentially one-off boost from new energy industry tax cuts, and perhaps that's true to an extent. Only time will tell whether tax cuts add enough of an incentive for producers to pump while prices are low. But either way, that shouldn't color your interpretation of Q2 as anything other than good. UK growth doesn't depend on the North Sea any more than it depends on factories.

As for Spain and Ireland, their swift growth once again shows the eurozone's recovery is broad-based, with the periphery contributing mightily-growth doesn't depend on Germany pulling everyone along. Ireland's numbers came out at a big lag (as usual for the Emerald Isle), but they were worth the wait: Thanks to revised 2014 growth, Irish GDP is now back at pre-crisis levels, making it the first bailed out eurozone nation to rebound fully from the debt crisis. For all the talk of "austerity" as irrevocably contractionary (ahem, Syriza), the Celtic Tiger has roared all the way back despite suffering the deepest spending cuts as a percentage of its economy. Spain too is nearing pre-crisis levels. Both countries took their medicine, swallowed difficult cuts and reforms, and now they're reaping the benefits. There is a path out of crisis.

Spain's continued growth dispels another myth, namely the belief high joblessness is a drag on future growth. For years, many feared Spain's sky-high unemployment (which peaked just over 26% in late 2012) was a huge structural problem. But Spain has now grown for eight consecutive quarters and is accelerating, while unemployment has eased only mildly to 22.4%. Further improvement will likely be similarly gradual, but Spain has proven high unemployment doesn't prevent growth. Rather, growth helps put folks back to work.

While these GDP numbers are all past-tense-not predictive-other recent data suggest more growth lies ahead. The US July Manufacturing Index reached 52.7, signaling continued expansion. Forward-looking new orders hit 56.5. Eurozone July Manufacturing Purchasing Managers Indexes also exceeded 50, as did readings in Germany, Italy, Spain and The Netherlands. The flash composite (services plus manufacturing) hit 53.7. The recovery remains broad-based.[i] The Conference Board's Leading Economic Indexes for much of the world are in solid uptrends-no US recession in 55 years began while LEI was high and rising. There are weak spots, particularly in commodity-dependent countries (Canada is on the verge of recession, by one common definition), but these are widely known and not big enough to offset the many plusses.

In short, the global economic backdrop for stocks is quite strong right now. The world might not be growing at a rip-roaring pace, but it doesn't need to be. Stocks don't move on data alone. They move on the gap between reality and expectations. Right now, most expect a weakening world, pulled down by China, other Emerging Markets and, eventually, a Fed rate hike. This sets a low hurdle for reality to clear, making continued modest growth quite bullish-and modest growth looks set to continue for the foreseeable future.

[i] Outside of Greece, anyway. Greece's Manufacturing PMI nosedived to 30.2 in July as capital controls and "Grexit" uncertainty hammered businesses.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis The New Tariffs in Town Are Still Old News2026-07-24

-

Expert Commentary This Week in Review | Market Volatility, Tariffs, SpaceX

2026-07-24

2026-07-24 -

Economics A Summertime Check-in on US Consumers2026-07-23

-

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today