Personal Wealth Management / Financial Planning

Guaranteed*

Little do many investors realize the word “guarantee” is multi-faceted—at least in the annuities world.

“Too good to be true.” A statement describing most annuity guarantees—like the promise of “tax-deferred retirement savings, upside growth with downside protection, and [steady] income throughout one’s lifetime” all in one amazing product! Before you dial (now!), we suggest reviewing what those guarantees actually, well, guarantee. Scrutinize the annuity contract, and you’ll likely find silver-bullet promises come up short for investors.

As an old saw goes, annuities are sold, not bought. High commissions give brokers a powerful incentive to peddle them, and guarantees provide a compelling pitch. Guarantees play on investors’ emotions—a time-honored sales trick. It’s the core differentiator between annuities and most other financial products that are in no way guaranteed. Hence, it’s unsurprising insurance firms would want to reiterate it, umm, often:

It seems these days that insurance companies find some way to attach the word “guaranteed” to almost every product, no matter the form, shape or benefit that the product provides. The insurers know that as long as a broker can indirectly use the word “guaranteed” with potential investors in any assumed fashion, products will get sold.

As Andrew Rice recently wrote at LifeHealthPro.com, advertised “guarantees” rarely live up to the hype. Take the commonly quoted “guaranteed” 6% annual return. Investors often forget markets are as unpredictable and uncontrollable for variable annuity sub-account fund managers as they are for everyone else—guaranteed returns don’t exist. What the phrase frequently refers to is the annuity’s income withdrawal rate, which isn’t performance or a return. Consider: If you owned a variable annuity with stock market-related subaccounts in 2008, your contract value likely went down. If you held in 2009, it likely rose. Contract value is what you get if you sell (surrender) the contract. It is based on real, not guaranteed*, stock market returns.

Bull market participation with no downside is a myth, too, though it’s often promised in equity-indexed annuities. It’s true enough most equity-indexed annuities’ contract values won’t fall if markets decline, yet you are extraordinarily unlikely to achieve anything resembling equity-like appreciation over time. Returns are usually capped at some periodic maximum, often a monthly limit that would sum near the S&P 500’s long-term average—around 8% to 10%. There are also participation rates, meaning you get only a share of market return. These are more impactful over time than the 0% floor. Markets rise far more often than fall. Compound growth is the reward of an equity investment, but equity-indexed annuities caps and participation rates frequently lead to CD-like returns. That isn’t market-like. (And if avoiding downside is your sole aim, then your default investment option should have nothing to do with stocks. Or bonds. Or mutual funds. Or variable annuities. It’s cash.)

Think of it this way: Insurance firms aren’t non-profits. Annuities are big money-makers. If an advertised feature seems better for you than the provider, chances are there is a big asterisk or negative elsewhere offsetting that benefit. Prospectuses nearly as thick as the Affordable Care Act with roughly equally complex language disclose everything you need to know, but the upfront 7% to 10% commission for indexed annuities and 3% to 7% commission typical for variable annuities give brokers a big incentive not to highlight and tag the drawbacks. So you often have to hunt through a dense document written in legalese to determine the total costs, underlying investments, withdrawal rates, penalties and other conditions.

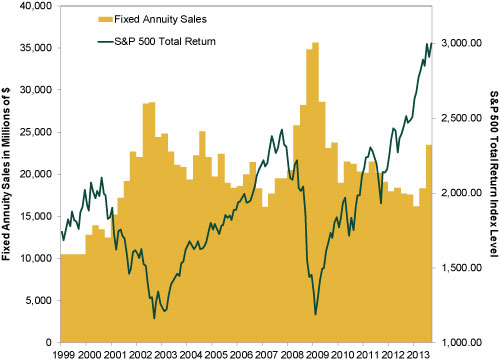

Studying the prospectus is an intense but necessary exercise. But for many prospective purchasers, it can be tempting to skip. Why? Annuities are often emotional purchases, and discipline and emotion don’t mix. Brokers know this. It’s no coincidence fixed annuity sales tend to peak during bear markets and corrections. Market declines are disconcerting, and brokers know pressing the “guarantee” button can perk a skittish investors’ attention.

Exhibit 1: Fixed Annuity Sales Peak at Market Lows

Source: LIMRA, Factset; S&P 500 Total Return Index level for the period 12/31/1998 through 09/30/2013.

This runs afoul of a cardinal rule of long-term investing: Each investor’s long-term strategy should be based on his own goals, objectives, time horizon, cash flow needs, financial situation and other personal factors. Fixed annuities are one of the lowest returning, least volatile investments out there and very illiquid—this isn’t just a temporary tactical switch to cash or bonds. It’s a wholesale flip into a locked-in fixed income strategy. Did all these fixed annuity buyers’ long-term goals really go from long-term growth one week to perpetual cash-like returns the next? Did their cash-flow needs and time horizon change so drastically?

Maybe, but we have our doubts. But when stocks are moving fast, the allure of guarantees and flashy sales tactics can trump rational thought.

Not to say every broker sees their clients as meal-tickets—no doubt some genuinely (if often incorrectly) believe annuities are truly best for their clients. Perhaps they’re not aware clients could reach the same goals with less costly and restrictive investments. But in our view, the high commissions increase potential conflicts of interests—and should equally raise investors’ skepticism of the product.

Regardless, for investors, independent due diligence is vital—with any product, not just annuities. Critically assessing the sales pitch, prospectuses and alternatives could be the difference between meeting and missing long-term goals. It’s an old adage but apt in investing: If it sounds too good to be true, it probably is.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis The New Tariffs in Town Are Still Old News2026-07-24

-

Expert Commentary This Week in Review | Market Volatility, Tariffs, SpaceX

2026-07-24

2026-07-24 -

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23 -

Economics A Summertime Check-in on US Consumers2026-07-23

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today