Personal Wealth Management /

Happy Anniversary, Taper Talk!

Last May, Ben Bernanke alluded to a quantitative easing taper. What does that mean for markets and the economy one year later?

Former Fed Chairman Ben Bernanke testifies in front of the Joint Economic Committee on May 22, 2013. Source: Alex Wong/Getty Images.

“If we see continued improvement and we have confidence that this is going to be sustained, in the next few meetings we could take a step down in our asset purchases.” One year ago yesterday, that’s how then-Fed head Ben Bernanke answered the question of when the Fed would begin winding down its quantitative easing (QE) program. The sentence launched furious speculation over the exact timing and angst over the impact of the actual “taper,” which finally began in January. What most folks didn’t realize: Markets started pricing in the change the instant Bernanke spoke. Long-term rates rose. It was a de facto taper. A year later, with asset purchases down from $85 billion per month to $45 billion, it’s clear the taper is nowhere near bad for the economy or stocks.

When the Fed actually started reducing bond purchases in January, long-term interest rates dropped—counter-intuitive to some, but to be expected considering markets had been digesting the change for eight months. From May 22 through December 30, 10-year US Treasurys rose a full percentage point. Exactly what folks feared would bring disaster. Yet stocks are up! As a point of trivia, the S&P 500 and MSCI World Total Return Indexes have hit 44 and 43 all-time highs over the past year! The economy hasn’t cratered either. Growth picked up post-taper talk. It took a breather in Q1, but with the Leading Economic Index (LEI) still high and rising and April data fairly strong overall, things are chugging right along.

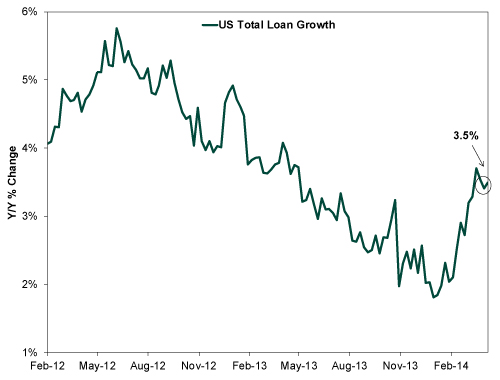

In our view, none of this should surprise. Higher long-term rates, coupled with short rates pegged near zero, means a steeper yield curve—a big positive for economies and markets. Yet one benefit of a steeper yield curve was slower to fall into place: Lending. Banks are prime beneficiaries of a bigger spread between short and long rates, which represents their potential profit margin on lending. A wider yield curve spread means lending is more profitable, in theory encouraging banks to lend more. Yet, as shown in Exhibit 1, loan growth continued slowing after the taper speech and didn’t start trending up until January, around when the taper started.

Exhibit 1: Total US Loan Growth

Source: FactSet, as of 4/21/2014. Seasonally adjusted weekly assets of Commercial Banks, Loans & Leases in Bank Credit, from 2/3/2012 – 4/11/2014.

The explanations here are twofold. One, it’s normal for monetary policy to impact the economy at a lag—it takes time for changes in the yield curve to flow through to banks’ net interest margins (NIM), which is what ultimately drives loan growth. NIMs kept dropping in Q2 and Q3 2013—a knock-on effect of the flatter yield curve before May 22. They finally ticked up a bit in Q4, finishing the year at 3.3%. Then, the actual taper likely gave banks more confidence they could, well, bank on wider margins looking forward, giving them all the more incentive to lend more eagerly. Many banks project NIMs to widen as 2014 progresses, which should support steady loan growth looking ahead.

This should hold, in our view, even with long rates down to 2.54% as of market close May 23, 2014—up a hair from the recent low of 2.49% on May 15. Volatility is normal in stock and bond markets alike, and it would be folly to assume rates are settling into a post-taper lull. Plus, even with the small drop, the yield curve spread remains wider than it did a year ago. It’s still wide enough to drive the bulk of recent LEI growth, and as QE keeps winding down and more of the buying pressure eases, it should stay wide (and get wider!), driving the economy and bull market higher.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Economics Quick Hit: Durably Broad-Based Growth2026-07-29

-

Market Analysis On the Chop in the Oil Market2026-07-29

-

Politics Takaichi Raises Japan’s Wall of Worry2026-07-27

-

In The News Why Kevin Warsh should think twice about hiking interest rates — even as anxiety over the Iran war grows2026-07-27

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today